5 Tax Mistakes Freelancers Make Every Year

5 Tax Mistakes Freelancers Make Every Year

Freelancers often face unique tax challenges, which can lead to costly mistakes if not managed properly. Here are five common errors and how to avoid them:

- Skipping Expense Tracking: Many miss out on $2,000–$5,000 in deductions due to poor record-keeping. Digitize receipts and log expenses weekly to maximize deductions.

- Miscalculating Taxable Income: Confusing gross income with taxable income can result in overpaying taxes. Deduct all business expenses and use net profit for calculations.

- Missing Quarterly Payments: Failing to save and pay quarterly taxes leads to penalties. Set aside 25–30% of income for tax payments and follow IRS deadlines.

- Mixing Personal and Business Finances: Commingling funds complicates bookkeeping and raises audit risks. Use separate accounts for business transactions.

- Overlooking Tax Breaks: Forgetting deductions like 50% of self-employment tax or S Corp benefits can cost thousands. Consider professional advice to structure finances effectively.

Quick tips: Organize records, separate finances, save for taxes, and consult a CPA for major decisions. These steps can save money and reduce stress.

5 Common Tax Mistakes Freelancers Make and How to Avoid Them

Top 5 Tax Mistakes to Avoid | Freelancers, Don’t Do This!

sbb-itb-66f4c95

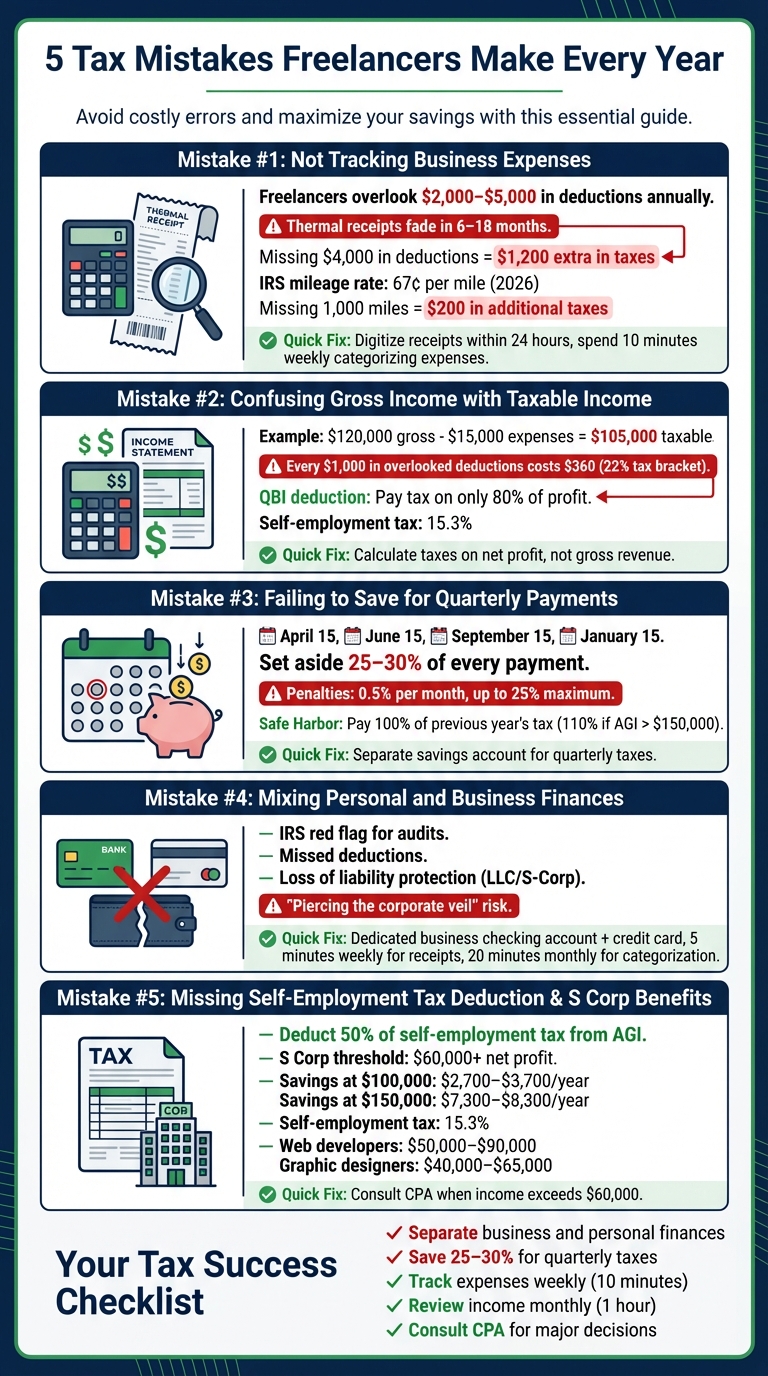

1. Not Tracking Business Expenses Throughout the Year

Freelancers often find themselves scrambling during tax season, hunting for receipts and missing out on thousands of dollars in deductions. On average, freelancers overlook between $2,000 and $5,000 in legitimate tax deductions each year simply because they fail to keep proper records.

To maximize your deductions, you need to record four key details for every expense: amount, date, item description, and business purpose. Without these, you're leaving money on the table. Paper receipts, especially those printed on thermal paper, are unreliable - they can fade within 6 to 18 months, making them unreadable by tax time.

A simple solution? Digitize your receipts within 24 hours. Snap a photo and jot down the business purpose. For items with both personal and business use, like phones or internet services, calculate a consistent business-use percentage (e.g., 50–75% for phones, 40–60% for internet).

Set aside 10 minutes each week to categorize your expenses into IRS Schedule C categories like Advertising, Office Expenses, and Supplies. This small investment of time can save you from the January chaos of reconstructing your records. Here's an example: if you're a freelancer earning $60,000 and you miss $4,000 in deductions, you could end up paying an extra $1,200 in taxes.

"Most freelancers leave thousands of dollars on the table every year because they don't know what qualifies." – Beancount.io

