How Much to Save for Taxes as a Freelancer

How Much to Save for Taxes as a Freelancer

As a freelancer, saving for taxes is critical to avoid surprises. Unlike employees, taxes aren’t automatically deducted, and you’re responsible for paying both income tax and self-employment tax (15.3%). Here’s what you need to know:

- Save 25–35% of your net income: This covers federal, self-employment, and state taxes. Adjust higher if you live in a high-tax state like California or New York.

- Pay quarterly taxes: Payments are due April 15, June 15, September 15, and January 15. Missing these deadlines can result in penalties and interest.

- Track deductions: Expenses like home office use, health insurance, and business-related costs can lower your taxable income, reducing how much you need to save.

- Set up a tax reserve fund: Transfer a percentage of every payment you receive into a separate account to ensure you’re ready for tax deadlines.

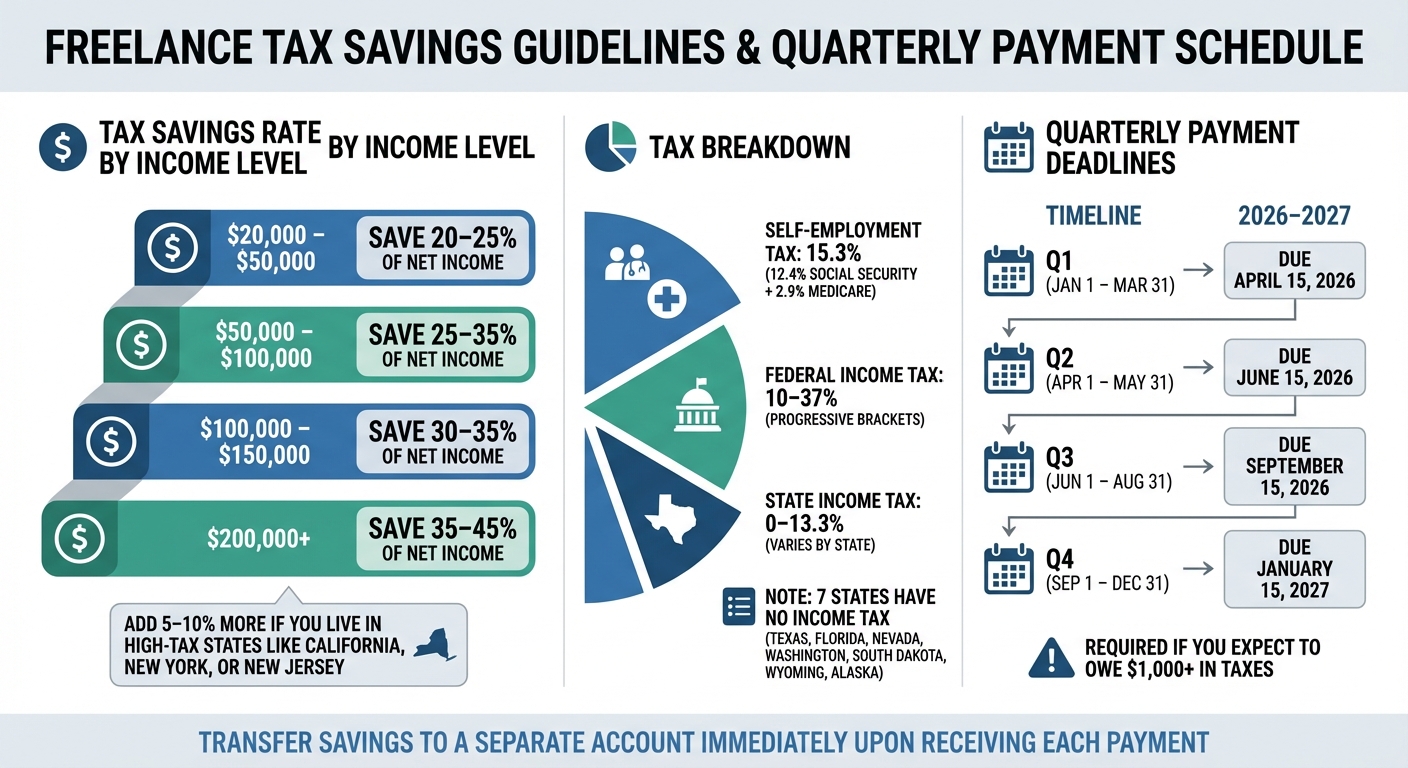

Freelancer Tax Savings Guide: Rates by Income Level and Payment Deadlines

Self-Employed Taxes: How Freelancers Can Prepare

sbb-itb-66f4c95

What Taxes Do Freelancers Need to Pay?

Being clear about your tax responsibilities is crucial for setting aside the right amount each quarter.

