Best Practices for Freelance Income Projections

Best Practices for Freelance Income Projections

Freelancers often struggle with unpredictable income, making financial planning challenging. Here's how to take control of your finances:

- Use past income data: Analyze 6–12 months of earnings to spot trends and calculate your average monthly income. Budget for expenses using your lowest-earning month to stay prepared for slow periods.

- Track current workload: Separate confirmed projects from potential leads. Use confidence percentages to estimate income from new opportunities and avoid overestimating.

- Forecast with methods: Try rolling averages for consistency, weighted probabilities for dynamic estimates, or scenario planning to prepare for best, worst, and likely outcomes.

- Account for external factors: Monitor market trends, inflation, and client risks. Diversify your client base to reduce reliance on any single source of income.

- Leverage tools: Use accounting software like QuickBooks or Wave for tracking and forecasting. Tools like Paid on Time can help ensure timely payments.

Freelancer Budget: How To Budget An Unpredictable Income

sbb-itb-66f4c95

Using Past Income Data

Looking at past earnings is a key step in creating realistic income projections. Start by gathering 6–12 months of historical financial data to identify patterns you can rely on. This involves pulling together invoices, bank statements, 1099-NEC forms, and deposit records. The more thorough your records, the clearer your understanding of your income trends. Once you have this data, track and analyze it systematically to uncover meaningful patterns.

Collecting Historical Data

To organize your financial records, use a tracker - either a spreadsheet or accounting software - that logs essential details like invoice numbers, client names, amounts, and dates (both sent and paid). A sequential invoice numbering system can help keep things tidy. For example, you might use simple numbering like INV-0001, INV-0002, or opt for date-prefixed numbers for high volumes, such as INV-202603-001. Keeping records this organized not only simplifies tax audits but also makes it easier to spot unpaid invoices.

If your financial tracking has been inconsistent, take immediate steps to separate your business and personal finances. Start by directing all client payments into a dedicated business account. This separation offers a clear view of your business's performance and makes record-keeping much easier. As Mike Allerson, CPA and Financial Expert at SelfEmployed.com, explains:

"The business account absorbs the volatility. Your personal life does not."

With your records in place, you can start identifying seasonal trends in your income.

Finding Seasonal Patterns

Once your data is collected, look for seasonal fluctuations in your income. A full 12-month cycle is ideal for spotting recurring dips and surges, such as slower months during holidays or busier periods at other times of the year. Identify your lowest consistent monthly income, your average monthly income, and your highest-earning months. These figures will give you a sense of your income's range and volatility.

Be sure to exclude unusual income spikes that don’t reflect your typical earnings. For instance, if you landed a one-time project that significantly boosted your income, it’s wise to leave that out when calculating your average.

Calculating Average Monthly Income

To determine your baseline income, add up your net earnings from the past 12 months and divide by 12. A good rule of thumb is to budget using the 80% Rule: allocate 80% of your monthly average for expenses and set aside the remaining 20% for savings and taxes.

For fixed expenses like rent and utilities, consider using your lowest-earning month from the past year as your baseline. This conservative approach, often called "survival budgeting", ensures you can cover essentials even during slow months. As SelfEmployed.com puts it:

"Living below your average isn't pessimism. It's insurance."

Another option is to calculate rolling averages based on the past 3–6 months. This method allows your forecasts to adjust dynamically as your business evolves. Rolling averages are particularly helpful for responding to recent changes in your income and provide a more current basis for budgeting and preparing for leaner times.

Assessing Current Workload and Pipeline

Looking at historical data shows where you’ve been, but assessing your current workload and pipeline gives you a clearer picture of where you’re headed. This assessment combines guaranteed work with potential opportunities, helping you predict future income more accurately. The key is to separate confirmed revenue from speculative opportunities. Together, this analysis complements your historical income review and sharpens your cash flow forecast.

