How to Use Cash Flow Tools for Freelance Planning

How to Use Cash Flow Tools for Freelance Planning

Freelancing offers flexibility but often comes with unpredictable income. Many freelancers struggle with late payments, unexpected expenses, and cash flow issues, which can make managing finances challenging. The key to overcoming this is understanding that revenue isn’t cash until it’s in your account. Cash flow tools help freelancers predict financial shortfalls, plan ahead, and avoid surprises.

Key Takeaways:

- Track income and expenses: Know your "survival number" (minimum monthly needs) and categorize costs as fixed or variable.

- Use cash flow tools: Options range from spreadsheets (manual) to software like Pulse or QuickBooks (automated).

- Create forecasts: Use a 3-month rolling forecast to project income and expenses, and prepare for best, base, and worst-case scenarios.

- Secure timely payments: Tools like Paid on Time ensure quicker payments by collecting payment details upfront.

- Regular updates: Review and adjust forecasts weekly to stay on top of changes.

By combining these strategies, freelancers can manage finances better, reduce stress, and build a stable career.

5-Step Cash Flow Management Process for Freelancers

Create a Cash Flow Forecast for Your Business (in under 16 minutes) {FREE TEMPLATE}

sbb-itb-66f4c95

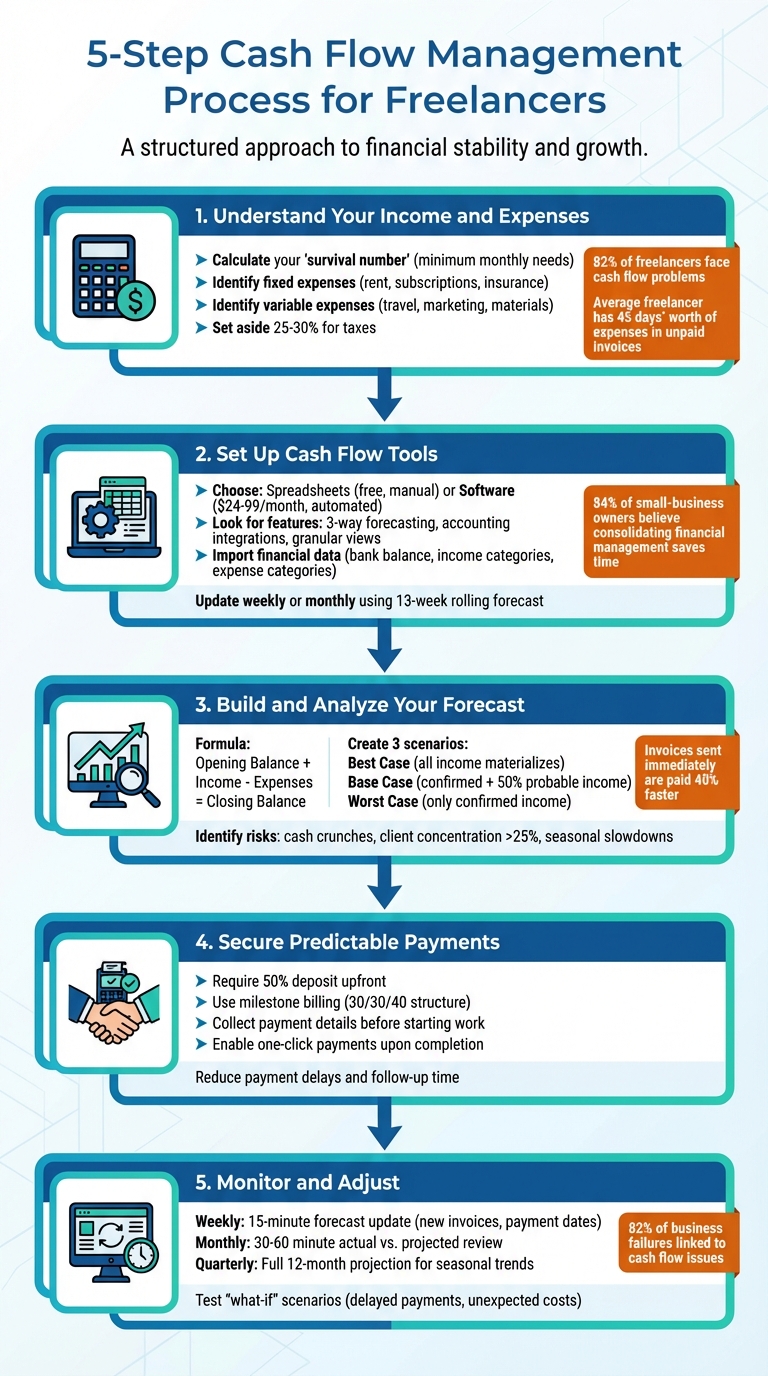

Step 1: Understand Your Income and Expenses

Knowing exactly where your money comes from and where it goes is essential. A cash flow tool is only as good as the data you provide, and overlooking even one recurring expense could lead to a dangerously inaccurate forecast.

