Cash Flow Management Tips for Freelancers in 2026

Cash Flow Management Tips for Freelancers in 2026

Managing freelance income can feel unpredictable, but with the right strategies, you can create financial stability in 2026. Here's how to handle common challenges like late payments, irregular earnings, and unexpected expenses:

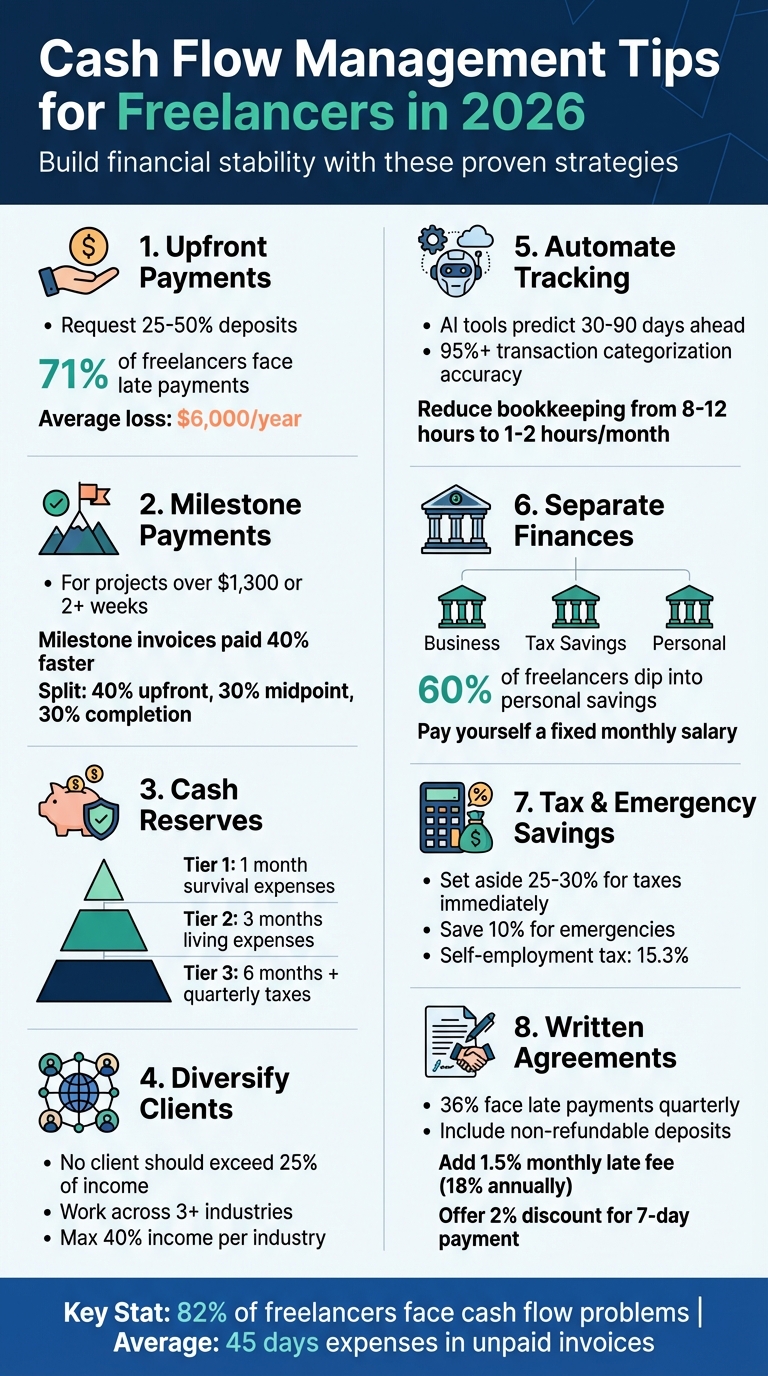

- Upfront Payments: Request 25–50% deposits to secure your finances and client commitment.

- Milestone Payments: Break larger projects into smaller payments tied to deliverables to maintain steady cash flow.

- Cash Reserves: Build a financial buffer in tiers - start with one month of essential expenses, then aim for three to six months.

