Invoice vs Payment Agreement: Which One Do You Need?

Invoice vs Payment Agreement: Which One Do You Need?

When managing payments, understanding the difference between invoices and payment agreements is crucial. Here's the quick takeaway:

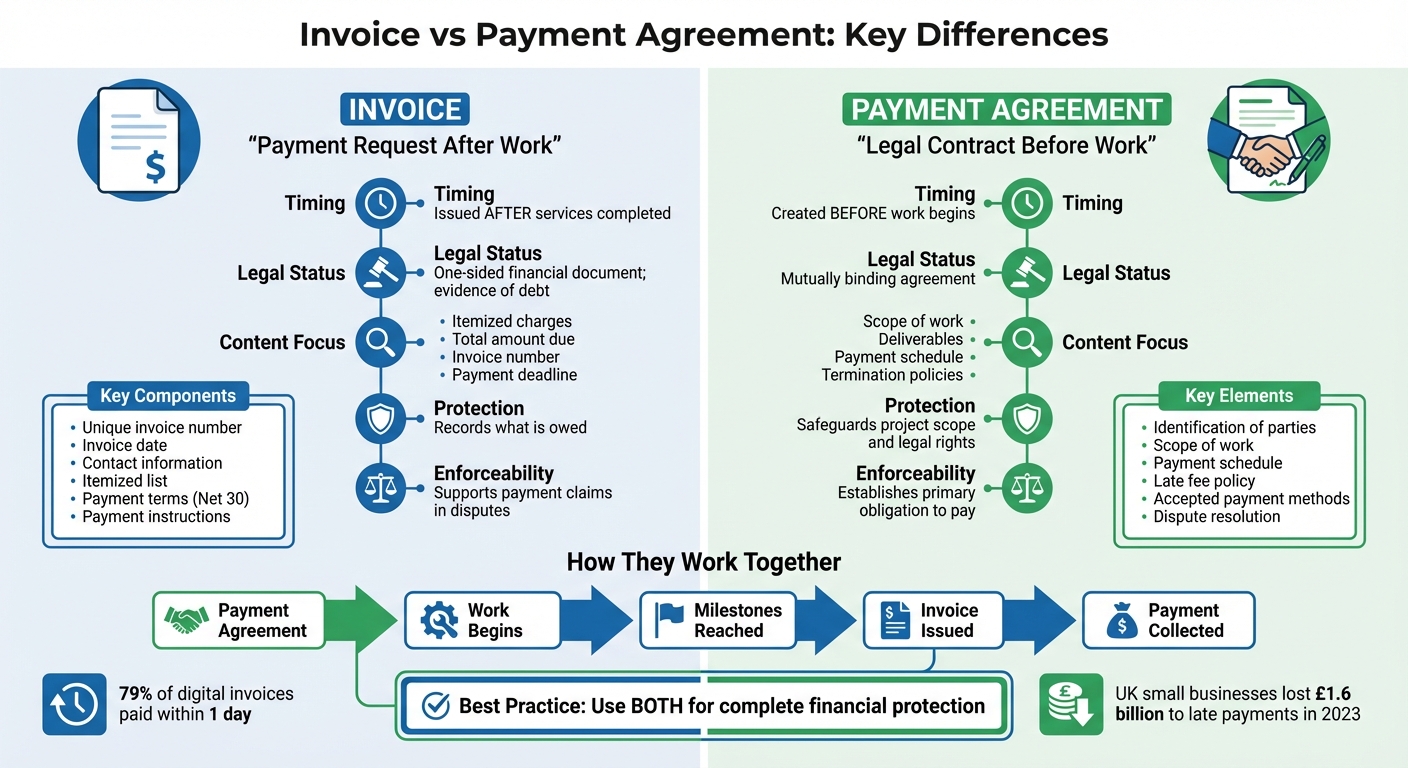

- Invoice: A formal payment request sent after delivering goods or services. It includes details like the amount owed, payment terms, and instructions.

- Payment Agreement: A legally binding contract created before work begins. It outlines the scope of work, payment schedule, deadlines, and penalties for missed payments.

Key Differences:

- Timing: Payment agreements set terms upfront; invoices follow completed work.