Reviewing Active Contracts

Start by listing all your active projects, retainers, and maintenance agreements. For each, note the total contract value, remaining hours or deliverables, and payment dates based on your agreed terms and milestones. This gives you a clear view of your guaranteed income.

Next, calculate your billable capacity by subtracting non-billable activities - like admin work, marketing, and sales - from your total available hours. For most solo freelancers, this typically ranges from 22 to 30 billable hours per week. Compare your committed work against this capacity to determine if you can take on new projects or if you’re nearing overload. A utilization rate between 65% and 80% is ideal, balancing productivity with enough flexibility for unexpected client needs. Going above 80% increases the risk of burnout, while falling below 50% signals a need to focus on finding more work. This step is crucial for understanding your workload before considering new opportunities.

For larger projects (over $2,500), break payments into phases - commonly 25% at kickoff, 25% at the midpoint, 25% at draft completion, and 25% at final delivery. This phased approach ensures steady cash flow rather than waiting until the project wraps up. Also, track payments by their due dates, not invoice dates, since 63% of freelancers reported waiting over 30 days to get paid in 2025.

Estimating Potential Leads

Not every lead converts into paying work, so assign a confidence percentage to each based on its stage in your sales process. For instance:

- A "Confirmed" project awaiting a signed contract might have a 90% likelihood.

- A "Likely" prospect requesting a detailed proposal could be at 60%.

- A "Possible" lead from an initial inquiry might only get 20%.

Multiply each lead’s estimated value by its confidence percentage to avoid overestimating your pipeline. This weighted approach refines your income projections.

Stick to the 70% Rule: only fill 70% of your available hours with committed work. The remaining 30% acts as a buffer for scope changes, urgent client requests, and time for business development. As Wiggleroom puts it:

"The feast-famine cycle is not inevitable - it is a symptom of poor capacity visibility".

By understanding your capacity, you’ll be better equipped to decide which leads to prioritize and when to dedicate time to marketing.

Finally, apply the "No more than 25%" rule to limit concentration risk. Make sure no single client accounts for more than 25% of your revenue. If a dominant client suddenly cancels, it could severely impact your income and ability to cover expenses. Balancing your client portfolio is key to maintaining financial stability.

Income Forecasting Methods

Freelance Income Forecasting Methods Comparison Chart

When it comes to predicting your freelance income, the right forecasting method can make all the difference. Over 59% of freelancers report inconsistent monthly earnings, which means traditional, fixed-budget strategies often fall short. By choosing a method that aligns with your workflow and income patterns, you can better prepare for fluctuations and opportunities.