Start by figuring out your "survival number" - the bare minimum you need each month to keep both your business and personal life afloat. This includes essentials like rent or mortgage, groceries, health insurance, internet, phone, and any minimum debt payments. As Suze Orman wisely states:

"Knowing this number [the survival number] should be like knowing the back of your hand."

This number serves as your financial baseline. Everything else you plan financially should build upon this foundation.

Identify Fixed and Variable Expenses

Break your expenses into two categories: fixed and variable. Fixed expenses are consistent each month - think rent, software subscriptions, insurance, and loan payments. On the other hand, variable expenses fluctuate based on your workload, such as travel costs, marketing campaigns, subcontractor fees, and materials for projects. Understanding this distinction is critical because it shows which costs can be adjusted during slower periods and which are non-negotiable.

It's worth noting that 82% of freelancers have faced cash flow problems because they failed to account for all their financial obligations. When planning, make sure to integrate your personal living costs with your business expenses.

Don’t forget about taxes - a common blind spot for freelancers. In the U.S., freelancers are subject to a 15.3% self-employment tax in addition to regular income taxes. To avoid any surprises, set aside 25–30% of every payment in a separate tax account so you don’t accidentally spend money meant for the government.

Once you have a clear picture of your expenses, it’s time to focus on your income.

Track and Organize Your Income

Now, shift your attention to tracking the money coming in. Set up a simple system to log essential details like the date you sent each invoice, the client name, the project, the invoice number, the amount, and - most importantly - the payment date. This is crucial because delays between billing and payment are common. In fact, the average freelancer has 45 days’ worth of expenses tied up in unpaid invoices.

Remember, an invoice doesn’t equal cash in hand.

Review your income from the past 12 months to identify trends. Use your lowest-earning month as the baseline for planning instead of relying on your average income. This conservative approach helps you avoid overestimating your available funds. Also, watch for seasonal patterns - many freelancers experience slower months in August or December. Preparing for these dips by building a cash buffer can save you from financial stress.

If you’re working with multiple clients, consider spreading out your invoices across the month instead of billing everyone on the same day. For instance, you could send invoices on the 1st, 15th, and 20th to maintain a steadier cash flow.

With a solid understanding of your income and expenses, you’re now ready to move on to setting up effective cash flow tools.

Step 2: Set Up and Use Cash Flow Tools

Once you’ve nailed down your financial baseline, the next step is choosing the right tool to help you forecast cash flow. A well-configured tool can turn raw financial data into insights you can act on - helping you stay ahead of potential cash flow problems.

Choose the Right Tool for Your Needs

If you’re just starting out, spreadsheets like Google Sheets can be a free and flexible option. However, they require manual data entry, which can be time-consuming. On the other hand, dedicated cash flow software automates tasks like syncing with your bank account and modeling different financial scenarios, though these tools usually come with a monthly subscription fee.

For instance, tools like Pulse let you organize cash flow by customer or project, making it easier to see which clients are driving the most profit. These tools often cost between $24 and $99 per month, but they can save you hours and provide deeper insights. When choosing software, focus on features like:

- Three-way integrated forecasting: Links your Profit & Loss statement, balance sheet, and cash flow for a complete picture.

- Accounting software integrations: Reduces manual data entry by syncing directly with platforms like QuickBooks or Xero.

- Granular views: Daily or weekly cash flow monitoring helps you keep tabs on short-term payments.

According to research, 84% of small-business owners believe consolidating financial management into one platform could save them time. Also, consider the tool’s forecasting range. Some, like QuickBooks, offer short-term projections (up to 90 days), while others, such as PlanGuru, support long-term forecasts of up to 10 years. If you’re a freelancer, aim for a rolling forecast covering at least three months. Need to manage expenses on the go? Look for tools with a strong mobile app.

Once you’ve selected your tool, import your financial data to start creating forecasts you can rely on.

Input and Organize Your Financial Data

Accurate data is the backbone of any reliable cash flow forecast. Start with your current bank balance as the opening cash balance - it’s the foundation for your projections. From there, focus on tracking cash when it actually moves, not when invoices are sent or bills are received. This ensures you’re working with cash-based accounting.

