How to Get Clients to Pay on Time: 7 Proven Methods

How to Get Clients to Pay on Time: 7 Proven Methods

Late payments can hurt your business. Here’s how you can reduce them and improve cash flow:

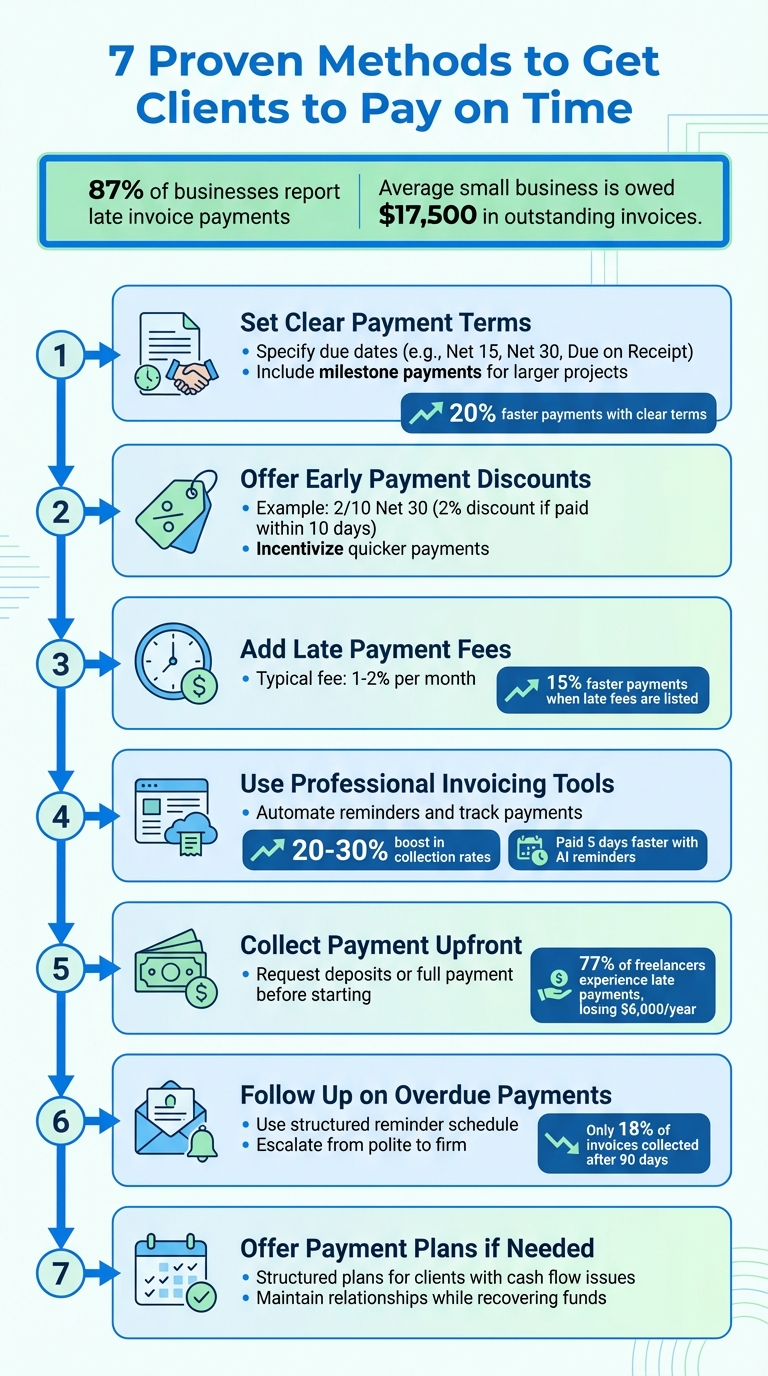

- Set Clear Payment Terms: Specify due dates (e.g., "March 15, 2026") and acceptable methods upfront in contracts. Include milestone payments for larger projects.

- Offer Early Payment Discounts: Encourage quicker payments with incentives like "2/10 Net 30" (2% discount if paid within 10 days).

- Add Late Payment Fees: Clearly state penalties (e.g., 1.5% monthly) in contracts to deter delays.

- Use Professional Invoicing Tools: Automate reminders and track payments for efficiency.

- Collect Payment Upfront: Request deposits or full payment before starting work to ensure steady cash flow.

- Follow Up on Overdue Payments: Use a structured reminder schedule, escalating from polite emails to firm notices.

- Offer Payment Plans if Needed: For clients facing financial issues, structured plans can recover funds while maintaining the relationship.

