Ultimate Guide to Seasonal Income Planning

Ultimate Guide to Seasonal Income Planning

Freelancers often face unpredictable income cycles, making it tough to manage finances effectively. This guide offers practical strategies to help you navigate irregular earnings, avoid financial stress, and maintain stability year-round. Here’s what you’ll learn:

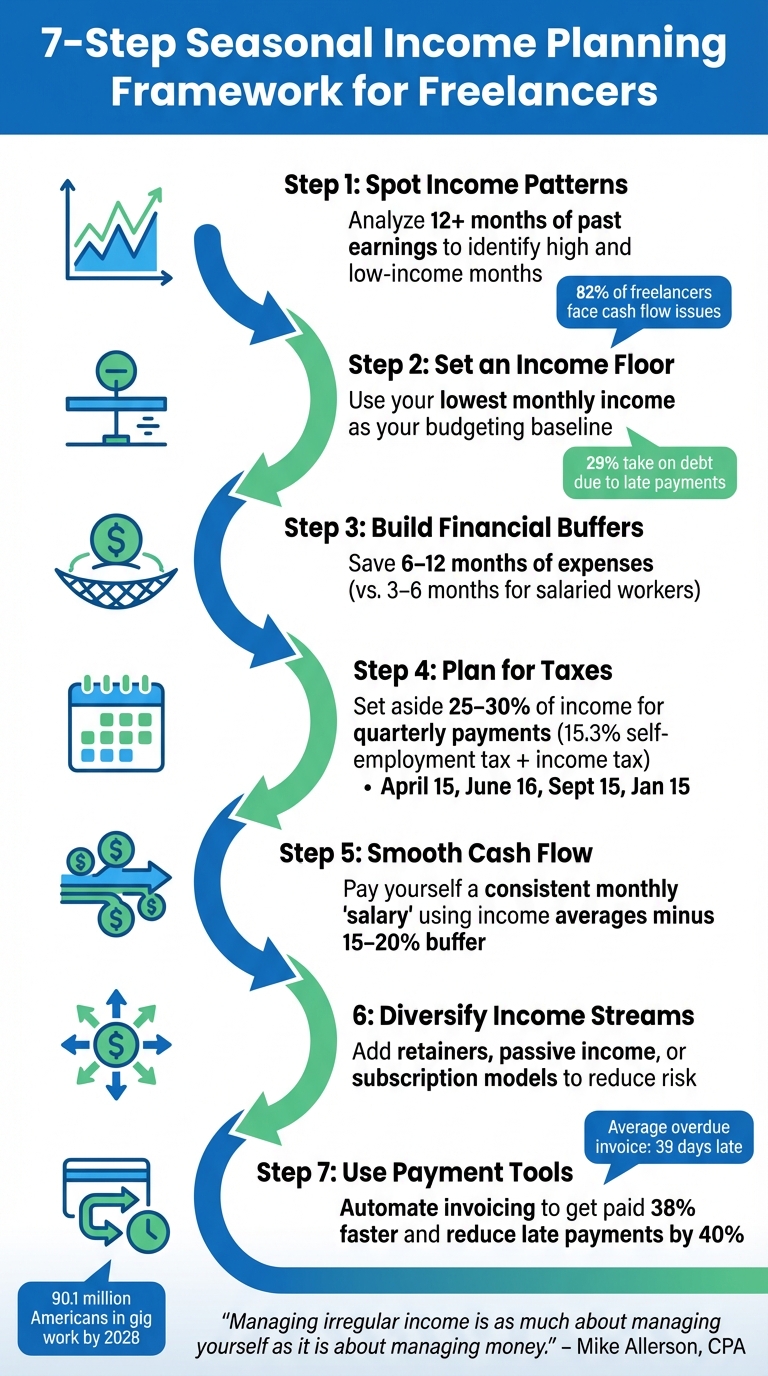

- Spot Income Patterns: Analyze past earnings to identify high and low-income months.