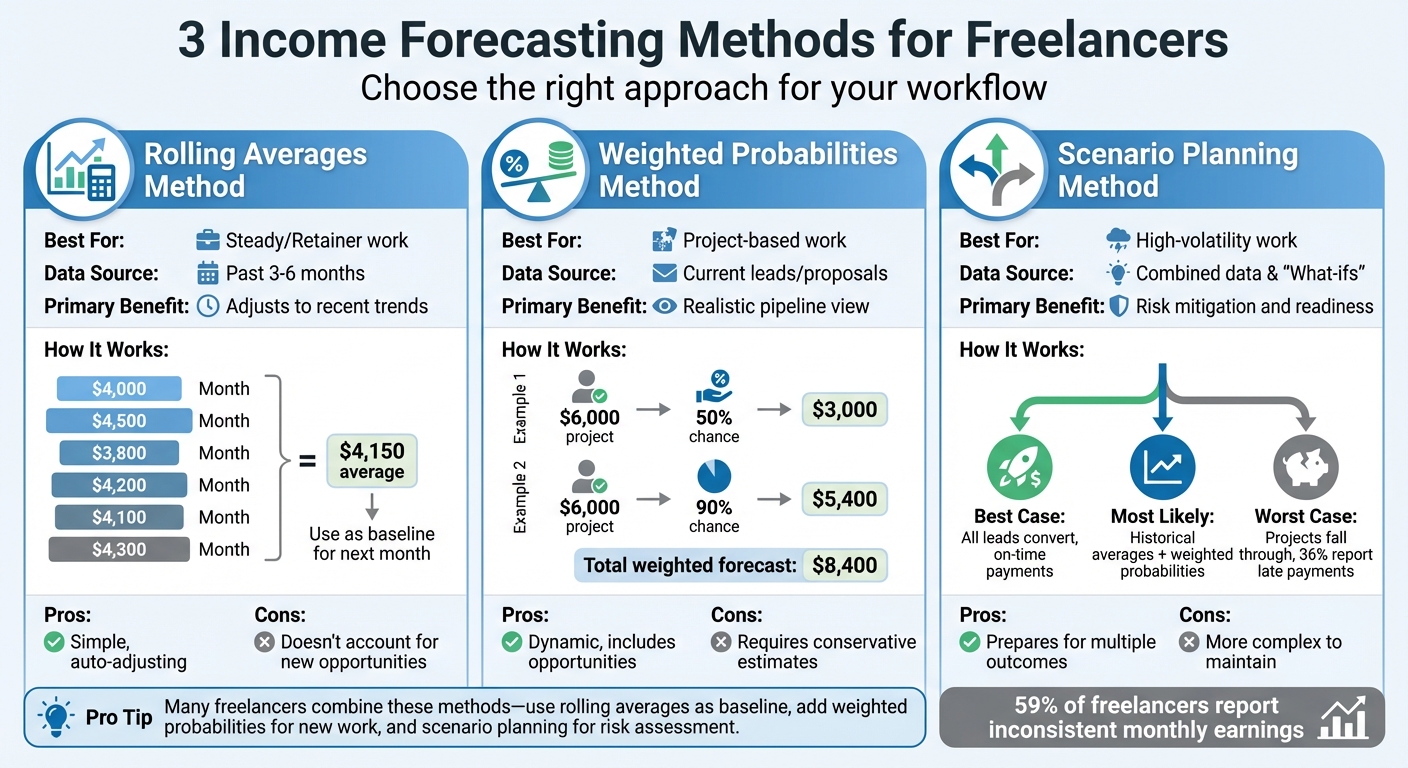

Rolling Averages Method

This approach uses a moving average of your earnings over the past 3–6 months, making it ideal for freelancers with consistent, recurring work. For instance, if your last six months of income were $4,000, $4,500, $3,800, $4,200, $4,100, and $4,300, your rolling average would be $4,150. This figure serves as a baseline for estimating next month’s income.

The biggest perk of this method is its simplicity. Your forecast automatically adjusts as you replace older data with newer figures. However, it’s worth noting that rolling averages don’t account for new opportunities or changes in your workload, making it somewhat limited in scope.

Weighted Probabilities Method

Unlike rolling averages, this method incorporates both past data and current opportunities. Here’s how it works: assign a probability to each potential project based on its likelihood of closing, then multiply the project’s value by that percentage. For example:

- A $6,000 project with a proposal sent might have a 50% chance of closing, contributing $3,000 to your forecast.

- A verbal agreement with a long-term client for $6,000 might be assigned a 90% chance, adding $5,400 to your projection.

The total of these weighted amounts gives you a more dynamic and realistic income estimate. This method is particularly useful for freelancers who rely on a steady flow of new proposals. However, it’s crucial to stay conservative with your probability estimates - reserve higher percentages for reliable clients and lower ones for newer leads.

As Mike Allerson, CPA at SelfEmployed.com, puts it:

"Irregular income isn't just a cash-flow problem; it's a psychological one".

Using weighted probabilities can help you manage uncertainty by giving you a clearer picture of what’s likely to come through.

Scenario Planning Method

Scenario planning involves mapping out three distinct income scenarios:

- Best Case: Every lead converts, payments arrive on time, and you secure additional work.