7 Proven Methods to Get Clients to Pay on Time

How to get paid faster in 2026 | Payment terms, payment reminders, & invoicing tips

sbb-itb-66f4c95

Set Clear Payment Terms in Your Contracts

Getting paid on time starts well before you send out an invoice. If you don’t have written payment terms in place, you’re essentially offering your services on credit. As Matt Fulton from Freelancers Union puts it:

"You are not a bank, do not work on credit. Or at least, minimize how much work you do on credit".

Your contract should spell out exactly when payment is due. Common terms include Net 15 (payment due 15 days after the invoice date), Net 30 (30 days), or Due on Receipt (immediate payment). Research shows that businesses with clear payment terms get paid 20% faster than those with vague or missing terms. To avoid confusion, always include a specific calendar date on your invoices, like "Due: March 15, 2026", so clients know exactly when the clock starts ticking.

In addition to deadlines, your contract should address acceptable payment methods - such as ACH, credit cards, or wire transfers - and outline milestone payments for larger projects. For example, you could break a project into stages, requiring 50% upfront, 25% midway, and 25% upon completion. Another option is to retain a secure payment method on file for automatic billing once the work is done. For ongoing work, consider using a retainer model, where clients pay upfront on a recurring basis. This approach not only secures your time but also creates a consistent income stream.

By incorporating these strategies into your contracts, you can protect your cash flow and reduce the stress of chasing payments. Clear payment terms also lay the groundwork for smoother invoicing and follow-ups.

Specify Payment Deadlines and Discounts

Clear deadlines create urgency. Avoid vague phrases like "payment due soon" and instead use terms such as Net 30 or include an exact due date. For instance, "Payment due by March 15, 2026" leaves no room for interpretation. While Net 30 is a common standard in business-to-business transactions, Net 15 may be a better option if you need faster payments. For smaller projects or new clients, Due on Receipt ensures immediate payment.

To encourage early payments, you might offer a discount. A popular example is 2/10 Net 30, where the client gets a 2% discount if they pay within 10 days, while the full amount remains due in 30 days. This small incentive can make a big difference in how quickly you get paid.

Add Late Payment Fees

Deadlines are essential, but penalties can reinforce them. Late fees serve as a deterrent, encouraging clients to pay on time. In fact, just listing a late fee on your invoice can lead to payments being made 15% faster, even if you never actually charge the fee. A typical late fee ranges from 1% to 2% of the outstanding balance per month. For example, a 1.5% monthly fee adds up to about an 18% annual rate.

It’s important to include late fee terms in your contract before starting the work. Once a payment is overdue, you can’t legally impose fees unless they were agreed upon beforehand. A clear statement like, "A late fee of 1.5% per month will be applied to any unpaid balance after the due date", sets expectations upfront. Be sure to check your state’s laws, as some limit the maximum interest rate you can charge.

Another effective clause to include is a work-stop provision. This allows you to pause all work immediately if a payment is missed, giving clients extra motivation to resolve any billing issues without delay.

Use Professional Invoicing and Payment Systems

Relying on manual invoicing can eat up your time and lead to mistakes, while a professional system takes care of repetitive tasks and lets you focus on your work.

Here’s a telling statistic: 87% of businesses report that their invoices are paid after the due date. And in Europe, businesses spend about 29% of their working year chasing overdue payments. A professional invoicing system helps you stay on top of this by organizing invoices based on due dates and payment status. This makes it easy to spot late-payers and prioritize the invoices that need immediate attention.

Some platforms go a step further by securing payment details upfront. This way, you can charge clients immediately after completing the work, avoiding the hassle of sending an invoice and waiting for payment. This approach not only improves cash flow but also reduces the chances of disputes over payments.

Another benefit? These systems keep detailed records of all invoicing and payment communications, which can be a lifesaver if you ever need to escalate an issue. As John Rampton, Entrepreneur and Investor, puts it:

"There is something to be said for having a machine doing the nagging (follow-up) for you!"

And that’s not all - these systems can even automate follow-ups, saving you even more time.

Automate Payment Reminders

Automated reminders are a simple way to keep clients on track without adding to your workload. These systems track the status of invoices and send reminders at key intervals, ensuring your payment terms are consistently reinforced. Plus, they can scale effortlessly as your client list grows.

The results speak for themselves: automating reminders can boost collection rates by 20–30%, and businesses using AI-powered reminders get paid an average of five days faster. To maximize effectiveness, set up a multi-stage reminder schedule. For example:

- A friendly reminder seven days before the due date

- A firm nudge on the due date

- Additional follow-ups three days and one to two weeks after the due date

Including a "Pay Now" button in these reminders can speed up payments significantly - up to four times faster than traditional methods.