- Purpose: Agreements establish legal obligations; invoices record and request payment.

- Content: Agreements define scope, terms, and penalties; invoices focus on itemized charges and total due.

Best Practice: Use both. A payment agreement protects your business by setting clear expectations, while invoices ensure timely payment and provide a financial record.

Quick Tip: Always send invoices promptly (within 24 hours) and include clear payment instructions to avoid delays.

An Invoice is Not a Contract

sbb-itb-66f4c95

What Is an Invoice?

An invoice is a formal document that a seller provides to a buyer after delivering goods or completing a service. It serves as an official request for payment and kicks off the payment process.

"Think of an invoice as your official payment request. Once you deliver goods or finish a service, the invoice creates a legal obligation for the customer to pay the amount specified." – Vivek Shankar, Paystand

Invoices go beyond simply requesting payment. They are a cornerstone of financial management, offering a clear record for tracking revenue, filing taxes, and maintaining accurate accounting records.

Key Components of an Invoice

A well-prepared invoice should include all the necessary details to eliminate confusion and ensure timely payments. Here’s what to include:

- Unique Invoice Number: For easy tracking (e.g., INV-001).

- Invoice Date: Indicates when the payment clock starts ticking.

- Contact Information: Complete details for both you and the client.

- Itemized List of Products/Services: Include quantities, descriptions, and unit prices.

- Financial Breakdown: Show the subtotal, taxes, and total amount due.

- Payment Terms: Use clear terms like "Net 30" or "Due upon receipt."

- Payment Instructions: Outline accepted methods such as bank transfers, credit cards, or online payment links.

Purpose of an Invoice

Invoices are essential for maintaining a formal record of accounts receivable. While they don’t serve as contracts, they create a clear payment obligation and can be used as evidence to recover unpaid debts. For tax compliance, businesses are generally required to keep invoice records for 3 to 7 years.

Switching to digital invoicing can speed up the process - 79% of PayPal invoices are paid within a day. Sending invoices promptly, ideally within 24 hours of completing the work, keeps the transaction fresh in your client’s mind and helps improve cash flow.

Next, we’ll look at payment agreements and how they differ from invoices.

What Is a Payment Agreement?

A payment agreement is a legally binding contract that outlines financial terms before any work begins. Think of it as the playbook for your business relationship - it sets the rules for how much will be paid, when payments are due, and what happens if someone doesn’t hold up their end of the deal.

"A payment agreement is the proactive plan you create before work begins, outlining how and when those invoices will be sent and paid." – Sirion

Unlike an invoice, which comes after services are delivered, a payment agreement establishes expectations upfront. This clarity helps avoid confusion and disputes over payment terms. For instance, in 2023, small businesses in the UK lost about £1.6 billion due to late payments. A clear payment agreement can help businesses steer clear of such costly issues.

But it’s not just about the numbers. A payment agreement also explains why money is owed, sets deadlines, and outlines what happens if payments are missed. This documentation can be a lifesaver if you ever need to enforce the agreement legally or remind a client of the agreed-upon terms. Now, let’s look at the key elements that make a payment agreement work.

Key Elements of a Payment Agreement

To be effective and enforceable, a payment agreement should include these essential components:

- Identification of Parties: Clearly list the full names and addresses of everyone involved.

- Scope of Work: Provide detailed descriptions of the work or deliverables to avoid misunderstandings or "scope creep."

- Payment Schedule: Define specific payment dates or milestones (e.g., "50% due upon signing, 50% due after final approval"). Include terms like "Net 30" to clarify deadlines.

- Late Fee Policy: Outline penalties for late payments, such as interest charges or flat fees after a grace period.

- Accepted Payment Methods: Specify how payments can be made (e.g., ACH transfer, credit card, wire transfer) and include any necessary instructions.

- Dispute Resolution: Detail how disputes will be handled, whether through mediation, arbitration, or a specific legal jurisdiction.

For example, in June 2009, West Central Cooperative signed an "Extended Payment Terms Agreement" with REG Ralston, LLC for soybean oil feedstock. This contract required wire transfers within 45 days of invoice delivery and set a maximum credit limit. If the balance exceeded the limit, West Central could halt deliveries. The agreement also included a security interest clause to protect against defaults.

