Late Payment Solutions for Small Business Owners

Late Payment Solutions for Small Business Owners

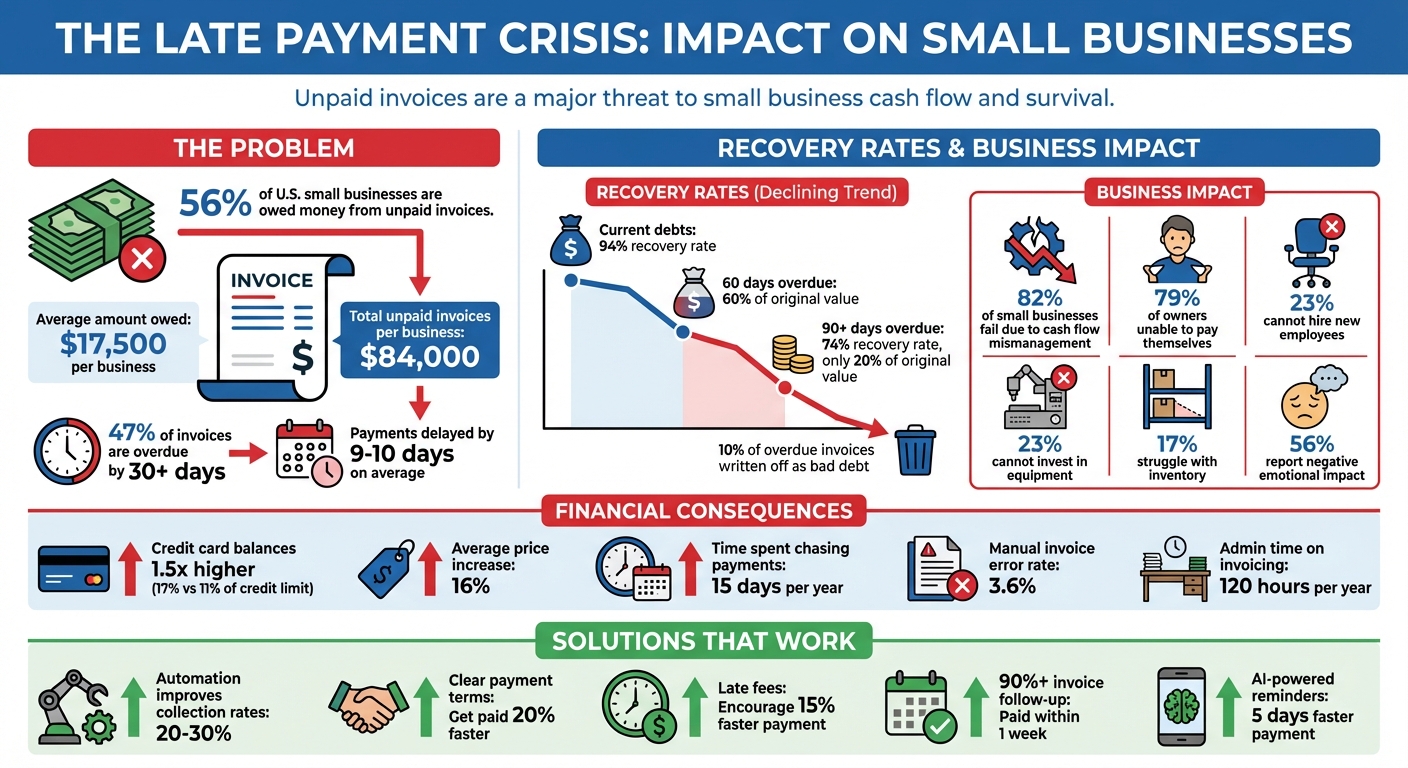

Late payments are a major issue for small business owners, with 56% of U.S. small businesses owed money from unpaid invoices, averaging $17,500 per business. These delays disrupt cash flow, hinder growth, and force tough financial decisions. Key insights include:

- 47% of invoices are overdue by over 30 days, and payments are delayed by 9–10 days on average.