Break down your income into categories like sales revenue, accounts receivable collections, and other income sources. For expenses, use three main categories:

- Fixed costs: Rent, insurance, software subscriptions.

- Variable costs: Materials, marketing, shipping.

- Periodic costs: Quarterly taxes, annual license renewals.

Review 6–12 months of past transactions to identify seasonal trends and understand client payment habits. If you’re using automated software, connect it to your bank and accounting platform to pull in real transaction data. Some tools, like Trezy, even use AI to auto-categorize transactions with up to 95% accuracy. You can refine the system by correcting errors, teaching it your unique spending habits.

Don’t forget to include sales tax or VAT in your cash flow records. Unlike your Profit & Loss statement, which excludes taxes, cash flow forecasts should reflect the actual movement of money.

Update your data regularly - weekly or monthly - using a 13-week rolling forecast for short-term planning. As one expert from Beancount.io wisely observed:

"A forecast from January is useless by March if you haven't updated it. Business conditions change constantly."

And don’t stress about perfection. Round numbers are fine for spotting patterns and preparing for potential cash gaps. The goal here isn’t flawless accounting; it’s staying ahead of financial surprises.

Step 3: Build and Analyze Your Cash Flow Forecast

Create a Monthly Cash Flow Projection

With your financial data organized, it’s time to put together your cash flow forecast. Start with a rolling 3-month (13-week) window - this timeframe strikes a balance between spotting patterns and maintaining accuracy. The formula is straightforward: take your opening balance, add projected income, subtract expenses, and you’ll arrive at your closing balance. That closing balance then becomes the opening balance for the next period.

When estimating income, it’s best to stay cautious. Categorize your income by confidence levels: include confirmed income (90% or more likely) at full value, and for probable income (40–60% likely), adjust by its likelihood. For example, if you’ve pitched a $5,000 proposal with a 50% chance of approval, you’d count it as $2,500. This method helps avoid the overconfidence that has caused cash flow problems for 82% of freelancers.

On the expense side, divide your costs into two categories: fixed costs (like rent, software subscriptions, and insurance) and variable costs (such as project materials, travel, or subcontractor fees). To prepare for uncertainties, create three scenarios for each quarter:

- Best Case (all income materializes)

- Base Case (confirmed income plus 50% of probable income)

- Worst Case (only confirmed income)

This three-scenario approach helps you anticipate different outcomes and make informed decisions. These scenarios will also guide you in managing payments and expenses, which we’ll explore further in the next section.

Keep your forecast updated weekly. Add new proposals, remove expired ones, and adjust probabilities as needed. A key figure to calculate is your survival number - the minimum amount you need each month to cover essential personal and business expenses. This figure acts as a baseline that your forecast should never dip below.

With your forecast ready, the next step is to identify potential risks and opportunities in your cash flow.

Identify Risks and Opportunities

Once your forecast is running, keep an eye out for cash crunches, or weeks where your projected balance falls below one month’s worth of expenses. The biggest risk often comes from timing gaps - when you’ve finished work but haven’t been paid yet. As Receipt Router puts it:

Profit tells you if your business is making money. Cash flow tells you if you can pay your rent next month.

Another risk to monitor is client concentration. If one client accounts for more than 25% of your revenue, losing them could seriously disrupt your forecast. Also, consider seasonal trends - freelancers often face slow periods in August (summer vacations) and December (holiday spending freezes). Recognizing these patterns allows you to build cash reserves during busier months.

Set decision triggers based on your forecast. For example, if the Worst Case scenario predicts a negative balance in two months, that’s your signal to ramp up marketing efforts immediately. Stress test your forecast by asking questions like, “What if my largest client delays payment by 30 days?” or “What if unexpected equipment costs come up?” These scenarios help you gauge whether your cash buffer can handle unexpected challenges.

Opportunities can also emerge from your forecast. Weeks with high cash flow are ideal for making major business purchases or investing in growth. If your forecast shows consistent surpluses, consider milestone billing for large projects - splitting payments into a 30/30/40 structure (deposit, midpoint, final delivery) ensures steady cash flow throughout the project. And here’s a simple but effective tip: invoices sent immediately after project completion are paid 40% faster than those sent at the end of the month.