- Worst Case: Key projects fall through, payments are delayed (36% of freelancers reported at least one late payment in the last quarter of 2025), or a major client cancels.

- Most Likely: A balanced estimate that combines your historical averages with weighted probabilities from current leads.

This method is especially helpful for freelancers dealing with unpredictable income or aiming for aggressive growth. It’s not about predicting the future but about preparing for multiple outcomes. As Mike Allerson explains:

"The freelancers who stay independent the longest aren't the ones who earn the most in any single month. They're the ones who design their financial lives to absorb unpredictability without panic".

Comparison of Methods

Here’s a quick comparison to help you decide which method works best for your situation:

| Method | Best For | Data Source | Primary Benefit |

|---|---|---|---|

| Rolling Averages | Steady/Retainer work | Past 3–6 months | Adjusts to recent trends |

| Weighted Probabilities | Project-based work | Current leads/proposals | Realistic pipeline view |

| Scenario Planning | High-volatility work | Combined data & "What-ifs" | Risk mitigation and readiness |

Many freelancers find that combining these methods works best. For example, you could use rolling averages as a baseline, layer in weighted probabilities for new opportunities, and apply scenario planning for a broader view of potential risks and rewards. This blended approach can provide a more comprehensive strategy for managing your freelance income.

Accounting for External Factors

Even the most well-thought-out income projections can fall short if you overlook broader economic and industry trends. As AlphaTax Blog puts it, "When companies tighten budgets, contractors get cut before employees. Projects get paused. Invoices get delayed". By factoring in these external forces, you can create forecasts that better withstand unexpected market changes.

Tracking Market Trends

Your income is tied to the ebb and flow of market demand, technological advancements, and industry cycles. For instance, freelancers working in fast-growing sectors like tech startups or eco-conscious brands often earn up to double the standard market rate. Staying on top of these trends is critical to keeping your projections accurate.

Platform fees also play a role in shaping your earnings. Take Fiverr’s decision to lower its commission from 20% to 15%; this change gave freelancers on the platform an instant boost in their take-home pay.

Technology is another game-changer. Rapid adoption of AI tools in 2025 and 2026, for example, sparked a surge in demand for specialists who could integrate these tools into design and marketing workflows. If you’re not actively tracking these shifts through industry reports, LinkedIn, or professional communities, you risk basing your pricing on outdated data. These insights also signal when it’s time to upskill or pivot your services.

Specializing in a niche can also help you stand out in saturated markets. For example, designers tailoring their services to environmental NGOs or SaaS startups can maintain higher rates even during economic downturns.

Adjusting for Economic Conditions

When refining your forecasts, it’s crucial to account for inflation and the possibility of a recession. Economic shifts hit freelancers differently - tight budgets often mean freelancers are the first to be cut, and some industries are more vulnerable than others. Think of real estate in 2008, hospitality in 2020, or tech in 2023. Prepare for scenarios where work slows down, no matter how skilled you are.

Inflation, in particular, raises both your operating costs and the minimum income you need to get by. In 2026, freelancers should consider raising their rates by 10–15% annually to offset rising costs for software, equipment, and daily living. Ignoring inflation in your planning is essentially setting yourself up to earn less over time.

Be proactive about spotting client red flags, such as extended payment terms, internal reorganizations, or sudden budget cuts. These are signals to revise your worst-case scenario forecasts immediately.

Diversifying your client base is another safety net. Avoid relying on any single client for more than 25% of your projected income, as previously discussed. Similarly, aim to spread your work across at least three industries, ensuring no more than 40% of your income comes from one sector. This approach cushions you against downturns in specific markets while others remain stable.