- Businesses recover only 74% of debts overdue by 90+ days, compared to 94% of current debts.

- Late payments lead to higher credit card reliance and price increases, with 10% of overdue invoices written off as bad debt.

To address this, small business owners can take action:

- Automate invoicing and reminders: Saves time and improves collection rates by up to 30%.

- Set clear payment terms: Define due dates, accepted methods, and penalties upfront.

- Charge late fees: Encourages on-time payments; common rates are 1–1.5% monthly interest.

- Track payment history: Identify and prioritize reliable clients while managing riskier ones.

Tools like Paid on Time simplify the process by securing client payment details upfront, creating legally binding agreements, and charging only a 5% transaction fee without monthly costs. These strategies help ensure steady cash flow and reduce the stress of chasing overdue payments.

Key takeaway: Proactive measures like automation, clear terms, and late fees are essential to minimize late payments and maintain financial stability.

Late Payment Statistics and Impact on Small Businesses

How Late Payments Hurt Small Businesses

Financial Damage from Late Payments

Late payments can wreak havoc on a small business's financial health. Cash flow mismanagement is a leading cause of failure for 82% of small businesses, and overdue invoices are a big part of the problem. The longer an invoice goes unpaid, the less valuable it becomes - after 60 days, it may only retain 60% of its value, and by 90 days, that figure drops to just 20%.

The ripple effects of late payments are staggering. Nearly 79% of small business owners report being unable to pay themselves due to overdue invoices. This financial strain extends to other critical areas: 23% cannot hire new employees, another 23% are unable to invest in essential equipment, and 17% struggle to maintain or expand their inventory. The longer payments are delayed, the harder it becomes to collect. While businesses typically recover 94% of current debts, that rate plummets to 74% for balances over 90 days overdue.

Late payments also push businesses into tough financial decisions. Companies dealing with delayed payments carry credit card balances that are 1.5 times higher than businesses with fewer delays - 17% of their credit limit compared to 11%. To compensate, many are forced to raise their prices, with an average increase of 16%. Worse yet, about 10% of late payments are never recovered and are written off as bad debt. These financial hits make it harder to manage day-to-day operations and plan for growth.

Day-to-Day Problems from Unpredictable Payments

When payments are unpredictable, covering basic expenses like rent, utilities, and payroll becomes a constant juggling act. Instead of focusing on growth, business owners are stuck putting out fires. Using an agreement-backed payment platform can prevent these fires by securing payment terms before work begins.

Chasing overdue payments is a massive time drain. On average, small business owners spend 15 days each year trying to collect on late invoices. This time could be better spent on activities that generate revenue. Delayed payments also create a domino effect - if you can’t pay your vendors on time, it can damage your reputation, hurt your credit score, and strain relationships you’ve worked hard to build.

The stress of managing cash flow issues takes a toll beyond the balance sheet. More than half (56%) of small business owners say these financial challenges negatively impact their emotional well-being. To avoid falling into this cycle, implementing strategies like proven methods to get clients to pay on time is essential.

sbb-itb-66f4c95

How to Get Paid & Charge Late Fees | Guide to Invoicing and Avoiding Late Payments

How to Prevent and Handle Late Payments

Late payments can disrupt your cash flow, but the good news is they’re not unavoidable. By taking proactive steps - like setting clear expectations, automating routine processes, and enforcing consequences - you can significantly reduce the likelihood of overdue invoices. The trick is to plan ahead, so you’re not left scrambling when payments don’t come through on time.

Set Up Automated Invoicing and Payment Reminders

Manually handling invoices is not only time-consuming but also prone to errors. Small business owners spend around 120 hours a year on administrative tasks like invoicing, and manual invoices have an error rate of about 3.6%, which can lead to disputes and delays.

