Freelancer Guide: Vetting Clients For Payment Security

Freelancer Guide: Vetting Clients For Payment Security

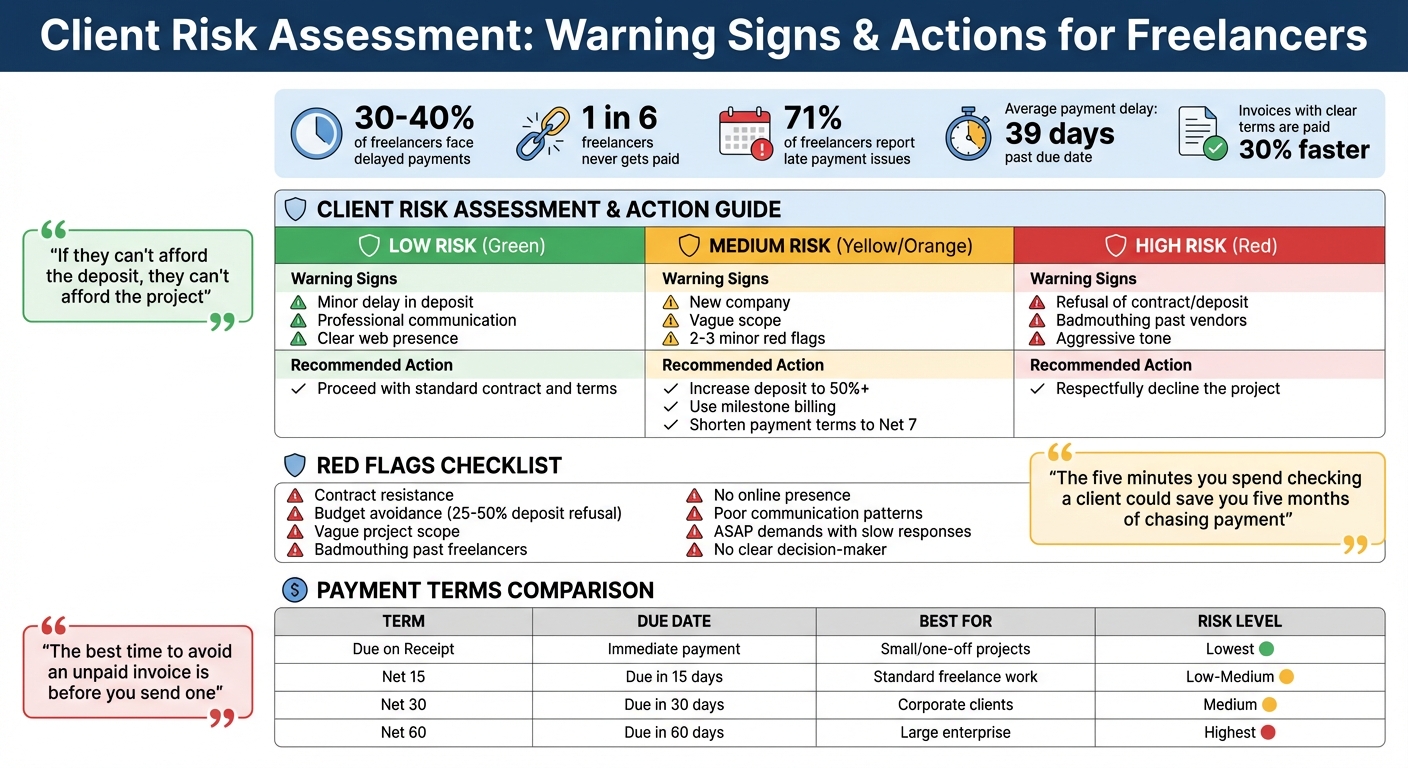

Freelancing can be rewarding, but it comes with risks - like late payments or never getting paid at all. Did you know 30–40% of freelancers face delayed payments, and 1 in 6 never gets paid? Protecting your income starts with identifying red flags before committing to a client. Here's how to avoid payment troubles:

-

Red Flags to Watch For:

- Clients refusing contracts or deposits.