Freelancers in the United States are responsible for three key types of taxes: self-employment tax, federal income tax, and state or local taxes. Unlike traditional employees, freelancers handle these taxes entirely on their own since no automatic withholding applies.

Self-Employment Tax Explained

Freelancers are subject to a self-employment (SE) tax rate of 15.3%, which includes 12.4% for Social Security and 2.9% for Medicare.

"When you work for an employer, your company pays half of these taxes and withholds the other half from your paycheck. When you work for yourself, you pay both halves." - Beancount.io

The IRS calculates this tax on 92.35% of your net earnings, not your full income. For 2026, the Social Security portion applies only to the first $184,500 of earnings. However, the 2.9% Medicare tax continues to apply to all income, with an additional 0.9% Medicare surtax for single filers earning above $200,000 or married couples filing jointly earning over $250,000.

One small relief for freelancers is the ability to deduct 50% of your SE tax (the "employer-equivalent" portion) from your gross income when calculating federal income taxes.

Now, let’s look at how federal and state income taxes can further affect your finances.

Federal and State Income Taxes

Federal income tax is applied using progressive tax brackets, ranging from 10% to 37% of your taxable income.

State income taxes, on the other hand, vary significantly depending on where you live. While 43 states have an income tax, seven states - Texas, Florida, Nevada, Washington, South Dakota, Wyoming, and Alaska - don’t impose one. For freelancers in high-tax states like California (13.3%), New York, New Jersey, Oregon, and Minnesota, it’s wise to set aside an additional 8–13% for state taxes.

Some states also require quarterly estimated payments, similar to federal tax obligations. If you work across multiple states or relocate during the year, you may need to file taxes in more than one state.

"Most states also require that you file estimated taxes. When these payments are due and how much you'll have to set aside will vary by your state of residence. You may have to pay estimated taxes to more than one state, depending on where you live and where you earn income." - Paula Pant, The Balance

On top of state and federal taxes, don’t overlook potential local business taxes, franchise taxes (common in states like California and New York), or licensing fees. These can add a surprising amount to your yearly tax bill.

Knowing these tax requirements makes it easier to calculate how much of your income you should reserve for taxes.

How to Calculate How Much to Save for Taxes

Once you're clear on your tax responsibilities, the next step is figuring out exactly how much to set aside from every payment you receive.

Calculate Your Net Income First

Start by determining your net income. This means subtracting eligible business expenses from your gross earnings. Using your net income as the base ensures you’re not setting aside more than necessary, leaving you with enough cash for ongoing business needs.

For instance, if your gross revenue is $90,000 and you have $10,000 in eligible expenses, your net profit comes to $80,000.

Estimate Your Self-Employment and Income Taxes

With your net income calculated, it’s time to determine the taxes you owe.

The IRS doesn’t base self-employment tax on your full net income. Instead, you multiply your net profit by 92.35%. This adjustment accounts for the employer-equivalent share of FICA taxes that typical employees don’t pay.

Here’s an example using an $80,000 net profit:

| Step | Calculation | Result |

|---|---|---|

| 1. Apply 92.35% Factor | $80,000 × 0.9235 | $73,880 (Taxable Base) |

| 2. Social Security Tax | $73,880 × 12.4% | $9,161.12 |

| 3. Medicare Tax | $73,880 × 2.9% | $2,142.52 |

| 4. Total SE Tax | $9,161.12 + $2,142.52 | $11,303.64 |

After calculating your self-employment tax, you’ll also need to account for federal income tax, which is determined using progressive tax brackets. Depending on your state, you might owe state income tax as well. One important thing to note: you can deduct 50% of your self-employment tax (in this case, $5,651.82) from your gross income when figuring out your federal income tax.

Use the 25–35% Savings Guideline

A common rule of thumb is to save 25–35% of your net income for federal tax obligations. This range typically covers both self-employment and income taxes for most freelancers.

The exact percentage you should save depends on factors like your income level, deductions, and state tax rates. If you live in states with higher taxes, such as California, New York, or New Jersey, you might want to increase your savings rate by an additional 5–10%.

| Annual Net Income | Recommended Savings Rate |

|---|---|

| $20,000 – $50,000 | 20–25% |

| $50,000 – $100,000 | 25–35% |

| $100,000 – $150,000 | 30–35% |

| $200,000+ | 35–45% |

To make this process easier, consider automating your savings. Transfer the appropriate percentage of each payment into a separate high-yield savings account. This habit ensures you’re consistently building a tax reserve fund without the stress of last-minute scrambling.

Tax Deductions That Lower Your Savings Target

Business deductions can significantly reduce your taxable income, which means you won’t need to set aside as much for taxes. For instance, if you claim $20,000 in deductions and your combined tax rate is 35%, you could lower your tax bill by $7,000. That’s money you can reinvest in your business instead of sending it to the IRS. Here are some key deductions to help reduce your tax liability.

