How to Secure Payment Before Starting Work

How to Secure Payment Before Starting Work

Securing payment upfront is essential for protecting your income and avoiding financial risks as a freelancer. Without upfront payments, you may face delayed or unpaid invoices, which can disrupt your cash flow and leave you covering project costs. Here's how to safeguard your earnings effectively:

- Use Clear Contracts: Define scope, payment terms, and deadlines. Include clauses for deposits, late fees, and work stoppages if payments are overdue.

- Request Upfront Deposits: Require 25%-50% of the project fee before starting. This confirms the client’s commitment and reduces risk.

- Leverage Secure Payment Methods: Avoid manual processes. Use platforms like Stripe or tools like Paid on Time to automate invoicing and ensure secure transactions.

- Consider Escrow for High-Risk Projects: For large or risky jobs, escrow services hold funds in trust, releasing them only after work is approved.

Upfront vs. Later: When to Get Paid as a Freelancer

sbb-itb-66f4c95

Create Clear Contracts with Payment Terms

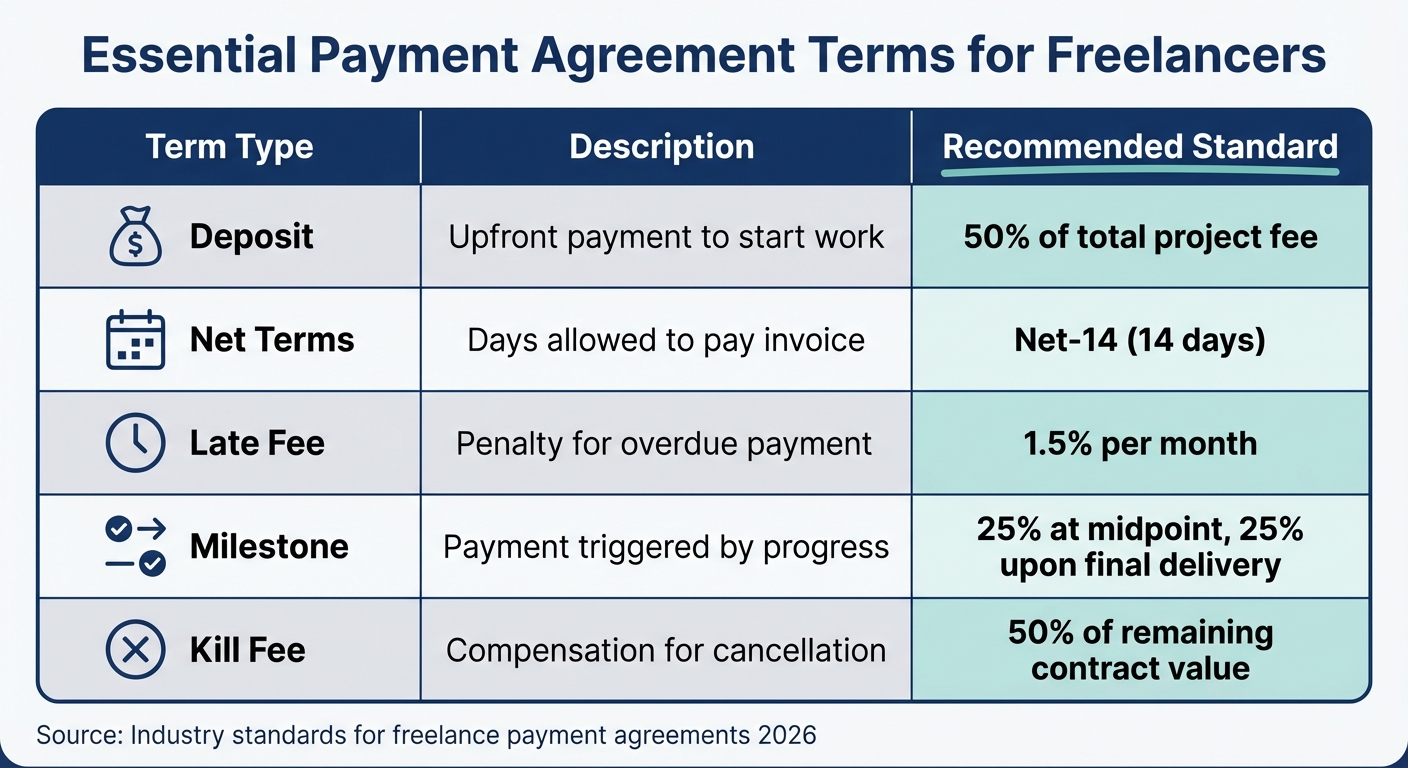

Payment Agreement Terms Guide for Freelancers

A written contract is your financial safety net. Paul Starkman, a Labor and Employment Attorney at Clark Hill, sums it up perfectly:

"Every significant freelance job deserves a written freelance contract. Without one, you open yourself up to potential disputes about all aspects of the job."

The stats back this up: in 2026, 47% of freelancers faced payment delays or disputes, many of which could have been avoided with clear contracts. Skipping a contract leaves you without legal protection if things go south.

Contracts are more than just paperwork - they set expectations upfront. They outline what you’ll deliver, when you’ll deliver it, and how much you’ll be paid. This clarity helps prevent surprises when it’s time to invoice and reduces disagreements about the project’s scope. Christopher Collins, Partner at Yugo Collins, explains:

"Contract terms almost always favor the drafter [since] the drafter sets terms that favor their own interests."

Here’s what you should include in your payment agreement to protect yourself.

What to Include in a Payment Agreement

Your contract should spell out payment terms clearly, leaving no room for misinterpretation. Start with a detailed scope of work that defines exactly what you’re delivering - this includes the number of revisions, file formats, and deadlines (using MM/DD/YYYY format, like 03/15/2026). This avoids "scope creep", where clients expect extra work without additional payment.