During economic slowdowns, skills that focus on cost-saving and efficiency - like process automation or ROI-driven marketing - become more valuable. If your expertise leans heavily toward services tied to discretionary spending, consider how you can pivot to more essential offerings during challenging times.

| Economic Factor | Impact on Forecast | Recommended Action |

|---|---|---|

| Inflation | Raises "Survival Number" and operating costs | Increase rates or cut non-essential expenses |

| Recession Risk | Higher likelihood of project cancellations | Build a 6–9 month cash reserve; diversify clients |

| Tech Shifts (AI) | Alters demand for certain skill sets | Upskill in cost-saving or high-demand niches |

| Tax Deadlines | Affects quarterly cash flow | Set aside 25–30% of every payment immediately |

Make it a habit to review industry trends and economic indicators every quarter. This includes checking your client concentration, identifying which industries are growing or shrinking, and updating the likelihood of pending proposals based on the latest market sentiment. Regular adjustments like these can keep your income pipeline resilient.

Tools for Income Projections

Accurate income forecasting is crucial for managing cash flow, especially for freelancers and independent professionals. Using the right tools can turn guesswork into a reliable process. For perspective, 82% of freelancers have faced cash flow issues - often due to outdated methods and poor tracking systems. Modern tools, many powered by AI, can predict payment dates more accurately, giving you a clearer picture of your financial situation.