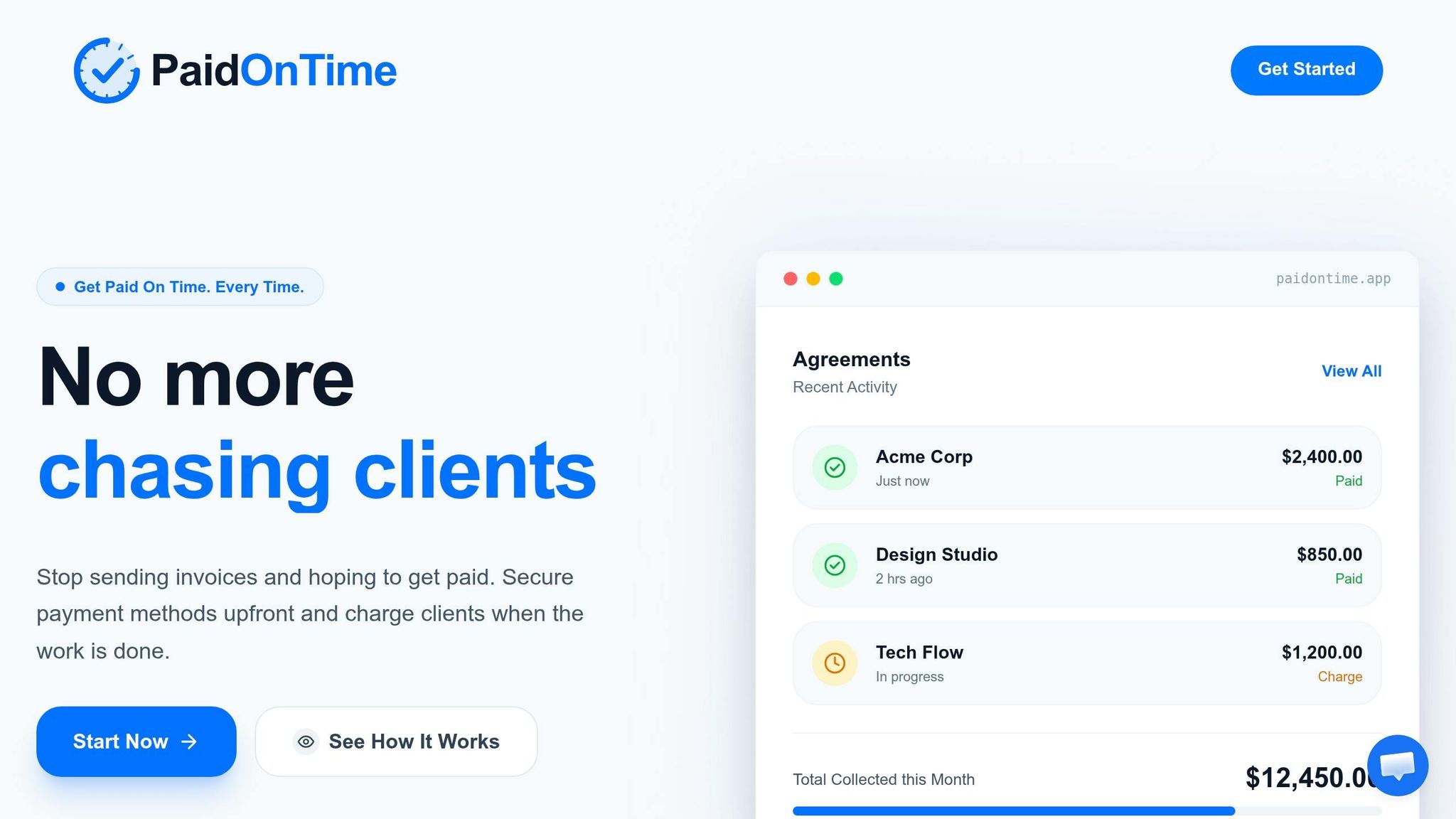

Step 4: Secure Predictable Payments with Paid on Time

Create Agreements and Secure Payment Methods

Delayed payments after completing a project can be a major headache, but you can tackle this issue before work even begins. The key? Make payment security a built-in part of your process by setting up clear agreements and locking in payment methods upfront.

With Paid on Time, you can draft legally binding agreements and collect payment details in advance. This aligns with the freelancing "Golden Rule": always require a 50% deposit to confirm the client’s commitment to the project. For longer engagements, setting up milestone payments - like 30% upfront, 30% halfway through, and 40% upon completion - can help ensure steady cash flow over the course of the project.

Once the groundwork is laid, simplify the payment process so funds are ready to transfer as soon as the project wraps up.

Enable One-Click Payments Upon Completion

Traditional invoicing can slow things down since it requires clients to manually process payments. Paid on Time eliminates this delay by securing payment details in advance and enabling one-click charges upon project completion. This hassle-free system spares you the trouble of following up on invoices, ensuring payments are processed quickly and without added stress.