- Set an Income Floor: Use your lowest monthly income as a baseline for budgeting.

- Build Financial Buffers: Save 6–12 months of expenses to handle lean periods and emergencies.

- Plan for Taxes: Set aside 25–30% of income for quarterly tax payments to avoid penalties.

- Smooth Cash Flow: Pay yourself a steady monthly “salary” using income averages and buffers.

- Diversify Income Streams: Explore retainers or passive income options to reduce financial risk.

- Use Tools for Timely Payments: Platforms like Paid on Time can prevent cash flow issues caused by late payments.

7-Step Seasonal Income Planning Framework for Freelancers

My Income Is Extremely Seasonal, How Do I Plan and Budget?

sbb-itb-66f4c95

What Seasonal Income Is and How It Affects Your Finances

Seasonal income refers to earnings that fluctuate throughout the year based on industry demand, specific seasonal trends, or project cycles. Unlike a steady paycheck, this type of income can come in waves - think of freelancers who might have several lucrative projects in a row followed by quieter months.

This irregular cash flow creates challenges that go beyond simple budgeting. Fixed expenses, like rent or loan payments, don’t wait for your next "busy season", which can lead to financial gaps. Additionally, banks and lenders often view inconsistent income as risky, making it harder to qualify for loans, mortgages, or even rental applications. Freelancers also face a 15.3% self-employment tax, which adds another layer of financial pressure if planning isn’t handled carefully.

The unpredictability of seasonal income can also have a mental impact. Months with low income may lead to anxiety, self-doubt, and hasty financial decisions. On the flip side, high-earning months can create a false sense of security, leading to overspending. This emotional rollercoaster often makes long-term goals - like buying a home or taking a vacation - feel out of reach.

Finding Seasonal Patterns in Your Income

To get a handle on seasonal income, start by analyzing at least 12 months of past earnings. Use bank statements, invoices, or accounting software to track income month by month. Plot these numbers in a spreadsheet to pinpoint "feast" and "famine" periods. Once you’ve identified trends, calculate your average monthly income by dividing your total annual net income by 12. This gives you a baseline to guide your budget, even during peak months.

Different industries often follow predictable seasonal cycles. For instance:

- Tourism and landscaping tend to thrive in the summer due to weather-driven demand.

- Retail and entertainment hit their stride in winter, fueled by holiday shopping and events.

- Tax preparation sees its busiest months during the first quarter of the year, aligning with tax filing deadlines.

- Construction and outdoor services often slow down in colder months but pick up in spring and summer.

Here’s a quick snapshot of some common industries and their income patterns:

| Industry | Typical Peak Season | Common Causes of Fluctuation |

|---|---|---|

| Tourism & Landscaping | Summer | Weather-dependent demand |

| Retail & Entertainment | Winter | Holiday spending and events |

| Tax Preparation | Q1 (Jan–April) | Annual filing deadlines |

| Construction | Spring/Summer | Weather and building cycles |

By identifying these patterns, you can better plan for the highs and lows of your income cycle.

Why You Need to Plan Ahead for Income Fluctuations

Recognizing income trends is just the first step - what’s critical is using this information to plan ahead. Without a strategy, irregular income can lead to reactive decisions. For example, you might accept underpaid work just to make ends meet, delay necessary business investments, or rack up credit card debt during lean times. Using an agreement-backed payment platform can help stabilize cash flow by ensuring you get paid as soon as work is completed. On the other hand, high-earning months can lead to overspending, leaving you unprepared for the next slow season.

Experts recommend that freelancers set aside an emergency fund to cover 6–12 months of expenses. This is more than the typical 3–6 months suggested for salaried workers, as freelancers don’t have unemployment benefits to fall back on during dry spells. Additionally, if you expect to owe more than $1,000 in taxes for the year, quarterly estimated tax payments using Form 1040-ES are required. Missing these payments can result in penalties, so staying on top of your finances is crucial.