When to Use a Payment Agreement

Payment agreements are particularly important in situations where financial risk is higher. They’re a must for:

- High-value projects: When significant amounts of money are involved, clear terms help protect both parties.

- Long-term retainers: For ongoing services, payment agreements ensure consistent cash flow.

- New clients: When working with someone who doesn’t have an established payment history, a formal agreement provides peace of mind.

- Custom or upfront investments: Projects requiring significant upfront resources need written terms to safeguard your business.

For international transactions, payment agreements become even more critical. They should specify the payment currency (often USD) and clarify who covers conversion or transfer fees. In milestone-based projects, like construction or website development, linking payments to specific deliverables ensures steady cash flow throughout the project instead of waiting until the end.

A payment agreement turns vague promises into clear, enforceable processes with deadlines and consequences. Knowing when and how to use one is key to maintaining cash flow and setting clear expectations with your clients.

Invoice vs Payment Agreement: Key Differences

Invoice vs Payment Agreement: Key Differences and When to Use Each

Now that we’ve covered what each document is, let’s dive into how they differ. Both are essential for managing payments, but they serve distinct purposes.

A payment agreement is a legally binding contract that sets up a mutual obligation to pay before any work begins. On the other hand, an invoice is a one-sided request for payment issued after work is completed or milestones are achieved. Essentially, the payment agreement lays the groundwork, while the invoice acts as a reminder of those terms.

"A payment agreement defines the obligation; payment terms define the mechanics." – Greg Mitchell, Legal Consultant, AI Lawyer

Timing is another key distinction. A payment agreement is prepared before the project starts to establish expectations, while an invoice is issued after the work is done or a milestone is reached, signaling the client to pay. If disputes arise, the terms in the payment agreement take precedence over the invoice in legal contexts.

Comparison Table: Invoice vs Payment Agreement

| Feature | Invoice | Payment Agreement |

|---|---|---|

| Legal Status | One-sided financial document; evidence of debt | Mutually binding agreement |

| Timing | Issued after services or milestones are completed | Created before work begins |

| Content Focus | Itemized charges, total due, invoice number, and payment deadline | Scope of work, deliverables, deadlines, and termination policies |

| Protection | Records what is owed | Safeguards project scope and legal rights |

| Enforceability | Supports claims for payment in disputes | Establishes the primary obligation to pay |

While these documents serve different purposes, they work together to ensure clear communication and protect your financial interests.

How They Work Together

When used together, these documents create a solid framework for managing payments. The payment agreement defines the terms of the relationship, giving you legal recourse if a client defaults. Meanwhile, the invoice provides a detailed record for accounting, taxes, and debt recovery.

Most payment disputes arise from unclear expectations rather than bad intentions. By setting clear terms in a payment agreement and issuing invoices that align with those terms (such as specifying "Net 30" payment deadlines), you minimize misunderstandings and improve cash flow.

Throughout a project, these two documents complement each other. For example, your payment agreement might require an upfront deposit with the remainder due upon project completion. As milestones are reached, issuing invoices that reference the original agreement creates a seamless connection between what was agreed upon and what is owed. This approach strengthens your ability to collect payments efficiently and keeps everything on track.

Practical Applications for Freelancers and Small Businesses

Discover ways to secure income and simplify project management. These strategies are designed to build on earlier insights, offering actionable steps for freelancers and small businesses to maintain financial stability and streamline operations.

Using Payment Agreements to Set Clear Terms

Start every client relationship with a written agreement that lays out specific terms. Avoid vague language and instead use concrete details. For example, say, "Final payment of $2,500 due within 15 days of project delivery on March 15, 2026", rather than "Final payment due when finished."

Including a late fee - such as 1.5%–2% per month - can encourage timely payments. Research indicates that simply mentioning late fees can lead to payments being made 15% faster, even if you never enforce the fees.

For larger projects exceeding $2,000, consider breaking payments into installments. A common structure is 50% upfront, 25% at the midpoint, and 25% upon completion. Additionally, offering early payment incentives, like "2/10 Net 30" (a 2% discount if paid within 10 days), can improve cash flow.