Automation can make a huge difference. For instance, businesses that follow up on 90% or more of their invoices often get paid within a week of the due date. Plus, automated reminders can boost collection rates by 20–30%, and AI-powered reminders help businesses get paid 5 days faster on average.

Here’s a good reminder schedule to follow:

- Send a friendly notice 7 days before the due date.

- Follow up with a firm reminder on the due date.

- Send an urgent notice with a direct payment link 3–7 days after.

Including "Pay Now" buttons in your emails can make it easy for clients to settle their bills instantly. For recurring payments, set up automatic invoices that go out monthly, quarterly, or at intervals that suit your business model.

It’s also smart to set invoice due dates a few days earlier than when you actually need the funds. This accounts for ACH processing times, which usually take 2–4 business days.

To complement automation, make sure your payment terms are crystal clear.

Define Clear Payment Terms in Your Contracts

Vague contracts are a breeding ground for late payments. For example, if your agreement says “payment upon completion” but doesn’t define what “completion” means, you’re leaving room for disputes. Businesses with clear payment terms get paid 20% faster than those with vague or missing terms.

"Most payment disputes start with unclear expectations, not bad intent." - Greg Mitchell, Legal consultant at AI Lawyer

Use straightforward language in your contracts. Clearly state the due date, accepted payment methods (like ACH, credit cards, or wire transfers), and the penalties for late payments. Avoid jargon like "Net 30" and instead write something like, "Payment is due within 30 days of the invoice date".

For bigger projects (over $2,000), consider requiring a 25% to 50% deposit upfront. This not only secures client commitment but also helps cover initial expenses.

Another helpful clause is to require clients to flag any billing issues within 7–14 days. This prevents disputes from being used as an excuse for delayed payments. And remember, invoices with direct payment links are paid twice as fast as those without.

Once you’ve set clear terms, enforcing them becomes much easier, especially with late fees in place.

Charge Late Fees to Encourage On-Time Payments

Late fees can be a powerful motivator. Even if you never actually charge the fee, just including a late fee policy on your invoice can encourage clients to pay up to 15% faster.

Most small businesses charge between 1% and 2% monthly interest on overdue balances, with 1.5% being the most common rate for service-based industries. For smaller invoices, a flat fee of $25–$50 might be more practical. Before setting your rates, check your state’s usury laws to ensure you’re within legal limits.

To legally enforce late fees, they must be spelled out in both your contract and your invoices. If you’re introducing a late fee policy for existing clients, give them advance notice via email or a phone call. Use professional phrasing like, "A late fee of 1.5% applies to overdue payments", rather than making it sound like a personal penalty.

Many businesses also offer a 1–5 day grace period after the due date to account for bank processing times before applying the fee.

Using Paid on Time for Legally Binding Payment Agreements

Traditional invoicing can leave you exposed - 60% of invoices are paid late. This forces you into the frustrating process of chasing overdue payments. Paid on Time changes the game by collecting your client’s payment details upfront and creating a legally binding agreement. This agreement clearly outlines payment terms, deadlines, and penalties. The result? A smoother transition from completing your work to getting paid.

How Paid on Time Secures Payments Before You Start Work

Paid on Time simplifies the payment process by securing your client’s payment details before you even begin. It establishes a legally binding agreement that ensures both parties are on the same page about payment expectations. With this in place, you can focus entirely on your project without worrying about delayed payments.

Charge Clients with One Click After Finishing Work

Once your project is done, getting paid is as easy as a single click. This eliminates the typical wait time - which averages 28.7 days for invoices, with payments often arriving 9–10 days late. No more waiting around or sending reminders.

Pay Only 5% Per Transaction with No Monthly Fees

Forget about monthly subscription fees that traditional invoicing tools charge, whether you get paid or not. Paid on Time operates on a pay-only-when-paid model, charging just a 5% fee per transaction. No recurring costs mean you can secure payments and keep your cash flow steady without unnecessary expenses.