Next, include a clear payment schedule to protect your cash flow. Specify whether you’re billing hourly, by fixed price, or based on milestones. Use familiar U.S. terms like Net-7, Net-14, or Net-30, which indicate payment is due within 7, 14, or 30 days of the invoice date. Many freelancers now prefer shorter terms - Net-14 or Net-7 - to ensure quicker payments.

| Term Type | Description | Recommended Standard |

|---|---|---|

| Deposit | Upfront payment to start work | 50% of total project fee |

| Net Terms | Days allowed to pay invoice | Net-14 (14 days) |

| Late Fee | Penalty for overdue payment | 1.5% per month |

| Milestone | Payment triggered by progress | 25% at midpoint, 25% upon final delivery |

| Kill Fee | Compensation for cancellation | 50% of remaining contract value |

Deposits are non-negotiable - require 25% to 50% upfront before starting work. Developer Matt Fulton shares this warning:

"If a client is reluctant to pay a deposit, this may be a sign that they’ll be reluctant to pay future invoices once work is complete."

To encourage timely payment, include a late payment penalty clause. A common rate is 1.5% monthly interest on overdue invoices, though you can adjust it between 1% and 5% depending on your preference. You can also incentivize early payments by offering discounts - like "2/10 Net 30", which gives a 2% discount if the client pays within 10 days, with the full amount due in 30 days.

Another critical addition is a work stoppage clause. This ensures you can pause work if payments are overdue. Make it clear that intellectual property rights only transfer to the client once final payment is received. This prevents clients from using your work without proper compensation.

Finally, list accepted payment methods (such as ACH transfers, credit cards, or wire transfers) and state all amounts in US dollars. Consider adding a "kill fee" clause - typically 50% of the remaining contract value - to protect yourself if the client cancels midway. For modern contracts in 2026, you might also want to include clauses on AI tool usage and ownership of AI-generated work.

How Contracts Protect Your Business

A signed contract creates legal accountability, ensuring your cash flow stays steady and giving you a clear path to resolve disputes if a client refuses to pay. Without one, you’re left relying solely on the client’s goodwill, which is risky when disagreements arise. The contract serves as enforceable proof of what both parties agreed upon.