Improve Cash Flow Predictability

By securing payment methods before starting a project, you turn payment into a seamless part of the approval process rather than a separate hurdle. Paid on Time charges a flat 5% transaction fee and has no monthly costs, giving you clear payment records. This transparency makes it easier to forecast cash flow and reduces uncertainty in your financial planning.

Step 5: Monitor and Adjust Your Cash Flow Plan

Review and Update Monthly

Keeping your cash flow forecast accurate means committing to regular updates. Once you've set up your forecast, it's important to revisit it frequently to reflect any changes. A quick 15-minute session every Friday to update your 3-month forecast with fresh invoices and revised payment dates can make a big difference in staying on top of your finances. It’s a small time investment that ensures your financial outlook remains current without taking over your day.

At the end of each month, spend 30–60 minutes comparing your actual income and expenses to your projections. This comparison helps you identify patterns. For instance, if you notice you're consistently overestimating income or underestimating expenses by about 20%, it's time to tweak your forecasts. This "Actual vs. Projected" review makes your forecast more precise, turning it into a dependable planning tool. By tying your forecast to real numbers, you strengthen the strategies you’ve already set in motion.

Additionally, conducting a full 12-month projection every quarter can reveal seasonal trends and help you prepare for major financial obligations, like taxes. Many freelancers, for example, notice slower periods in August and December during these quarterly reviews. Recognizing these trends allows you to save during busier months and create a financial cushion for leaner times.

Once your forecast is updated, take the extra step to test its strength against different scenarios.

Test Different Scenarios

Your cash flow plan should reflect reality - not just the rosiest version of it. Testing your forecast with best-case, base-case, and worst-case scenarios helps you stay prepared. These scenarios can act as decision triggers. For example, if your forecast warns of a possible cash shortfall, you can ramp up marketing or client outreach before it becomes a problem.

It’s also smart to explore "what-if" situations, like a client delaying payment by 30 days. These tests reveal whether your cash reserves can handle unexpected hiccups. By running these simulations, you’ll be equipped to make thoughtful, proactive decisions rather than scrambling to react when challenges arise.

Conclusion

Managing freelance cash flow effectively isn't about guesswork - it’s about using the right tools and staying on top of your financial situation. By tracking your income and expenses, implementing automated forecasting tools, and creating realistic financial projections, you can map out a plan that helps you spot potential problems before they hit your wallet.

"Cash flow planning isn't about gazing into a crystal ball. It's about drawing a realistic map that gives you enough of a heads-up to steer around the potholes instead of driving straight into them." – Receipt Router

This quote perfectly captures the importance of taking a proactive approach to cash flow management.

The statistics are sobering: 82% of business failures are linked to cash flow issues. For freelancers, this challenge is often amplified by the delay between completing work and getting paid. That’s why tools like Paid on Time are game-changers. By allowing freelancers to secure payment methods upfront and charge clients with a single click after completing a project, these platforms help close the gap between invoicing and receiving payment. This means fewer sleepless nights worrying about unpaid invoices.

unpaid invoices don’t pay your bills. But when you combine payment certainty with the strategies outlined in this guide - tracking income and expenses, using forecasting tools, and keeping your projections updated - you can build a financial safety net. This approach ensures you’re prepared to handle the unpredictable ups and downs that come with freelance work.

FAQs

How much cash should I keep as a buffer?

Freelancers are often encouraged to keep a cash reserve that covers at least three months of living expenses. This can help manage the ups and downs of irregular income or unexpected bills. If saving that much feels overwhelming, even setting aside enough for one month can offer some peace of mind. For those whose work is seasonal or highly unpredictable, aiming for a larger cushion might be a smarter move to stay financially secure.

What should I do if a client pays late?

If a client delays payment, safeguard your cash flow by establishing clear contracts that outline payment due dates and late-fee policies upfront. Use automated reminders to nudge clients toward timely payments. If late payments continue to be an issue, you might need to pause work or take further steps to address the situation. These measures can help minimize the financial strain caused by overdue payments.

How do I estimate income from proposals?

To get a handle on your potential income from proposals, start by listing all active proposals along with their expected value. For each proposal, assign a probability of success based on your confidence or historical win rates. Then, estimate when payments might come in, considering typical terms like Net 30 or whatever applies to your industry.

Using this information, you can forecast your cash flow by factoring in both the likelihood of winning and the expected payment timing. This approach gives you a practical view of your future income, helping you plan your expenses with greater accuracy.