- Vague project scopes or unclear budgets.

- Poor communication or boundary-pushing behavior.

- Negative comments about past freelancers.

- Lack of an online presence or verifiable references.

-

Steps to Vet Clients:

- Research their online presence (website, LinkedIn, reviews).

- Check payment history via references or public records.

- Schedule a discovery call to assess professionalism.

-

Set Payment Terms:

- Always use a written contract with clear deadlines (e.g., Net 15).

- Request upfront deposits (25–50%) and use milestone payments.

- Include late payment penalties and work-pause clauses.

-

Use Payment Platforms:

- Tools like Paid on Time secure payment methods upfront and automate invoicing.

What I Wish I Knew Before Freelancing: My Biggest Mistakes

sbb-itb-66f4c95

Red Flags: Spotting High-Risk Clients

Client Risk Assessment Guide for Freelancers: Red Flags and Recommended Actions

Common Signs of Unreliable Clients

The first conversation with a potential client often reveals a lot. One major red flag is contract resistance - when a client insists you "start work now and handle paperwork later." This tactic can leave you vulnerable to payment issues once you're already committed.

Another warning sign is reluctance to discuss budgets. Clients who avoid budget conversations or push back against standard deposits (usually 25–50%) may not be prepared to pay in full. As freelancer Sagar Vaishnava explains:

"If they can't afford the deposit, they can't afford the project. If they won't pay a deposit, they're keeping their options open to bail".

Ambiguity in project scope is another issue. Without clearly defined deliverables, disputes over what’s owed or whether the work is complete become far more likely.

Pay attention to how they describe past freelancers. If they label every previous contractor as "incompetent" or claim no one "understood their vision", it’s possible the client is the common denominator. Sagar Vaishnava puts it bluntly:

"When someone tells you every designer before you was incompetent, you're about to become the next incompetent designer in their story".

Lastly, check their online presence. A company without a website, LinkedIn profiles, or reviews might pose a risk. While new businesses aren’t automatically problematic, a complete lack of a digital footprint can make accountability challenging.

These behaviors often show up in how clients communicate, which we’ll explore next.

Poor Communication Patterns

A client’s communication style can be a strong indicator of how they’ll behave during the project. For instance, clients who demand "ASAP" delivery but then vanish for weeks when you need feedback or invoice approval are likely to disrupt your schedule.

Confusing feedback is another red flag. If you ask, "Who has final approval?" and they can’t identify a decision-maker, expect conflicting instructions and endless revisions. This is especially true if multiple stakeholders - say, eight or more - join a Zoom call without a clear leader.

Boundary-pushing is another common issue. Clients who ignore agreed-upon communication methods, like texting your personal number instead of using email or Slack, or expecting immediate responses on weekends, often lack respect for professional boundaries. Remote work has made these issues more frequent.

Vagueness during consultations is equally concerning. If questions about goals, timelines, or budgets result in unclear or contradictory answers, you’re likely stepping into a chaotic situation. As Asrify notes:

"The riskiest clients are not always the lowest payers - they're the ones who don't respect boundaries, process, or expertise".

Let’s move on to understanding how payment history can reveal even more about a client’s reliability.

Problematic Payment History

A client’s payment history is one of the best indicators of their reliability. Before committing to a project, especially with a new or unknown company, take time to research their financial track record.

For U.S.-based clients, state business registries can provide useful details like incorporation dates, financial filings, and any legal judgments against the company. For high-value projects, you might even consider running a formal credit check.

Request references from other freelancers the client has worked with. A legitimate business should have no problem providing these. If they hesitate or make excuses, that’s a major red flag.

Be cautious of clients who blame past freelancers for issues that only came up after delivery. This could be a tactic to dispute the work and avoid payment. This "post-delivery complaint" approach is a common manipulation strategy.