Contracts also eliminate misunderstandings by defining what “completion” means. Avoid vague terms like “due on sign-off” and instead specify “due on completion of work” to sidestep delays caused by lengthy internal reviews.

Additionally, contracts establish your status as an independent contractor rather than an employee. This distinction protects you and the client from tax and benefit complications. Including a jurisdiction clause - like “This agreement shall be governed by the laws of New York” - helps simplify legal proceedings in case of a dispute.

Though hiring a professional to draft your contract might cost a few hundred dollars, it’s worth the investment. A well-written contract can save you from losing income and dealing with legal headaches. It’s not just a document - it’s a shield for your business.

Collect Secure Payment Methods Before Work Begins

Getting secure payment details upfront is just as critical as having a signed contract. Without verified payment information, you risk completing work without ever getting paid. The numbers back this up: 74% of freelancers report not being paid on time, and 85% have faced late payments at least occasionally.

By collecting payment details before starting a project, you achieve two things. First, it confirms the client is serious and capable of paying. Second, it prevents the hassle of chasing down payment details after delivering the work. Sean Gallagher, CEO of Gallagher Website Design, emphasizes:

"Don't start a project unless you received 1/2 upfront or at least some partial payment."

The process should be handled securely and professionally to reassure clients about sharing their financial details. This step also sets the stage for smooth, automated payment transactions.

How to Verify Payment Details Securely

Requesting sensitive payment details via email is a major no-go. Not only does it expose both parties to security risks, but it also violates payment industry standards. Instead, rely on secure payment processors that handle encryption and validation for you.

Platforms like Stripe are a great option. They allow you to send secure payment links, validate card details, and detect fraud during checkout - all while being PCI DSS compliant. This ensures sensitive data is encrypted and securely stored.

Offering multiple payment methods can speed up the process. Research shows that 80% of clients prefer credit cards, while 59% opt for debit cards. For larger invoices, consider ACH bank transfers - they generally cost less, with fees around 1.5%, compared to roughly 2.9% plus $0.25 for card transactions. Automating invoicing further enhances security and simplifies the payment process.

For new clients, requiring an upfront deposit confirms their ability to pay and shows their commitment to the project. If a client hesitates or refuses to provide even a partial deposit, it’s a warning sign about their reliability.

Stephanie Allen, CEO of AirWorks Solutions, saw immediate benefits with this approach:

"The most effective strategy I've implemented is requiring 50% deposits before any major equipment installation begins."

For instance, on a $6,000 project, she collected $3,000 upfront and offered a 2% discount for payments made within 10 days. This incentive worked - 60% of her clients took advantage of the early payment discount.

Problems with Manual Payment Processes

Even with secure verification, manual payment methods can create headaches. Processes like emailed invoices, mailed checks, or manual bank transfers are prone to delays and errors. Many businesses end up spending a significant chunk of their time chasing overdue payments.

Manual processes also lack transparency. Without features like automated tracking or read receipts, it’s hard to confirm whether an invoice was received, leading to endless follow-ups.

Delays are another issue. Paper checks can take days to arrive and clear, while manual bank transfers often take three to five days - or, in extreme cases, up to 72 days.

Automated systems solve these problems by streamlining the process. Features like "Pay Now" buttons embedded in invoices and automated reminders - sent three days before, on the due date, and seven days after - help ensure timely payments. Some platforms report that 90% of invoices processed through their systems are paid on time or early, compared to the industry average, where 72% of freelancers deal with unpaid invoices.

Damon Delcoro, Founder of UltraWeb Marketing, learned this the hard way when a Miami restaurant client took 75 days to pay a $15,000 invoice. He switched to "Due Upon Receipt" terms with automated reminders and saw a dramatic improvement:

"The psychological trick that changed everything was switching to retainer agreements for ongoing SEO work... This eliminated 90% of my payment headaches and improved cash flow dramatically."