Issuing Invoices for Payment Collection

Once terms are agreed upon, timely invoicing is crucial to ensure payments are collected. Send invoices within 24 hours of completing the work. Be sure to include key details like a unique invoice number, a clear breakdown of services, the total amount in U.S. dollars, and a specific due date. Invoices issued promptly - within a day - are paid up to three times faster than those sent after a week.

Adding a "Pay Now" button can further speed up the process. Invoices with direct payment links are settled twice as fast as those requiring manual steps. While platforms like PayPal (3.49% + $0.49 per transaction) or Stripe (2.9% + $0.30 per transaction) charge fees, the added convenience and quicker payments often outweigh the costs.

Automated reminders can also reduce the need for manual follow-ups. A good schedule might include a reminder seven days before the due date, another on the due date, and additional follow-ups at three, seven, and 30 days overdue.

Benefits of Combining Invoices and Payment Agreements

Using both payment agreements and invoices together reduces misunderstandings and ensures clarity. Invoices serve as detailed records for taxes and accounting, while payment agreements establish clear expectations from the outset.

Late payments are a common issue - over 50% of small business owners identify them as their main cash flow challenge, with 80% citing stress related to cash flow. Often, these delays result from unclear terms rather than bad intentions. By clearly outlining expectations in a payment agreement and aligning invoices with those terms, you can minimize confusion and delays.

This approach also strengthens client relationships. When everything is documented upfront, clients know exactly what to expect - what they’re paying for and when. With deliverables linked directly to the agreement, there’s less room for misunderstandings or unexpected charges. This reduces the risk of scope creep, ensures faster payments, and allows you to focus more on your work without unnecessary distractions.

Conclusion: Choosing the Right Tools for Financial Security

Key Takeaways

Invoices and payment agreements each play a crucial role in your financial dealings. While a payment agreement establishes the legal framework and outlines deliverables before the work begins, an invoice acts as the formal request for payment and documents the transaction once the work is completed or a milestone is achieved.

When used together, these tools remove ambiguity and reduce the risk of payment disputes. Clear documentation is the foundation of financial stability.

The agreement safeguards your time and scope, while the invoice secures your payment. A solid contract helps prevent scope creep without additional compensation, and an invoice provides the necessary paper trail for tax purposes, audits, or legal disputes. Together, they offer both legal protection and operational clarity.

These practices ensure smooth, enforceable financial interactions.

Next Steps for Implementation

Use these strategies to solidify your financial processes. These tools can help you streamline payment collection and establish trust with your clients.

Put it into action with your next project. Before starting, draft a payment agreement that clearly outlines deliverables, payment amounts in U.S. dollars, deadlines, and any late fees. Once the work is done, send an invoice that reflects those terms.

Take a moment to evaluate your current client relationships. If any lack formal documentation, consider introducing a payment agreement - even for ongoing projects. This step ensures alignment and protects both parties. Consistency is key to managing financial expectations. A simple one-page agreement is far better than relying on verbal commitments, and a basic invoice is much more dependable than an informal payment request. The goal is to clearly outline your terms, as Mitchell wisely points out:

"Money moves faster when the rules are specific and written down".

FAQs

Can I get paid without a signed payment agreement?

Yes, you can still get paid without a signed payment agreement. However, having one in place offers clear payment terms, protects both parties involved, and minimizes the risk of disputes. A signed agreement lays out expectations and provides a sense of security, making it simpler to handle any issues that might come up.

What should I do if a client disputes an invoice?

If a client raises concerns about an invoice, it's important to respond quickly - preferably within 24 hours - and maintain a calm, professional tone. Take the time to understand their concerns, carefully review the invoice for any inaccuracies, and provide supporting documentation if necessary. Should you discover an error, correct it promptly to address the issue. Timely and transparent communication is key to preserving trust and ensuring the matter is resolved smoothly.

How do I set late fees that are enforceable?

To implement enforceable late fees, make sure your invoice or payment agreement includes clear and legally compliant terms. Spell out the exact fee amount or percentage, the payment deadline, and the penalties for overdue payments. Double-check that your fees align with state laws and are reasonable to steer clear of potential legal troubles. It's also important to communicate these terms upfront and apply them consistently. This approach not only ensures enforceability but also helps maintain trust and strong relationships with your clients.