Creating a Financial Plan for Variable Income

When your income fluctuates from month to month, having a financial plan that prioritizes stability and flexibility is key. Start by building your system around your lowest monthly earnings - this ensures you're prepared for leaner times while making the most of peak income periods.

Establishing Your Income Floor

Your income floor is the lowest amount you earned in a single month over the past year. Financial experts suggest using this figure, rather than your average income, as the foundation of your budget. Why? It prevents overspending during slower months. Suze Orman emphasizes the importance of knowing this "survival number", which represents the absolute minimum needed to cover essentials like housing, utilities, insurance, debt payments, groceries, and critical business expenses.

Once you've determined your income floor, consider implementing an income smoothing system. This means paying yourself a consistent amount each month from your business account, regardless of how much you earn. By absorbing income fluctuations at the business level, your personal finances stay steady.

Another helpful strategy is percentage-based budgeting, such as the 50/20/30 framework. Here's how it works:

- Allocate 50% of your income to essentials, including taxes (set aside 25–30% for taxes specifically).

- Use 20% for financial goals like savings or debt repayment.

- Reserve 30% for discretionary spending.

This approach adjusts automatically with your income, encouraging higher savings during profitable months without requiring constant recalculations. To make it work, use separate accounts for business, personal expenses, taxes, and savings. Deposit any surplus from peak months into a buffer account to maintain a steady paycheck. As CPA Mike Allerson says, "Living below your average isn't pessimism. It's insurance."

Setting a Basic Budget for Core Expenses

Your core budget should focus on the essentials - expenses that keep your life and business running. Use your income floor to guide this survival budget, which includes necessities like rent or mortgage, utilities, insurance, minimum debt payments, groceries, transportation, and essential business tools.

This process will reveal your survival number, the bare minimum you need to cover your obligations. The idea isn't to live at this level constantly but to know exactly what you need when income dips. To manage spending effectively, organize your expenses into tiers:

- Baseline Tier: Covers survival essentials.

- Comfortable Tier: Includes flexible costs like dining out or subscriptions.

- Thriving Tier: Adds growth expenses, such as retirement contributions or extra debt payments.

When income is tight, stick to the baseline tier. During better months, you can move up to the comfortable or thriving tiers. This tiered approach helps prevent financial stress by offering flexibility without sacrificing structure.

Building an Emergency Savings Fund

An emergency savings fund is a critical safety net for anyone with variable income. Unlike your income buffer, which covers predictable shortfalls, an emergency fund is reserved for unexpected crises - think medical emergencies, major repairs, or losing a key client. Freelancers, who lack unemployment benefits, should aim for three to six months of expenses, or even six to twelve months for added security.

To build this fund, use a percentage-based savings model. For example, save 20% of every payment you receive. If you earn $10,000 in a month, save $2,000; if you earn $3,000, save $600. This method ensures your savings grow in proportion to your income.

To stay organized, open separate accounts for income, taxes, operating expenses, and emergency savings. When a payment comes in, allocate funds immediately - set aside 25–30% for taxes, then direct a fixed percentage into your savings before covering personal expenses. As CPA Mike Allerson advises, "If you can't afford to set aside taxes, you can't afford the income."

A well-funded emergency account offers more than just financial security - it gives you freedom in decision-making. With only two months of savings, you might feel pressured to take on any available work. But with six months or more, you can afford to wait for opportunities that align with your goals.

Using the Annual Average Method to Distribute Income

The annual average method is another way to smooth out income fluctuations. Start by calculating your total net earnings from the past year and dividing by twelve to find your average monthly income. This number becomes your baseline monthly "salary."

Here’s how to implement it:

- Open a dedicated business account for all client payments.

- Calculate your average monthly income and reduce it by 15–20% to create a buffer.

- Transfer a fixed amount to your personal account twice a month, mimicking a steady paycheck.

During high-earning months, let any surplus stay in your business account or add it to your income buffer. During slower months, continue paying yourself the same amount, using the buffer to cover the shortfall. If your business account balance drops below two months of personal salary, it may be time to adjust your draw or focus on boosting revenue.