To verify legitimacy, cross-check the company’s website with LinkedIn profiles of its staff. A polished website doesn’t mean much if there’s no verifiable team behind it. As Landolio wisely advises:

"The best time to avoid an unpaid invoice is before you send one".

| Risk Level | Warning Signs | Recommended Action |

|---|---|---|

| Low Risk | Minor delay in deposit; professional communication; clear web presence. | Proceed with standard contract and terms. |

| Medium Risk | New company; vague scope; 2–3 minor red flags. | Increase deposit to 50%+; use milestone billing; shorten payment terms to Net 7. |

| High Risk | Refusal of contract/deposit; badmouthing past vendors; aggressive tone. | Respectfully decline the project. |

How to Vet Clients Before Starting Work

Spotting red flags is one thing, but taking the time to vet potential clients before committing to a project is just as crucial. The good news? This doesn’t have to involve fancy tools or hours of digging. A quick five-minute check can save you from months of frustration. As Landolio wisely puts it:

"The five minutes you spend checking a client before you start could save you five months of chasing after you've finished".

The goal is simple: confirm identity, payment ability, and professional reputation. Start by looking into the client’s online presence.

Research Client Background and Online Presence

A client’s digital footprint can tell you a lot. A legitimate business usually has a professional website, an active LinkedIn company page, and employees with verifiable work histories. If their website looks generic or incomplete, consider it a warning sign.

For U.S.-based clients handling larger projects, check state business registries to confirm incorporation details. Make sure their registered address isn’t just a virtual office. A quick Google search using phrases like "[Company Name] + not paying" or "[Company Name] + late payment" can reveal complaints from other freelancers.

It’s also worth checking public court records for any legal judgments against the company, which could point to a history of non-payment. For high-value projects, reviewing business credit reports can provide insight into their payment trends.

If the client is a publicly registered company, pay attention to their financial health. A negative or declining net asset position is a red flag. For sole proprietors who may not appear in business registries, rely more heavily on social proof, references, and stricter payment terms - such as requiring a 50% upfront deposit.

Ask for References or Testimonials

Once you’ve verified their online presence, dig deeper into their track record by asking for references. For projects over $500, request contacts from other freelancers or vendors they’ve worked with. Any reputable business should be able to provide these without hesitation.

When speaking with references, ask pointed questions like:

- Did they pay on time?

- Were their expectations clear from the start?

- How did they handle revisions or disputes?

This feedback gives you a clearer picture of how the client operates. If a client hesitates, makes excuses, or claims they’ve never worked with freelancers before - despite presenting themselves as an established business - it’s a major red flag.

Schedule Direct Calls to Assess Professionalism

A discovery call is another essential step. It’s not just about discussing the project - it’s also a chance to gauge their professionalism. Pay attention to whether they’re punctual and respectful of your time. This interaction can reveal whether they’re serious about payment and project management.

Ask direct questions, such as:

"Who has final approval on this project?"

If they can’t provide a clear answer or mention too many decision-makers, prepare for potential chaos with feedback and delays. As Sagar Vaishnava puts it:

"If you ask 'who has final approval?' and they can't give you a name, run".

Also, listen closely to how they discuss budget. Professional clients are usually upfront about ballpark figures early on. If they avoid discussing numbers until after you’ve submitted a proposal, they might be planning to lowball you. Similarly, resistance to contracts or deposits is a red flag for possible payment problems.

Setting Up Payment Terms to Protect Your Income

Once you've vetted a client and decided to move forward, setting clear payment terms from the start is a must. Without a well-defined agreement, you might find yourself chasing payments later. Did you know that 71% of freelancers report issues with late payments, with delays averaging 39 days past the due date?.

Having clear, written payment terms can make a huge difference. For instance, invoices that outline specific terms and offer multiple payment methods are paid 30% faster. Think of your contract as more than just paperwork - it's your safeguard against financial uncertainty.

Document Payment Schedules and Terms in Writing

Every payment agreement should clearly define when payments are due and what happens if they aren’t made on time. Use specific deadlines, like "Net 15" (payment due within 15 days), which is a standard for many freelancers. Avoid vague phrases like "upon completion", which can lead to misunderstandings.

For larger projects - those over $2,000 or lasting more than four weeks - consider breaking payments into milestone schedules tied to specific deliverables. A common structure might be 40% upfront, 30% at the midpoint, and 30% upon final delivery. This strategy ensures you're compensated throughout the project and keeps clients engaged.