It’s important to keep these reminders professional yet personal. Mention the client’s name and invoice details to maintain a good relationship. As Ben Brigden from Teamwork.com advises:

"The goal is to incentivize clients to pay on time, not drive them away."

Offer Multiple Payment Methods

Making payments easy for your clients is key to getting paid on time. Offering multiple options - like ACH transfers, credit cards, and digital wallets such as Apple Pay or Venmo - removes common excuses, such as not having a checkbook or dealing with banking restrictions.

This flexibility can also help clients manage their own cash flow. For instance, a client who can’t pay immediately via bank transfer might be able to settle the bill using a credit card. For recurring clients, auto-pay options ensure payments are processed automatically on the due date, eliminating the need for manual action.

The numbers back this up: 16% of business invoices go unpaid altogether, and 37% aren’t paid until more than 30 days past their due date. By offering diverse payment methods and embedding "Pay Now" buttons in your invoices, you make it easier for clients to pay promptly. As John Rampton notes:

"Offering more ways to pay leaves a client with very little excuses not to pay on time."

Collect Payment Information Before Starting Work

After establishing clear contract terms, the next critical step is securing payment details before beginning any project. This practice shields you from the risks of late or missed payments, a problem that affects 77% of freelancers, costing them an average of $6,000 annually.

Collecting payment upfront - whether through credit card authorization, a 50% deposit, or full payment - not only ensures steady cash flow but also spares you the hassle of chasing down payments later. Freelance designer and consultant Matt Olpinski emphasizes this point succinctly:

"The money effectively becomes the contract."

For smaller projects under $5,000, requesting 100% payment upfront is a smart move. For mid-range projects between $5,000 and $10,000, a 50/50 payment split works well. Larger projects exceeding $10,000 benefit from a tiered payment structure, such as 50% upfront, 25% mid-project, and 25% upon completion. To incentivize early payments, you could even offer a 10% discount for clients who pay the full amount upfront.

It’s essential to hold off on scheduling the project until the deposit or payment clears your account. For recurring clients, setting up automatic payments on specific dates can simplify the process, eliminating the need for manual invoicing while ensuring a steady cash flow.

Tools like Paid on Time streamline this process by enabling you to create legally binding agreements and securely store payment details before starting work. Once the project wraps up, you can charge the client with a single click, allowing for immediate payment upon completion. This proactive approach ensures smoother payment handling and helps set the tone for a professional and efficient working relationship.

Follow Up on Overdue Payments Consistently

After setting clear contracts and securing deposits, consistent follow-up becomes the backbone of recovering overdue payments. It's this steady approach that helps maintain your cash flow and keeps your business running without interruptions.

On average, U.S. small businesses are owed around $17,500 in outstanding invoices. The secret to recovering these payments? It's not about being pushy or confrontational. Instead, a calm, specific, and consistent follow-up process works best.

The aim here isn’t to argue or embarrass a client. In most cases, late payments are just administrative hiccups. As Quick Invoice Tool explains:

"The goal isn't to 'win' an argument. The goal is to move your invoice through the client's process with clarity, consistency, and a calm tone."

Timing is also critical. Statistics show that only 18% of invoices are successfully collected after 90 days past due. Worse, the likelihood of recovering payment drops by 60% after three months. This is why having a structured, escalating follow-up plan is non-negotiable.

Create a Follow-Up Schedule

A follow-up schedule provides a clear, step-by-step plan for addressing late payments. Start with a polite tone and gradually become firmer as the delay continues. Below is a proven framework for escalating follow-ups:

| Days Past Due | Action | Tone & Approach |

|---|---|---|

| Day 1–3 | First reminder email | Polite; assume it was an oversight |

| Day 7 | Second follow-up email | Factual; request a payment date and offer to resend the invoice |

| Day 10–14 | Escalation email | Direct; reach out to the accounts payable contact directly |

| Day 14–21 | Pause Notice | Firm; notify the client that work is paused until payment is received |

| Day 30+ | Final notice | Serious; mention late fees and potential third-party collection |

In early reminders, always reattach the invoice as a PDF and include key details like the invoice number and due date in the subject line. This approach eliminates the common "I can't find it" excuse and makes it easier for busy clients to locate payment information. If emails go unanswered for two weeks or more, switch to a phone call. A quick conversation often resolves issues that get lost in crowded inboxes.