- Diversify Clients: Avoid relying on one client for more than 25% of your income to reduce risk.

- Automate Finances: Use AI tools for tracking, forecasting, and categorizing income and expenses.

- Separate Finances: Keep business and personal accounts distinct for easier management and tax preparation.

- Plan for Taxes: Set aside 25–30% of every payment for taxes and automate savings for emergencies.

- Written Agreements: Define clear payment terms, include non-refundable deposits, and set late payment penalties in contracts.

These approaches help you stay prepared, avoid financial stress, and focus on growing your freelance business.

8 Cash Flow Management Tips for Freelancers in 2026

Cash Flow Management: How To Never Run Out Of Money | Back To Basics

sbb-itb-66f4c95

1. Get Paid Immediately With Upfront Payment Agreements

Securing upfront payments is one of the best ways to maintain steady cash flow. By asking for a portion of the project fee before starting, you not only protect your finances but also ensure your clients are committed. Typically, requesting a deposit of 25%-50% is a good starting point.

Late payments are a common issue for freelancers - 71% face delays, losing an average of $6,000 each year as a result. In the B2B world, only 52% of invoices are paid on time, with 43% becoming overdue and 5% turning into bad debt. Clients who pay upfront tend to stay more engaged because they’ve already made an investment.

Here’s a real-world example: In early 2026, a freelance product manager implemented a 10% retainer with milestone payments. Within just 90 days, their monthly revenue fluctuations dropped by 45%, allowing them to confidently take on larger projects. The trick? Presenting the deposit professionally. A simple yet effective way to phrase it could be:

"To get your project officially on my calendar and kick off the work, a 50% deposit is required. This reserves your slot exclusively." - Billzy.io

You can also encourage faster payments by offering incentives, like a 2% discount if the client pays the full amount upfront or within 10 days. This approach works well across different scenarios: long-term clients might appreciate the discount, new clients should ideally pay at least half upfront, and for smaller tasks (like a single blog post or consultation), it’s reasonable to ask for full payment before starting.

Upfront payments not only stabilize your income but also let you focus on delivering your best work. For larger projects, combining this with milestone payments can provide even more financial stability.

2. Set Up Milestone Payments for Large Projects

Breaking large projects into milestone payments is a smart way to ensure steady cash flow. Instead of waiting weeks - or even months - for full payment, you can receive funds as you hit specific progress points. The rule of thumb? Use milestone payments for projects worth over $1,300 or lasting more than two weeks. This strategy works well alongside upfront payment agreements, giving you financial stability as the work progresses.

Here’s how to make it effective: tie each payment to a clear, measurable deliverable. For example, instead of vague terms like “halfway through,” use something concrete such as “First draft of all five blog posts delivered.” This avoids confusion and reduces the risk of disputes. It also prevents you from essentially financing your client’s project out of your own pocket, minimizing your financial risk if things go sideways.

Here’s why this matters: 82% of freelancers have faced cash flow problems, and the average freelancer has 45 days’ worth of expenses tied up in unpaid invoices. However, invoices tied to milestones get paid 40% faster than traditional month-end billing, helping you access funds more quickly.

A common approach is to split payments into three stages: 40% upfront, 30% at the midpoint, and 30% upon final delivery. For new or higher-risk clients, you might adjust this to 50% upfront, 25% at the midpoint, and 25% at the end. The golden rule? Follow the 25% Rule, which means never leaving more than 25% of the total fee unpaid when the project wraps up. This keeps you in a stronger position throughout the process.

To further protect yourself, include a work-pause clause in your contract. This clause allows you to stop work if a milestone payment is overdue by more than 7 days [15,16]. Also, set a clear review window - if the client doesn’t provide feedback within 5 business days, the milestone is automatically approved, and the invoice becomes due. These terms, combined with milestone payments, reduce financial interruptions and help you maintain a consistent income throughout your projects. For more professional advice, explore our freelancer tools and guides.

3. Build a Cash Reserve With Priority Tiers

Having a cash reserve can be the difference between thriving as a freelancer and barely getting by. Consider this: 80% of freelancers who depend on gig work as their main income struggle to handle unexpected expenses, and 60% have tapped into personal savings to cover business costs. The key to avoiding this? Build your reserve step by step instead of trying to save it all at once.