To keep things on track, schedule a 15-minute weekly money check-in. Use this time to review recent income, check your buffer balances, and adjust your spending plans as needed. Regular check-ins help you avoid surprises and ensure your income smoothing strategy works as intended. With consistent application, you'll turn unpredictable earnings into a reliable cash flow system.

Managing Income and Expenses Year-Round

Once you've crafted a financial plan that includes your income floor and emergency fund, the next challenge is maintaining that stability throughout the year. This involves staying disciplined during both high and low-income periods, preparing for predictable expenses like taxes, and taking advantage of growth opportunities. Consistent planning ensures you stay financially secure, no matter the season.

Budgeting for Fixed and Variable Expenses

Fixed expenses - things like rent, insurance, loan payments, and essential utilities - are predictable and should always take priority in your budget. These are best funded directly from your baseline monthly "salary." On the other hand, variable expenses, such as groceries, dining out, and entertainment, require more flexibility. During slower months, stick to your survival budget by cutting back on non-essentials. When income is higher, you can afford to loosen the reins on discretionary spending.

To avoid overspending, consider using separate accounts. Ideally, you should have at least five: one for incoming revenue, one for personal operating expenses (your "salary"), a tax account, an emergency fund, and a business operating account. When payments come in, allocate 25–30% to taxes before distributing the rest. As SelfEmployed.com wisely puts it:

If you can't afford to set aside taxes, you can't afford the income.

Planning for Taxes and Large Purchases

If you're a freelancer and owe $1,000 or more in taxes annually, the IRS requires you to make quarterly estimated tax payments. Missing these deadlines can result in penalties, so treat saving for taxes as a must. For 2026, these payments are due on April 15, June 16, September 15, and January 15, 2027.

Self-employment taxes tack on an additional 15.3% for Social Security and Medicare, not to mention federal and state income taxes. To avoid a last-minute scramble during tax season, automate your tax savings by regularly transferring funds into a high-yield savings account. For major purchases - whether it's new equipment, professional development, or a significant personal expense - time these buys during periods of higher income to protect your reserves and budget.

Adding Income Streams to Reduce Risk

Diversifying your income sources can ease financial stress, especially during slower months. The goal is to create a more predictable income stream without overloading your schedule. One way to do this is by offering retainer agreements to your best clients. Charging a fixed monthly fee in exchange for a guaranteed block of time can provide a steady income baseline. As SelfEmployed.com notes:

One or two recurring clients often stabilize cash flow enough to make everything else feel manageable.

You can also explore passive income opportunities, such as selling templates, online courses, or digital downloads. These require minimal ongoing effort and can bring in revenue year-round. If you find yourself with gaps during off-seasons, gig platforms can offer short-term work without long-term commitments. For service-based businesses, subscription models or maintenance agreements can create steady, recurring revenue.

Ultimately, the freelancers who succeed in the long haul aren't necessarily those who earn the most in a single month. Instead, they are the ones who design their financial systems to handle unpredictability with ease.

Using Paid on Time to Ensure Predictable Cash Flow

Even the most carefully crafted financial plan can crumble when clients don’t pay on time. The numbers speak volumes: 82% of freelancers have faced cash flow issues, and 29% have had to take on debt due to late payments. On average, freelancers are left with 45 days of unpaid expenses, making it nearly impossible to maintain the consistent "salary" approach we discussed earlier. This is where Paid on Time (https://paidontime.app) becomes an essential part of managing seasonal income.

How Paid on Time Streamlines Payment Collection

Paid on Time tackles the root cause of payment delays: the manual invoicing process. Instead of waiting weeks after sending an invoice, the platform secures payment methods upfront and allows for one-click charges once the work is delivered. This method aligns with research showing that invoices sent immediately after work completion are paid 40% faster than those delayed until the month’s end.