For delays stretching into the 14–21 day range, set clear boundaries by pausing work. Frame this as a standard business policy rather than a personal action. For instance:

"Our policy is to pause active projects when invoices exceed 14 days past due. Once the outstanding balance is settled, we'll resume immediately."

Following this schedule not only increases your chances of payment but also sets professional boundaries that protect your time and resources.

Document All Payment Communications

In addition to following a structured timeline, thorough documentation is essential. Keeping a detailed record of every interaction about payments serves as both good organization and critical protection. Should you need to escalate the matter legally or involve a collection agency, this documentation will be your strongest evidence.

For every follow-up, log the date, time, method of contact (email, phone, text), and the person you spoke with - whether that’s the project lead, a manager, or someone in accounts payable. If the client provides a payment timeline, disputes the invoice, or explains the delay (e.g., a missing purchase order), record those details too. If you're using invoicing software, note whether the client has viewed the invoice email, as this confirms receipt.

Additionally, retain copies of the original signed contract, all invoices sent, and any payment plans or extensions you’ve agreed to. This comprehensive paper trail ensures accountability and protects your claims in case of legal action. As QuickBooks puts it:

"A well-crafted email keeps the conversation professional without damaging the client relationship... It creates a crucial written record of your communication."

Tools like Paid on Time can simplify this process by automatically tracking all payment-related communications and organizing them alongside contracts and invoices. With everything stored in one place, you’ll always know who owes you, how much, and the status of your follow-up efforts.

Offer Payment Plans When Appropriate

Another way to address unpaid invoices is by offering payment plans, especially when clients are dealing with short-term cash flow issues. If a client can't pay the full amount upfront, a structured plan can help you recover at least part of the payment instead of losing it entirely.

Here’s a sobering fact: 16% of business invoices go unpaid, and 37% aren't paid until more than 30 days after submission. Temporary financial setbacks - like delayed funding, seasonal slowdowns, or unexpected expenses - can make it hard for clients to pay in full. Offering a payment plan in these situations can be a practical solution. As Stripe explains:

"It's often better to bring some consistent money in than wait indefinitely for a lump sum that might not arrive."

When a client is upfront about their financial challenges and has a good track record of paying on time, a payment plan shows flexibility without compromising your bottom line. John Rampton from Entrepreneur suggests:

"To show that you understand their changes and to solidify the value you place on the relationship, you can discuss options for payment plans or agree to different payment terms for a temporary period of time."

For larger or long-term projects, milestone-based billing can break down hefty invoices into smaller, more manageable chunks. Instead of waiting to bill a large amount at the project's end, tie payments to specific deliverables. A common approach is 50% upfront and 50% upon completion, which reduces risk and helps cover initial costs. Alternatively, switching to biweekly billing cycles can make payments easier for clients while improving your cash flow.

For ongoing work, consider moving to a retainer agreement. This ensures predictable monthly income and simplifies budgeting for both you and your client. Whatever payment structure you choose, document all details - dates, amounts, and milestones - in writing. Tools like Paid on Time can help automate reminders and track payments, making the process smoother for everyone involved. This strategy not only helps recover overdue funds but also strengthens your financial planning in the long run.

Send Demand Letters and Take Legal Action If Necessary

When repeated follow-ups don’t result in payment, it may be time to consider legal action. Protecting your cash flow sometimes means taking stronger steps, especially when unpaid invoices pile up. Sending a formal demand letter is often the first move in this direction. This letter serves as a clear signal that you intend to recover the outstanding amount. If that fails, legal action might be your only option. To put things into perspective, in 2024, half of all B2B invoices in the U.S. were overdue, and small businesses were owed an average of $17,500 each for unpaid invoices. These numbers highlight the importance of acting decisively when necessary.

Typically, businesses wait 60 to 90 days after an invoice’s due date before escalating the situation[29,26]. But before reaching this point, make sure you’ve tried every internal option - like sending reminders, making phone calls, or following up multiple times. Legal action should be your last resort, reserved for clients who either refuse to pay or have completely stopped responding despite being able to settle their debt. This step complements earlier efforts by providing a formal path to recover unpaid funds.

Write a Formal Demand Letter

A demand letter is a final attempt to collect payment before involving third parties or pursuing legal action. Attorney Brette Sember, J.D., explains:

"A demand letter - or debt collection letter - is the first step in collecting a debt that is owed to you."

Your demand letter should include the following:

- Clear identification of both parties: Include names, addresses, and contact information.

- Details of the agreement: Summarize the contract terms and reference the unpaid invoice.

- Total amount due: Specify the amount owed, including any late fees.