Start by figuring out your "survival number" - the bare minimum you need each month for essentials like rent or mortgage, groceries, insurance, debt payments, and critical business expenses. This number forms the foundation of your cash reserve strategy:

- Tier 1: Save one month of survival expenses in your business checking account to cover gaps between payments.

- Tier 2: Build up three months of living expenses in a high-yield savings account to weather slow periods or the loss of a client.

- Tier 3: Aim for six months of expenses, plus one quarter of your estimated taxes. This gives you the freedom to turn down bad deals and invest in opportunities.

Tackle these tiers one at a time. As Beancount.io suggests, don’t overwhelm yourself by trying to save for everything simultaneously. Automate the process by setting aside 10–15% of every client payment into your reserve as soon as you receive it. Keep these savings in a separate high-yield account so they can earn interest while staying out of easy reach.

This isn’t just about numbers - it’s about mindset. Even a small buffer can change how you approach your work. As Landolio explains, "Even a single month's buffer transforms your negotiating psychology. You stop saying yes to everything because you have to and start saying yes to things because you want to". With a Tier 2 or Tier 3 reserve, you’ll feel confident walking away from clients offering poor terms.

If you dip into your reserve during a slow month, make replenishing it a top priority when your next payment comes in. This habit ensures your safety net stays intact, helping you avoid financial stress. Building this reserve is a critical step as you work toward securing a stable freelance income.

4. Work With Multiple Clients to Reduce Income Risk

Once you've secured steady payments through upfront and milestone strategies, the next step is to diversify your client base. Depending on a single client can be risky - 59% of freelancers report inconsistent monthly income due to client concentration risk. If your main client reduces their budget or ends the contract, your income could drop drastically - or even vanish - overnight.

To avoid this, stick to the "25% Rule": no single client should account for more than 25% of your annual revenue. As Beancount.io aptly puts it, "Client concentration is income fragility". Losing a client that makes up 50% of your income can be catastrophic, but losing one contributing 20% is far more manageable. If a client's share of your income starts creeping past that 25% threshold, it's time to seek out new opportunities. This approach not only stabilizes your income but also encourages diversification across industries.

Speaking of industries, don't just focus on having multiple clients - spread your work across different sectors. Aim to keep no more than 40% of your income tied to a single industry, and work with clients from at least three different fields. For example, if you're a designer working exclusively with tech startups, a wave of layoffs could wipe out your client base. But if you're also collaborating with healthcare companies and government agencies - sectors that tend to be more stable during economic downturns - you'll be better protected if one industry falters. Combining this strategy with fintech tools can help keep your cash flow steady and secure.

Beyond industry diversification, structure your client mix to balance stability and growth. A good approach is to pair one or two retainer clients with two or three project-based clients. Retainers provide predictable income to cover your essential expenses, while project-based work offers opportunities for higher earnings and growth. To smooth out cash flow, stagger your invoice dates - for example, on the 1st, 10th, and 20th of the month - so payments arrive consistently. This makes budgeting and financial planning much easier.

Finally, dedicate 2–3 hours each week to business development to ensure you always have new projects in the pipeline. The goal is to secure your next project before your current one ends, avoiding gaps in income that can last 2–6 weeks. As OwnedWork explains, "When you are not desperate for income, you can say no to bad clients, hold firm on your rates, and wait for the right opportunities". By diversifying your client base, you'll gain the flexibility to make better decisions and maintain financial stability.

5. Automate Your Cash Flow Tracking and Forecasting

Keeping your freelance income steady can be a challenge, especially with 59% of freelancers reporting inconsistent monthly earnings. Traditional budgeting methods often fall short in these situations. That’s where automating your cash flow tracking becomes a game-changer. Instead of relying on manual processes, automation provides efficiency and accuracy. By 2026, AI-powered tools are expected to predict cash flow 30–90 days in advance by analyzing outstanding invoices, past payment trends, and scheduled work. This means you’ll know about potential cash shortfalls weeks ahead, giving you time to adjust your expenses or take on extra projects.