Your contract should also include a late payment penalty, typically 1.5% to 2% monthly interest on overdue balances. As Landolio explains:

"A late fee clause isn't just about collecting extra money... Its real value is psychological deterrence. Clients who know there's a financial consequence for paying late tend to prioritise your invoice".

Other key elements to include in your contract are:

- Work suspension clause: Allows you to pause work if payments are late.

- Ownership contingency: Ensures intellectual property remains yours until the final payment is received.

- Kill fees: Compensates you if the client cancels mid-project.

- Payment methods and transaction fees: Clarify what forms of payment you accept and who covers processing fees.

Here’s a quick breakdown of common payment terms:

| Payment Term | Meaning | Best For | Risk Level |

|---|---|---|---|

| Due on Receipt | Immediate payment | Small/one-off projects, new clients | Lowest |

| Net 15 | Due in 15 days | Standard freelance work; ongoing clients | Low to Medium |

| Net 30 | Due in 30 days | Corporate clients and agencies | Medium |

| Net 60 | Due in 60 days | Large enterprise procurement | Highest |

Once your terms are set, using secure payment systems can add an extra layer of protection.

Use Payment Security Platforms

Manually invoicing clients can lead to excuses like "the check is in the mail" and awkward reminders. Payment security platforms streamline the process, automating payments and holding clients accountable.

Take Paid on Time (https://paidontime.app), for example. This platform lets you create legally binding agreements upfront, securely collect the client’s payment method, and charge it with a single click once the work is complete. The client commits to paying before you even start, ensuring you get paid immediately upon project completion. With no monthly fees and a 5% transaction cost, you only pay when you get paid.

This kind of system aligns payment terms with the process itself, making it legally consistent and hassle-free.

Break Projects into Smaller Payment Milestones

Breaking projects into milestones reduces your financial risk. As Landolio points out:

"When you invoice only at the end of a project, you're giving the client maximum leverage and yourself zero protection".

If a client relationship deteriorates or they face financial trouble, milestone payments ensure you’re not left unpaid for weeks - or worse, months - of work.

Each milestone payment acts as a checkpoint. Clients review your progress, provide feedback, and recommit financially. Tie these payments to specific, measurable deliverables like "delivery of the first draft" rather than vague terms like "mid-project". For high-risk clients, a structure like 50% upfront, 25% at the midpoint, and 25% upon final delivery offers extra security.

Include a work-pause clause in your contract, stating that work will stop if a milestone payment isn’t made on time. This creates urgency for clients to pay without requiring uncomfortable conversations. And remember: never hand over final deliverables until the final payment clears. As Landolio wisely advises:

"The final deliverable is your leverage. Once you hand everything over, you've got no cards left to play".

Building a Stable Client Base Over Time

Once you've secured clear payment terms, the next step is to build a reliable client base. The aim isn't just to attract more clients - it's to develop strong relationships with those who respect your work and pay promptly.

Focus on Repeat Clients with Proven Track Records

The best clients aren't always the ones who pay the most - they're the ones who pay on time, communicate effectively, and respect your boundaries. Repeat clients save you the hassle of constant vetting because they've already shown they can follow through on agreements.

Clients who quickly sign contracts and pay upfront are often the most dependable. A helpful strategy is to create a "Good Client Checklist" to track which clients are worth working with again. Pay attention to their payment habits, communication style, and how well they stick to agreed-upon terms. This way, you can focus on nurturing relationships that consistently benefit your workflow.

Set Up Retainer Agreements for Predictable Income

If you're looking for steady income, retainer agreements can be a game-changer. They shift your earnings from unpredictable, project-based payments to a more stable, subscription-like model. Instead of constantly seeking new projects, retainers provide guaranteed income and show a client's long-term commitment to your work.

Before jumping into a retainer, it's smart to test the waters with a smaller "discovery" project, like a paid audit or strategy session. This helps you gauge the client's communication and reliability without committing to a long-term deal right away.