The platform also supports upfront deposits, a critical feature for freelancers managing irregular income. By requiring 25–50% deposits from new clients or for large projects, you can improve cash flow and filter out unreliable clients. For projects exceeding $3,000, you can implement milestone-based payments - such as 30% upfront, 30% at the midpoint, and 40% upon completion - to ensure steady income over the course of longer assignments. Automating payments with tools like this has been shown to reduce late payments by 40% and help freelancers get paid 38% faster. These features also pave the way for clearer, enforceable agreements.

Minimizing Payment Disputes with Clear Contracts

Vague terms are often the root of payment disputes. Paid on Time solves this by generating legally binding agreements before the project even begins. These agreements establish specific payment terms like "Net 15" or "Net 30", replacing ambiguous phrases like "payment upon completion". The platform’s AI-powered contract scanner reviews your terms to ensure they’re legally sound and protect your cash flow.

Having detailed agreements in place also reduces the risk of scope creep or endless revision requests, which can delay final payments. When clients know exactly what’s included, how many revisions they’re entitled to, and when payments are due, disputes become far less likely. Additionally, the platform can verify late fee clauses (e.g., 1.5% monthly interest), encouraging clients to pay on time without the need for uncomfortable conversations. Considering that 71% of freelancers struggle with late payments and the average overdue invoice takes 39 days beyond its due date, these safeguards are a vital part of keeping your financial plan on track.

Conclusion

Freelancers who succeed over the long haul know how to manage their finances in a way that absorbs unpredictability without triggering panic. This guide has walked through key strategies to help you forecast, budget, and protect your finances, so you can maintain stability even when income fluctuates.

An effective financial plan boils down to four key steps. Budgeting helps you identify your "survival number", while forecasting gets you ready for slower months. Saving builds a buffer that allows you to pay yourself a steady salary from your business account. And tools like Paid on Time ensure the income you’ve planned for actually arrives on time, without disputes.

“Managing irregular income is as much about managing yourself as it is about managing money.” – Mike Allerson, CPA

With projections showing over 90.1 million Americans will be involved in gig work by 2028, learning how to manage seasonal income is no longer optional - it’s rapidly becoming a critical skill for nearly half the workforce. Start by analyzing your past earnings to identify your income floor. Separate your business and personal finances immediately, and treat taxes like non-negotiable expenses by setting aside 25–30% of every payment. Make it a habit to review your financial systems every quarter to avoid making rash decisions.

The ultimate goal? Build a financial system that softens the blow of income ups and downs. When you have a solid plan in place, you can move beyond the stress of surviving paycheck to paycheck and focus on growing your freelance career with confidence.

FAQs

How do I pick my monthly “salary” with irregular income?

To manage a steady “salary” when dealing with irregular income, start by calculating your average monthly income. Look at your earnings over a significant period to identify patterns. Use this average to set a consistent amount you can rely on for budgeting.

It’s also smart to create separate savings accounts, such as an “off-season” fund. This can act as a safety net during months when your income dips, ensuring you can cover your expenses and maintain financial stability despite fluctuations in earnings.

What’s the difference between an income buffer and an emergency fund?

An income buffer is a small reserve of money set aside to smooth out cash flow when income fluctuates or dips temporarily. It helps ensure that your day-to-day spending stays consistent, even during times of irregular or reduced income.

An emergency fund, however, is a larger savings reserve designed for significant, unexpected expenses - things like losing a job, major medical bills, or urgent home repairs. While the income buffer is meant to bridge short-term gaps, the emergency fund offers protection for more substantial, long-term financial challenges.

How can I avoid cash flow gaps when clients pay late?

Freelancers can avoid cash flow gaps caused by late client payments by taking a proactive approach. Start by building an emergency fund to handle slower periods - it’s your safety net. Also, establish clear payment terms in your contracts, like upfront deposits, to ensure a steady flow of income.

Make it a habit to forecast your earnings, keep a close eye on expenses, and automate savings. This way, you’ll always stay one step ahead financially. Pair these practices with well-structured agreements, and you’ll be better equipped to maintain financial stability without depending on delayed payments.