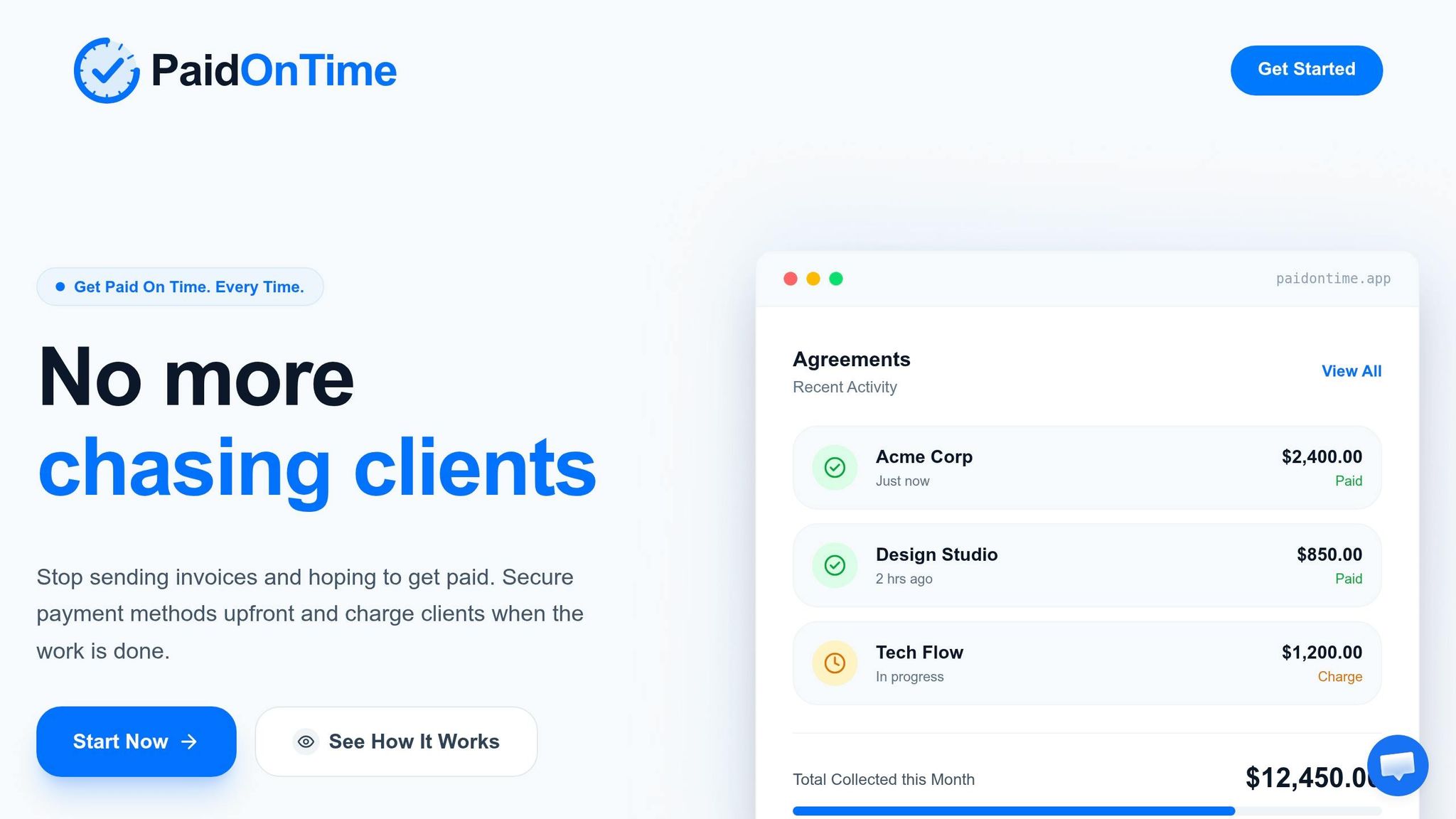

Paid on Time for Payment Security

Getting paid on time is essential for steady cash flow and dependable forecasting. Paid on Time simplifies this by securing upfront payments and formalizing legally binding agreements. This means you’ll receive your funds promptly without worrying about long payment delays. Once your work is done, you can initiate a one-click charge, eliminating the need to chase payments. This is particularly helpful given that the average invoice takes 45 days to get paid, leaving expenses tied up during that period. Knowing exactly when payments will arrive allows for more precise cash flow projections. Additionally, clear payment terms help minimize disputes and unexpected project changes, making your forecasts more dependable.

Spreadsheets and Accounting Software

Spreadsheets remain a straightforward way to track income over 6–12 months, spot seasonal trends, and calculate an average baseline. However, they lack real-time tracking, which can lead to underreporting. In fact, 77% of professionals underreport billable hours, costing high earners over $10,000 annually.

For a more streamlined approach, accounting software automates many tasks, like categorizing expenses and generating reports. Tools such as QuickBooks Self-Employed (priced at $15–$30/month) and Wave (free for invoicing) make these processes easier. More advanced platforms like Float ($49/month) and Pulse ($29/month) provide cash flow forecasting with a 13-week rolling window, which is an industry standard for identifying trends and ensuring short-term accuracy. Many of these tools also use AI to analyze client payment histories, predict payment dates, and send automated reminders - reducing late payments by up to 60%.

Updating Your Forecasts

To keep your income projections useful, they need to be updated regularly. While historical data and current workload evaluations are key to accurate forecasting, staying on top of changes is just as important. A consistent review process ensures you’re prepared for any financial surprises.

Setting Regular Review Dates

A structured review schedule can help you keep your forecasts on track:

- Daily: Spend about 2 minutes checking your bank balance to stay on top of immediate liquidity.

- Weekly: Update your 13-week rolling forecast with new invoices and confirmed project start dates.

- Monthly: Dedicate roughly an hour to compare your actual income against projections.

- Quarterly: Set aside 2–3 hours for strategic planning, including adjusting your salary based on your business account's performance.

The 13-week rolling forecast is particularly effective for freelancers. It’s short enough to stay accurate yet long enough to reveal trends, covering most payment cycles. For example, if a client consistently pays late, adjust your forecast to account for delays - such as payments arriving 14–30 days after their "Net 30" terms. These regular updates ensure your projections reflect both short-term liquidity and long-term patterns, helping you stay prepared for unexpected changes.

Adjusting for New Projects or Cancellations

In addition to routine reviews, update your forecasts immediately when major changes happen, like postponed projects, scope changes, or new contracts. For larger projects, it’s a good idea to break payments into milestones rather than forecasting a single lump sum. This approach gives you a clearer picture of your cash flow throughout the project.