Use Paid on Time for Legally Binding Agreements and Secure Payments

Paid on Time combines contracts, invoicing, and secure payments into a single platform, eliminating the hassle of managing multiple tools. This integration addresses common gaps that lead to payment issues, ensuring smoother operations for freelancers and small businesses.

The platform tackles a widespread issue: over 77% of freelancers face late or non-paying clients, with an average loss of $6,000 annually due to unpaid invoices. By securing both the agreement and payment method upfront, Paid on Time automates the process, making payments predictable and stress-free.

One standout feature is the card-on-file authorization. Unlike traditional methods that rely on manual invoicing and follow-ups, this system ensures funds are transferred directly and on schedule. No need for constant reminders or chasing payments.

Paid on Time operates on a simple pricing model: a 5% transaction fee with no monthly costs. You only pay when you get paid. This aligns the platform’s goals with yours, offering a streamlined solution for legally binding agreements, secure payments, and effortless charging.

How to Set Up Paid on Time

Setting up Paid on Time is straightforward and designed for efficiency. Start by creating an account and entering basic business details, including your bank information for deposits. Then, use the platform’s AI-guided interface to draft a professional contract. Answer a few project-specific questions, and you’ll have a contract ready to customize. You can adjust clauses for scope of work, intellectual property rights, and late fee penalties - key safeguards against common disputes like scope creep.

Once the agreement is finalized, both you and your client can review, edit, and electronically sign it directly on the platform. After signing, the system generates a secure payment link for your client. They can enter their credit or debit card details through an encrypted checkout page, with their information safely stored for future billing. The card-on-file setup allows for one-click charging once the project is complete, ensuring quick and reliable payment transfers.

Benefits of Paid on Time vs. Manual Methods

Switching from manual payment methods to an automated system like Paid on Time offers clear advantages. Manual processes often involve delays, errors, and time-consuming follow-ups, while automation simplifies everything from invoicing to payment collection.

| Feature | Manual Payment Methods | Paid on Time |

|---|---|---|

| Processing Speed | Slow – requires manual invoicing and follow-ups | Fast – one-click charging for quick transfers |

| Cash Flow Predictability | Unpredictable – reliant on manual actions | Predictable – payments processed on schedule |

| Administrative Time | Hours spent on invoicing and reminders | Minutes – automation handles the tasks |

| Payment Accuracy | Prone to typos and miscalculations | Automated systems ensure accuracy |

| Security | Vulnerable to unprotected records | Encrypted storage and multi-factor authentication |

| Dispute Resolution | Difficult due to scattered communications | Clear records with legally binding contracts |

By automating payment processes, Paid on Time reduces the time spent on invoicing from hours to minutes, allowing you to focus on your work. Advanced security features, like encrypted storage and multi-factor authentication, protect both you and your clients from potential risks.

Moreover, the platform eliminates the awkwardness of chasing payments. With automatic billing triggered upon project completion, you can avoid uncomfortable reminders and maintain a professional relationship with your clients. These benefits make Paid on Time a valuable tool for freelancers and small businesses alike. Up next, we’ll explore how escrow services can safeguard high-risk projects.

Use Escrow Services for High-Risk Projects

When tackling high-risk projects, escrow services can be a game-changer for securing payment. They act as a safety net, holding funds in trust until the work is completed and approved. An escrow agent - a neutral third party - manages the funds, ensuring they’re only released once both sides meet the agreed terms.

"An 'escrow' is a compromise between the two parties in a transaction. It's an agreement between the parties where something being transferred (usually money) leaves the hands of the sending party but is held in trust by a third party... before being delivered to the receiving party." - J. Gerard Legagneur, Attorney

Escrow services are especially useful for large-scale projects, new client relationships where trust is still being built, or international transactions where legal enforcement might be tricky. If a client doesn’t approve or request changes within 14 days of submission, the funds are automatically released to the freelancer. Typically, escrow fees hover around 1% of the transaction amount, though smaller deals may have a flat fee instead.