The move from reactive to predictive accounting is already happening. Tools like QuickBooks Online use historical data and current invoices to forecast your financial position up to 90 days in advance. Meanwhile, FreshBooks offers a visual cash flow timeline, making it easy to see when payments are expected and when bills are due. For those who want more flexibility, Float allows you to explore "what if" scenarios - like how landing or losing a major client could impact your cash flow. Thanks to machine learning, these tools now categorize transactions with over 95% accuracy, cutting down bookkeeping time from 8–12 hours to just 1–2 hours per month.

To streamline this process even further, connect your bank accounts and payment platforms (like Stripe, PayPal, or Venmo) through services such as Plaid. This integration updates your cash flow data hourly, removing the need for manual data entry. Another helpful tip? Automate your tax savings by directing 25–30% of every incoming payment into a separate account for taxes. This ensures you’re prepared for quarterly tax payments without the stress of last-minute calculations.

"AI can predict your cash flow 30–90 days out. This is incredibly useful for making decisions about taking on new projects or timing big purchases." – SoloStack

It’s also important to keep an eye on your cash runway, which tells you how many months you can operate without new income. Tools like Origin combine income forecasting with AI-powered expense categorization to give you a clear picture of your financial future. For those who prefer more control, Beancount.io offers plain-text accounting with AI insights, ensuring full ownership of your financial data. Pricing for these tools typically ranges from $12 to $35 per month, with budget-friendly options like Wave offering free plans. Investing in these tools can help you avoid cash flow gaps and make smarter financial decisions.

6. Keep Business and Personal Finances Separate

Mixing your business and personal finances isn’t just messy - it can create real headaches when tax season rolls around. A surprising 60% of freelancers have had to dip into personal savings to cover business expenses. This makes it harder to figure out whether your business is actually making money or if you’re just moving funds around that should be set aside for taxes. Separating your finances isn’t just a good habit - it’s an essential step for staying organized and avoiding financial chaos.

Here’s a simple system: open three accounts. Use a Business Checking account for client payments, a Tax Savings account to set aside 25–30% of each payment, and a Personal Checking account for your monthly salary. This setup ensures that tax money stays untouched, gives you a clear picture of your business’s profitability, and makes managing your finances much easier.

Pay yourself a fixed amount from your business account into your personal account each month. This approach helps smooth out the ups and downs of inconsistent income, prevents overspending during good months, and keeps enough money in your business account for taxes, operating costs, or even an emergency fund. By keeping everything separate, you’ll not only have a better handle on your cash flow but also set yourself up for long-term financial stability.

To make this process even easier, consider using tools like Expensify or Wave. These platforms can automatically categorize your transactions with over 95% accuracy. Wave offers free accounting and invoicing features, while Expensify provides a 30-day free trial before switching to paid plans. Setting up these tools now can save you a ton of time - and stress - when tax day comes around.

7. Set Up Automatic Tax and Emergency Savings

When a client payment lands in your account, make it a habit to allocate 30% for taxes and 10% for emergency savings right away - before spending a dime. As a self-employed individual, you're responsible for a 15.3% self-employment tax on top of regular income taxes. Setting aside 25–30% of every payment for taxes is non-negotiable. Moving these funds immediately helps you avoid accidental overspending.

Here’s how to streamline this process and protect your finances: open four separate accounts. Use a Business Operating account to receive all client payments. From there, transfer 30% to a Tax Savings account and 10% to an Emergency Fund account. The rest stays in your Business Operating account for expenses and your monthly "salary", which you can transfer to your Personal account. This system keeps your tax money safe and ensures your emergency fund grows consistently without requiring constant effort.

For your emergency fund, aim to build it in tiers as discussed earlier. Many freelancers stop at Tier 2, but reaching Tier 3 can provide you with the flexibility to decline clients who aren't a good fit and make smarter long-term decisions.

To make this process even easier, consider using automation tools. Platforms like PayTrack (free to $9.90/month) offer AI-powered cash flow forecasting, while QuickBooks Self-Employed ($15/month) provides automated tax estimations. These tools can forecast payment schedules, flag potential cash flow issues, and help you adjust your savings plan as needed. This way, you’ll always stay ahead of your tax obligations and emergency savings goals.