Running "what-if" scenarios can also be a lifesaver. For instance, consider how your finances might look if two major clients delay projects at the same time or if demand suddenly drops. Planning for these possibilities can help you spot potential cash flow issues before they escalate. Also, using an agreement-backed payment platform to automate billing as soon as a project is completed speeds up payments - on average, invoices sent immediately are paid 40% faster than those sent at the end of the month. Make it a habit to update your forecast within 24 hours of completing work to keep your cash flow data current.

Quarterly reviews are a great time to reassess your assumptions and refine forecasts based on new client deals or timeline changes. Use this time to recalculate your lowest monthly income from the past year and adjust your spending baseline accordingly. This ensures your budget is grounded in realistic numbers rather than overly optimistic ones. Keeping your forecasts up to date creates a solid foundation for strategic decisions in your future planning sessions.

Conclusion

Accurate income projections are the backbone of financial stability, especially in the unpredictable world of freelancing. Long-term success in freelancing isn’t about earning the most; it’s about creating systems that help you handle income fluctuations with confidence. By analyzing past income trends, using structured forecasting tools like rolling averages and scenario planning, and reviewing your progress regularly, you can replace uncertainty with clarity. That clarity is what drives practical financial decisions.

Consider this: 80% of freelancers who rely on gig work struggle with unexpected expenses, and 59% face inconsistent monthly income. These challenges stem not just from irregular earnings but also from delayed payments. While forecasts can help you plan what you should earn, tools like Paid on Time ensure you actually receive it. With 80% of freelancers reporting late payments and average delays stretching to 60 days, securing upfront payment agreements and streamlining invoicing can bridge the gap between financial projections and real cash flow.

Here’s how you can put these strategies into action:

- Keep personal and business finances separate.

- Automatically transfer 25–30% of your income for taxes as soon as you get paid.

- Build a cash reserve based on your "Survival Number."

As Mike Allerson, CPA and Financial Expert at SelfEmployed.com, wisely notes:

"The freelancers who stay independent the longest aren't the ones who earn the most in any single month. They're the ones who design their financial lives to absorb unpredictability without panic".

Make it a habit to update your projections whenever a project is added or canceled. Set aside time each month to compare your forecasted income against what you actually earned, refining your assumptions as you go. Clear payment terms alone can reduce late payments by up to 40%, so pairing smart forecasting with reliable payment practices can create a solid financial foundation for your freelance business.

The goal isn’t flawless predictions - it’s about lowering financial stress and making smarter decisions about growing your business, managing expenses, and saving for the future. Start small, track your progress, and fine-tune your approach as you go. Every step brings you closer to financial stability and long-term success.

FAQs

How do I project income if I have less than 6 months of data?

If you've got less than six months of data to work with, start by reviewing your recent income trends and calculating an average. Be sure to account for any seasonal changes or project-based variations that might affect your earnings. Don’t forget to factor in external influences, like upcoming projects or potential changes in your workload. Use this information to set income goals that align with your expenses and savings needs. As you gather more data over time, make it a habit to update your projections regularly to keep them as accurate as possible.

What confidence percentages should I use for leads in my pipeline?

Assigning confidence levels to your freelance leads - like confirmed, likely, or possible - can help you project your income more accurately. By weighting projects based on their likelihood, you can better forecast demand for the next 4–6 weeks. This method not only helps you manage your workload effectively but also prevents overcommitting. The result? More dependable income predictions and improved planning.

How much cash reserve should I keep for slow months and late payments?

Experts suggest setting aside a cash reserve that covers at least three months of living expenses. This can help you navigate slow periods or late payments without stress. If saving that much feels daunting, aim to build up one month's worth first. For those seeking extra peace of mind, a reserve covering six months of expenses is often recommended. The goal is to have enough savings to handle irregular income and delays in payments confidently.