Track Payment History and Choose Better Clients

Keeping an eye on how clients handle payments is crucial for securing your cash flow. Did you know that 82% of small businesses fail because of cash flow problems? One big reason is working with clients who habitually pay late - or not at all. On average, small businesses are stuck with $84,000 in unpaid invoices.

Monitor Client Payment Patterns with Payment Tracking

Your accounting software is your best friend here. Use it to create aging reports every week. These reports categorize unpaid invoices into 30, 60, and 90+ day segments, making it crystal clear which clients are falling behind. Keep detailed records of all communication about overdue payments - this documentation can be a lifesaver if legal action becomes necessary.

Pay close attention if your accounts receivable start growing faster than your sales. This could signal an increase in payment risks. Here's a sobering fact: the chance of collecting payment drops from 94% for current debts to 74% for those overdue by 90 days. And after 60 days, an overdue invoice might only be worth 60% of its original value. The longer an invoice sits unpaid, the less likely you'll recover the full amount.

These insights not only help you chase payments but also guide you in deciding which clients deserve your time and effort.

Refine Client Relationships Based on Payment Reliability

Combining payment tracking with automated reminders and clear terms can greatly improve cash flow management. For new clients, consider starting them on "Payment on Receipt" terms or requiring a 25%–50% upfront deposit until they establish a track record of reliability. For larger contracts, running a credit check through agencies like Experian, TransUnion, or D&B is a smart move. It could save you from months of chasing overdue invoices.

Over time, use your payment data to create a tiered system for clients. Offer perks like Net 15 or Net 30 terms to your most reliable clients - those who consistently pay on time. For clients who are habitually late, switch to cash-on-delivery terms or require milestone payments. And if a client repeatedly ignores deadlines despite reminders, it’s time to stop working with them altogether. As small business expert Barry Moltz puts it:

"Giving a customer credit is a privilege, not a right".

Your time, energy, and resources are far too valuable to waste on clients who don’t respect your payment terms. Focus on building relationships with clients who value your work and pay you on time.

Conclusion

Managing payments effectively is critical for keeping your business afloat. Late payments aren't just small setbacks - they can jeopardize your entire operation. Tools like automated invoicing, clear payment terms, late fees, and diligent payment tracking are essential for maintaining a steady cash flow and ensuring your business runs smoothly.

Acting early to prevent late payments is essential. Shortening payment terms and using digital invoicing with direct payment links can help speed up collections. Automated reminders, on the other hand, can significantly improve recovery rates, ensuring you get paid faster.

For example, Paid on Time offers a practical solution by securing payment details upfront and simplifying billing after the work is done. With a 5% per transaction fee and no monthly costs, it eliminates the uncertainty of starting work without guaranteed payment.

FAQs

When should I stop following up and send an overdue invoice to collections?

You might want to think about turning an overdue invoice over to collections if multiple polite reminders and reasonable follow-up efforts haven’t worked. Many small businesses typically wait 30 to 60 days past the due date before taking this step. Having clear contracts in place that include late fee terms can help set expectations from the start and provide a framework for deciding when to escalate if payments remain outstanding despite persistent follow-ups.

What late fees can I legally charge in the U.S.?

In the U.S., late fees can be charged as long as they are agreed upon in writing before the work starts. These fees usually fall within a range of 5% to 10% annually or a flat fee of $25–$50. However, the exact limits depend on state laws. It's crucial to review your state's specific regulations to ensure compliance before adding late fees.

How do I qualify clients for Net 15 or Net 30 terms?

To offer clients Net 15 or Net 30 payment terms, it’s important to evaluate their credit history and payment habits. Clients who consistently pay on time, demonstrate financial stability, and maintain solid business partnerships are typically good candidates for these terms. For clients who are newer or less established, it’s wise to begin with shorter terms like Net 7 or require upfront payment to minimize risk. Keep an eye on their payment patterns over time, and consider extending longer terms only to those who prove dependable.