- Firm deadline: Set a payment deadline, usually 10–14 days.

- Consequences of non-payment: State that failure to pay will lead to legal action.

Make sure to include payment instructions, such as accepted methods like bank transfers, credit cards, or online portals. Attach copies of the invoice and any relevant contract documents to back up your claim. Send the letter via certified mail with a return receipt to have proof of delivery. Keeping the tone professional can also encourage payment. As Sember notes:

"In many cases, simply writing the demand letter lets the debtor know you're serious about collecting and they will pay without your having to go to court."

Know Your Legal Options

If the demand letter doesn’t work, you have two main legal options: hiring a collection agency or filing a case in small claims court.

- Collection agencies charge between 25% and 50% of the recovered amount[26,33]. They’re most effective for older debts (90 to 120 days overdue) when the client has stopped responding entirely[29,33]. While they handle follow-ups and negotiations, keep in mind that you’ll only receive a portion of the recovered funds.

- Small claims court is another option, especially for debts that fall within your state’s jurisdictional limits - usually between $2,500 and $25,000. Filing fees are affordable, ranging from $35 to $150, and you can often represent yourself in straightforward cases of non-payment.

Before pursuing legal action, confirm the debtor’s financial standing. Winning a judgment doesn’t guarantee immediate payment - you might still need tools like wage garnishment, bank levies, or property liens to recover the money. Some jurisdictions, such as New York City, even have laws like the "Freelance Isn’t Free" act, which allows freelancers to recover double damages and attorney fees if they win a non-payment case.

To avoid reaching this stage, tools like Paid on Time can help you secure payment methods upfront and establish legally binding agreements before starting work. However, if all other efforts fail, don’t hesitate to take the necessary steps to recover what you’re owed. Legal action is your safety net to protect your cash flow.

Conclusion

Paying attention to the strategies discussed earlier can make timely payments a consistent part of your business operations. Getting clients to pay on time doesn’t have to feel like an uphill battle. The steps outlined here work together to safeguard your cash flow and ease the burden of chasing overdue invoices. Each approach targets a specific stage of the payment process, creating a system that’s both reliable and effective.

The statistics highlight the challenge: 87% of businesses report late invoice payments, and 59% of freelancers are owed $50,000 or more in overdue payments. But you can flip the script. By applying these strategies, you shift from reactive chasing to proactive management. As writer Precious Oboidhe notes:

"Once you and a client sign a contract... payment is a standard contract term. This mindset shift lets you view payment requests as business communication, not a confrontation."

Start with the essentials: written contracts, automated invoicing, and upfront deposits. These steps alone can resolve many payment issues. Then, build on that foundation with additional tactics such as offering multiple payment options, providing early payment incentives, and maintaining a consistent follow-up routine. This makes it easier - and more appealing - for clients to pay you promptly.

By streamlining your payment process, you not only ensure timely payments but also create a steady cash flow system. The benefits go beyond receiving money faster. Predictable cash flow means you can handle payroll and other expenses without delays, plan for growth confidently, and free up time previously spent on administrative tasks. You’ll also feel less stress when you eliminate the constant chase for overdue payments. Tools like Paid on Time can help simplify this process by securing payment details upfront and formalizing agreements before work begins.

Don’t wait. Take a close look at your payment process, identify gaps, and start implementing two or three strategies right now. Your financial health - and your peace of mind - are worth it.

FAQs

What payment terms should I use for new clients?

Establishing clear and straightforward payment terms is essential for ensuring timely payments. Specify due dates, accepted payment methods, and any penalties for late payments or discounts for early payments. Opting for shorter terms, such as Net 30 or even less, can encourage faster payments.

Make sure these terms are included in both contracts and invoices to align expectations right from the start. Additionally, offering options like upfront deposits or milestone-based billing can motivate clients to stay on schedule. The key is to communicate these terms clearly and transparently to avoid misunderstandings and ensure prompt payments from new clients.

What’s a fair late fee that’s legal in my state?

Late fees typically range between 5% and 10% annually or may be a flat rate, such as $25, depending on the state. To enforce a late fee, most states require it to be clearly stated in a written contract. Make sure to review your state’s laws to stay compliant and include these terms in your agreements to prevent potential disputes.

When should I send a demand letter for an unpaid invoice?

When follow-ups and reminders don’t lead to payment, it’s time to send a demand letter. This step is usually taken when an invoice is long overdue but before escalating to legal action. A demand letter acts as a formal notice, highlighting the urgency of the situation and encouraging the client to settle the payment to avoid further complications.