How to Add Escrow to Your Contracts

To integrate escrow into your workflow, start by choosing a reliable escrow agent. This could be a financial institution specializing in escrow or an attorney with a dedicated trust account. Look for agents with a solid reputation and FDIC-insured holdings. Your escrow agreement should clearly outline the agent’s role, fees, and the conditions for releasing funds - whether to you or back to the client.

For bigger projects, breaking the work into milestones can make escrow even more effective. Each milestone should have a specific deliverable and payment amount. This setup ensures steady cash flow and reduces the risk of doing extensive work without payment. Be sure to specify in your contract who will cover escrow fees and any additional costs, like bank wiring or administrative charges.

Before starting any work, confirm that the funds have been deposited into the escrow account. Submit your work through the escrow platform’s designated system to trigger payment countdowns and keep an official record of the transaction. It’s also wise to handle all communications and file deliveries within the platform to ensure there’s evidence in case of disputes.

By following these steps, escrow can do more than just protect your payment - it can also streamline your project workflow.

When to Use Escrow Services

Escrow services are most valuable when the stakes are high enough that losing payment would seriously hurt your business. They’re ideal for projects worth several thousand dollars or more, especially when working with new clients who lack a payment history or verifiable reviews. If a client has a track record of late or missed payments, escrow is a smart precaution. It’s also a must for international projects, where legal challenges can complicate payment recovery.

If your project involves significant upfront costs - like buying equipment, hiring subcontractors, or committing a lot of time - escrow ensures you won’t be left footing the bill if the client vanishes. Additionally, if a client is hesitant to pay the full amount upfront, escrow offers a middle ground by securing funds before the work begins.

Conclusion: Secure Your Payments and Protect Your Business

Getting paid on time shouldn't be a gamble. By combining clear contracts with upfront deposits, you're not just safeguarding your income - you’re setting a professional tone that serious clients appreciate. Consider this: 71% of freelancers face payment collection issues at least once in their careers. That’s not just a statistic; it’s missed opportunities to pay bills, invest in equipment, or grow your business.

The strategies outlined here - detailed contracts, upfront deposits, and escrow services - work together to minimize payment risks. Start with a solid contract, secure an upfront deposit, and for larger or riskier projects, consider escrow to ensure funds are held until deliverables are approved. For everyday tasks, tools like Paid on Time simplify the process by enabling one-click payments upon delivery. For high-stakes or international projects, escrow provides an extra layer of security.

As FreshBooks puts it:

"View deposits as a tool for filtering out customers your business doesn't need and attracting those you do: Those who pay well, pay on time, and are a pleasure to work with." - FreshBooks

But the benefits go beyond just securing payment. When clients invest upfront, they’re more engaged, provide quicker feedback, and take the project seriously. This means less time chasing invoices and more time focusing on what you love to do. Considering that 82% of businesses fail due to cash flow problems, securing payment isn’t just a good idea - it’s a necessity.

FAQs

How do I ask for a deposit without losing the client?

To ask for a deposit while keeping the client comfortable, approach the conversation with professionalism and clarity. Let them know the deposit is necessary to secure their project, handle upfront expenses, and confirm their commitment. Present it as a normal business practice, typically ranging between 20-50% of the total cost, depending on the size and complexity of the work. Use a polite and respectful tone, give straightforward payment instructions, and emphasize your commitment to delivering exceptional results.

What should I do if a client won’t sign a contract or pay upfront?

If a client hesitates to sign a contract or pay upfront, it’s crucial to protect yourself from potential risks. Be upfront about why upfront payments or deposits are essential - they provide security for both you and the client. One option is to suggest a partial deposit or propose using an escrow service as a compromise. If the client still resists, hold off on beginning the project until you’ve reached an agreement on terms. Establishing clear policies and expectations from the start can help prevent misunderstandings down the road.

When is escrow worth using instead of a deposit?

Escrow works well when extra security is necessary - think new clients, big projects, or international deals. Unlike a standard deposit, escrow involves a neutral third party holding the funds until specific conditions are met. This means payment is only released once the work is completed to everyone's satisfaction. It’s a smart way to minimize risk and create trust, especially when payment reliability might be a concern.