"Cash flow management is the difference between a struggling freelancer and a thriving business owner." - PayTrack Team

8. Use Written Agreements to Define Payment Terms

A written agreement is your best safeguard against cash flow problems. With 36% of freelancers dealing with at least one late payment every quarter, it’s crucial to outline payment terms clearly and in writing. Make sure your contract specifies exactly when payments are due. Use precise terms like "Net 14" or a specific date (e.g., April 15, 2026) instead of ambiguous phrases like "upon completion" [29, 30].

Start every project with a non-refundable deposit. This not only secures initial funds but also helps filter out clients who may not be fully committed. For smaller projects under $500, consider requesting 50–100% upfront. For medium-sized projects ranging from $500 to $5,000, ask for 25–50%. For larger projects exceeding $5,000, 25–33% upfront is a common practice. This approach protects your time and demonstrates that you run a professional business. Clear terms like these set the tone for the entire project, starting with your deposit.

Include a late payment clause in your agreement to establish consequences for delays. For instance, you can charge a 1.5% monthly penalty on overdue balances, which amounts to 18% annually. To encourage prompt payments, offer a 2% discount for invoices paid within seven days [29, 30]. This creates clear expectations and provides leverage if payments are delayed.

"The foundation of your financial stability and professional respect rests upon one critical part of your contract: the Payment Terms." – PactlyApp Blog

Additionally, to protect your cash flow, define revision limits in your contract. Specify how many rounds of revisions are included and outline the process for handling extra changes. This ensures projects don’t get stuck in endless tweaks, holding up your final payment. Clear guidelines like these keep things moving smoothly and protect your bottom line.

Conclusion

Managing freelance cash flow in 2026 doesn't have to feel like an uphill battle. By combining strategies like ensuring timely payments and automating cash flow tracking, you can create a system that brings stability to your income. The right mix of technology and financial discipline can turn the uncertainties of freelance work into something much more manageable.

Today's tools can categorize transactions, provide real-time updates on your cash position, and even automate reminders for overdue payments. It's not about working harder - it's about working smarter by using systems that take the guesswork out of your finances.

Adopting these practices now can fundamentally change your freelance business. Simple steps - like setting aside 25–30% of earnings for taxes, keeping business and personal finances separate, and monitoring your cash runway - can give you the breathing room to make smarter decisions. Managing cash flow isn't about cutting corners; it's about designing a system where your money works for you, not against you.

The bottom line is this: written agreements protect your time, automation conserves your energy, and cash reserves give you freedom. When you can forecast your cash flow weeks in advance, you eliminate the daily stress of financial uncertainty. This empowers you to turn down clients who aren’t a fit, negotiate better terms, and build the steady freelance career you’ve always envisioned. With these tools and strategies, you’re setting yourself up for long-term success.

FAQs

How do I ask for a deposit without losing the client?

To ask for a deposit without risking the client relationship, focus on clear and professional communication. Let the client know that a deposit - usually ranging from 20% to 50% - is a common practice. Emphasize that it benefits both sides by ensuring mutual commitment and setting the foundation for a strong working relationship. Present it as a positive step, not a penalty, and use a friendly tone to reassure them. Highlight how this process helps streamline the project and reflects a professional approach, something most clients value and understand.

What’s the simplest milestone payment schedule to use?

The easiest way for freelancers to set up a milestone payment schedule is by breaking the project into clear stages and requesting payment upon completing each one. This approach helps maintain a consistent cash flow, minimizes financial risk, and eliminates the need to wait until the project's completion for full payment. For best results, outline each phase of the project clearly and send invoices at the end of each stage. This method is particularly effective for larger or multi-phase projects.

How do I estimate quarterly taxes as a freelancer?

To figure out your quarterly tax payments for 2026, start by estimating your expected annual income. From there, calculate both your self-employment taxes and income tax obligations for the year. Once you have the total, divide it into four equal payments to match the IRS deadlines.

Using financial tools to track your revenue and expenses can help ensure your calculations are accurate. Keep in mind, if you anticipate owing $1,000 or more in taxes for the year, you're required to make these quarterly payments to avoid penalties. Staying on top of deadlines is key to staying compliant with IRS rules.