When structuring a retainer, tie payments to specific calendar dates rather than project milestones. For example, billing on the 1st of every month ensures consistent cash flow and avoids delays caused by shifting deadlines. Be sure to include a late fee policy - such as 1.5% interest per month - in your contract to address overdue payments without awkward follow-ups. Tools like Paid on Time can also simplify billing by automating payment schedules and securing upfront payments.

Keep Detailed Records of Client Payment Patterns

Tracking how clients pay isn't just about staying organized - it’s a way to identify your most profitable relationships. Use a spreadsheet or a CRM system to log every payment, including the due date, the date received, the total amount, and the number of follow-ups required. This information can reveal trends you might otherwise miss.

For instance, a client who pays well but demands endless revisions or constant project management may actually be less profitable than a lower-paying client who values your time. Pay close attention to how quickly clients pay initial deposits, as this can indicate the "hidden time cost" of working with them.

Be wary of repeated excuses:

"One excuse is human, but three is a strategy used by cash-strapped or predatory clients to stall payments".

If a client consistently delays payments by two weeks or more - a problem affecting about one-third of clients - it might be time to renegotiate your terms or stop working with them altogether.

Visual tools like color-coded spreadsheets can help you spot late-payers at a glance. This kind of systematic tracking makes it easier to make informed decisions about which clients to prioritize, ensuring a more predictable and sustainable freelance income stream.

Conclusion

Protecting your income as a freelancer starts with recognizing potential red flags, thoroughly vetting clients, setting clear payment terms, and fostering strong client relationships. These steps are crucial to maintaining a steady and reliable freelance career.

Did you know that 30–40% of freelancers experience late payments, and 1 in 6 never gets paid at all? These challenges can often be avoided by making client vetting a standard practice. As Landolio wisely states:

"Vetting a client before you start work isn't suspicious, it's professional." - Landolio

For larger projects, insist on upfront deposits and perform credit checks to minimize risk. A 50% deposit is a strong starting point, paired with a written contract that includes clear payment terms, such as Net 15 or Net 30 deadlines. If the project exceeds $1,000, consider spending $5 to $15 on a credit check - it’s a small investment that could save you months of headaches chasing unpaid invoices.

Once your payment terms are in place, automating your invoicing process can provide additional peace of mind. Tools like Paid on Time simplify this by securing payment methods upfront, generating legally binding agreements, and allowing for quick, hassle-free charges once the work is delivered. Plus, these platforms can document interactions, which is invaluable if disputes arise.

The ultimate goal isn’t just about avoiding problematic clients - it’s about building a network of clients who value your work, pay on time, and even recommend you to others. That’s how you shift from worrying about cash flow to enjoying a stable and predictable freelance business.

FAQs

What should I say if a client refuses a contract or deposit?

If a client hesitates to agree to a contract or provide a deposit, take the time to explain that these practices are standard in the industry. They exist to protect both parties and ensure a clear, committed working relationship. Address their concerns calmly and professionally, emphasizing how these measures create mutual security and clarity.

If the client remains unwilling, you might explore alternative arrangements that still safeguard your interests. However, it’s equally important to recognize when it’s best to step away. Protecting your business while maintaining a professional approach should always be your priority.

How can I verify a client’s payment history quickly?

When evaluating a client's payment reliability, it's smart to look for potential warning signs early. Start by noting any hesitation they might show in signing contracts or sudden shifts in agreed payment terms - these could indicate trouble ahead.

Next, dig into publicly available financial records. Look for red flags like late payments or any legal judgments against them. These details can provide a clearer picture of their financial habits.

Finally, don't underestimate the power of a quick online search. Explore their presence on social media and other platforms to get a sense of their reputation and past behavior. Together, these steps can give you a better idea of their trustworthiness before committing to any work.

When should I use a tool like Paid on Time?

Using a tool like Paid on Time can make sure you get paid promptly while lowering the chances of non-payment. It’s particularly useful for establishing clear payment terms, collecting upfront payments, automating invoices, and minimizing disputes. This is a great option for freelancers working with clients who might push back on standard payment terms or show warning signs, helping protect your earnings and streamline the payment process.