Home Office Deduction

If you work from home, the IRS allows you to deduct expenses for a space exclusively used for business. You can choose between two calculation methods, depending on which one benefits you more.

- Simplified Method: Multiply the square footage of your office by $5, with a cap of 300 square feet. This results in a maximum deduction of $1,500. It’s straightforward and requires little record-keeping.

- Actual Expense Method: Calculate what percentage of your home is used for business by dividing your office space by your total home square footage. Apply that percentage to actual expenses like rent, mortgage interest, utilities, and repairs. While this method has no dollar limit and could yield a larger deduction, it does require detailed records.

Beyond home office expenses, there are other deductions that can further ease your tax burden.

Other Common Deductible Expenses

- Health Insurance Premiums: Premiums for yourself and your family are fully deductible as an above-the-line adjustment, meaning you don’t need to itemize to claim them.

- Retirement Contributions: Contributions to a SEP-IRA or Solo 401(k) not only build your retirement savings but also lower your taxable income. For 2026, you can contribute up to $72,000 to a SEP-IRA or $24,500 (plus an additional 25% employer contribution) to a Solo 401(k).

- Equipment and Software: Purchases like computers, office furniture, and software subscriptions can be deducted under Section 179, with a limit of $2,560,000 for 2026. Items costing $2,500 or less can be expensed immediately without depreciation.

- Professional Services: Fees for accountants, tax preparers, lawyers, or business coaches are fully deductible.

- Marketing Costs: Expenses such as website hosting, SEO services, social media ads, and business cards are deductible as well.

- Business Travel and Meals: Travel expenses like airfare, hotels, rental cars, tolls, and parking are fully deductible, while meals are deductible at 50%.

- Vehicle Expenses: If you drive for business, you can either deduct the standard mileage rate (72.5 cents per mile for 2026) or calculate actual vehicle expenses based on your business-use percentage. The standard mileage method is generally simpler and works well for freelancers.

- Education: Costs for courses, certifications, or conferences that improve your skills in your current field are fully deductible. Be sure to keep digital copies of receipts, as the IRS now accepts smartphone photos as valid documentation.

How to Make Quarterly Estimated Tax Payments

The U.S. tax system operates on a "pay-as-you-go" basis, meaning taxes are due as income is earned - not just in one lump sum in April. Since freelancers don’t have employers withholding taxes from their paychecks, the IRS requires them to make quarterly estimated tax payments. These payments cover both federal income tax and self-employment tax. If you expect to owe $1,000 or more in taxes for the year, you’re required to make these payments. Failing to pay on time or underpaying can result in an underpayment penalty - even if you’re due a refund when you file your annual return.

To avoid penalties, you need to meet specific payment thresholds: either 90% of the current year’s tax or 100% of last year’s tax (110% if your adjusted gross income exceeded $150,000). Below, we’ll walk through dividing your annual tax liability and choosing the best way to estimate your payments.

Divide Your Annual Tax Into 4 Payments

Start by estimating your total tax liability for the year, then divide it into four equal payments. Submit these payments by the IRS deadlines:

| 2026 Quarter | Income Period | Due Date |

|---|---|---|

| Q1 | January 1 – March 31 | April 15, 2026 |

| Q2 | April 1 – May 31 | June 15, 2026 |

| Q3 | June 1 – August 31 | September 15, 2026 |

| Q4 | September 1 – December 31 | January 15, 2027 |

You can make payments through several methods:

- IRS Direct Pay: A free bank transfer option.

- Electronic Federal Tax Payment System (EFTPS): Lets you schedule payments in advance.

- Mail: Send a check with Form 1040-ES vouchers.

If your income varies significantly throughout the year, consider making smaller weekly or monthly payments to ensure you meet the quarterly total by the deadlines.

Once you’ve divided your tax liability, the next step is deciding how to estimate your payments.

Base Estimates on Last Year or This Year?

You have two main methods for estimating your quarterly payments: using last year’s tax figures or projecting this year’s income.

- Prior-Year Method: This is the simplest option. Take last year’s total tax, divide it by four, and pay that amount each quarter. This method ensures you avoid penalties, even if your income increases significantly. If your adjusted gross income (AGI) last year was $150,000 or less, pay 100% of last year’s tax; if it was higher, pay 110%.

- Current-Year Method: This approach works well if your income has decreased or you’re just starting out. Estimate your total income for the year, subtract deductions, calculate the tax, and divide by four. While this prevents overpaying, it carries the risk of penalties if you underestimate your income.

For those with irregular or seasonal income, the Annualized Income Installment Method (Form 2210 Schedule AI) allows you to calculate payments based on actual earnings during each specific period.

Accurate quarterly payments not only help you avoid penalties but also make managing your cash flow and tax reserves more efficient.

How to Build and Manage a Tax Reserve Fund

Avoiding last-minute stress at tax deadlines starts with making tax planning a regular part of your financial routine. By setting aside money for taxes every time you get paid, you can avoid penalties and cash flow issues. This habit works hand-in-hand with your quarterly estimated payment plan.

Set Aside a Percentage of Every Payment

Every time you receive a payment, immediately transfer a portion of it into a dedicated tax savings account. For instance, if you aim to save 25% to 30% for federal taxes, a $5,000 payment means setting aside $1,250 to $1,500 right away. This method adjusts automatically to your actual income, so there’s no need to predict earnings far in advance.

"The business owners who do the best are the ones who learn to protect themselves… from themselves."

That’s how Sarah York, EA at Keeper, explains it. To make sure you don’t accidentally dip into these savings, consider opening a separate account - ideally at a different bank. This extra step adds a layer of protection, especially during tough months or when unexpected expenses arise.

This approach is particularly helpful for freelancers or anyone with irregular income. For example, after a high-earning month, your tax reserve will grow, providing a cushion for slower periods. This way, you’ll always have funds ready for those quarterly tax bills, keeping your finances on track.

Use Tools to Maintain Steady Cash Flow

Consistent cash flow is key to sticking with your save-as-you-go tax strategy. Late payments from clients can throw off your ability to save and leave you scrambling when taxes are due. Tools like Paid on Time can help by securing payment methods upfront and allowing one-click charges once work is completed. This eliminates the common 30- to 60-day wait for manual invoice processing, ensuring you have predictable income.

Paid on Time also simplifies tax preparation. Its legally binding agreements and detailed payment records make it easy to track exactly when income was received, which is crucial for accurate tax reporting. With a 5% transaction fee and no monthly charges, you only pay when you get paid - making it easier to calculate your net income and set aside the right amount for taxes.

Conclusion

Managing your taxes as a freelancer doesn’t have to be overwhelming. By sticking to the strategies outlined here, you can take control of the process and reduce stress. One of the simplest and most effective habits? Set aside 25–30% of every payment you receive. This ensures you’re always prepared, whether you’ve had a big $10,000 month or a quieter $2,000 one.

Consistency is key. Open a separate savings account specifically for taxes, and treat that money as off-limits. Automating transfers to this account and submitting quarterly payments on time (April 15, June 15, September 15, and January 15) will help you avoid unnecessary penalties from the IRS.

Don’t forget to maximize your deductions. Keep track of all eligible expenses, like home office use, mileage, and other business-related costs, throughout the year. And don’t overlook the 20% Qualified Business Income deduction - it can make a noticeable difference in lowering your taxable income. If your earnings grow beyond certain thresholds, consulting a CPA can help you refine your approach even further.

Planning ahead is your best defense against financial surprises. From setting aside funds to making quarterly payments, these habits create a safety net that protects your business. Tools like Paid on Time can help ensure clients pay promptly, so you can maintain steady cash flow and stick to your savings plan. Pairing this with accounting software gives you a clear picture of your tax obligations in real time.

The key to success? Make tax planning a regular part of your routine. Freelancers who thrive are those who prioritize tax savings, automate the process, and stay disciplined year-round. It’s a small effort that pays off in a big way.

FAQs

How do I choose the right tax savings percentage for my income?

Freelancers are often told to set aside 25-30% of their gross income to cover taxes. This includes self-employment taxes, which are projected to be 15.3% in 2025, as well as income taxes. Some experts recommend saving 25-35% to fully account for all tax obligations. To fine-tune this percentage, you can use a tax calculator or estimate based on your income and filing status. Consistently reserving this amount can help you stay financially ready when tax season rolls around.

What should I do if my freelance income changes a lot during the year?

If your freelance income changes from month to month, it's important to adjust how much you're setting aside for taxes. Aim to regularly recalculate the percentage you save - usually between 25% and 30% - to align with your current earnings. Tax calculators can be a helpful tool to estimate your liability and fine-tune your quarterly payments. Also, keeping thorough records of both your income and expenses will ensure accuracy and help you avoid any unexpected issues when tax season rolls around.

How can I avoid underpayment penalties if I’m new to quarterly taxes?

When it comes to avoiding underpayment penalties, staying on top of your estimated tax payments is crucial. The IRS recommends paying at least 90% of your current year's tax liability or 100% of last year's tax (this increases to 110% if your adjusted gross income (AGI) from the previous year was over $150,000).

To stay compliant, make sure your payments align with the quarterly deadlines: April 15, June 15, September 15, and January 15. If you're unsure about calculating these payments, consulting a tax professional can help you navigate the process smoothly.