Mileage tracking is another area where freelancers lose out. For 2026, the IRS standard mileage rate is 67 cents per mile. Missing 1,000 business miles could cost you about $200 in additional taxes. Keep a logbook or use an app to track each business trip in real time, noting the date, destination, and business purpose.

Next, we’ll dive into income reporting mistakes that can add even more stress to tax season.

2. Confusing Gross Income with Taxable Income

One common tax mistake is calculating your tax bill based on gross income instead of taxable income. Gross income refers to the total revenue - or "gross receipts" - you receive from clients before deducting any expenses. Taxable income, however, is what remains after subtracting legitimate business expenses and other allowable deductions.

For instance, let’s say you earned $120,000 in gross receipts but spent $15,000 on software, equipment, and office rent. Your net profit would then be $105,000, and this is the figure used to calculate both your self-employment tax (15.3%) and your income tax. Missing out on these deductions could lead to overpaying taxes. For example, if you’re in the 22% tax bracket, every $1,000 in overlooked deductions could cost you an additional $360.

Here’s a breakdown of how income flows through your 2026 tax return: Start by subtracting your business expenses from gross receipts to calculate your net profit. Then, apply above-the-line deductions, such as half of your self-employment tax and health insurance premiums. Next, subtract the standard deduction ($16,100 for single filers) and the 20% Qualified Business Income (QBI) deduction to determine your taxable income.

"Revenue is the top line - gross income. What's left after paying for servers, salaries, marketing, and taxes is net income. They can be dramatically different numbers." – Slava Akulov, Founder, Jupid

The QBI deduction, in particular, can result in substantial savings by allowing you to pay income tax on only 80% of your profit. However, these savings are only achievable if you calculate taxable income accurately. To stay on track, make sure to document every expense, keep personal and business finances separate, and base your tax calculations on net profit rather than gross revenue. Doing so will prepare you to handle additional tax challenges ahead. Up next, learn how to avoid penalties by saving appropriately for quarterly tax payments.

3. Failing to Save for Quarterly Tax Payments

One common mistake freelancers make is not saving for quarterly tax payments. If you’re self-employed and expect to owe $1,000 or more in taxes, you’re required to make quarterly estimated payments. These payments cover both federal income tax and the 15.3% self-employment tax, which funds Social Security and Medicare.

"The US has a pay-as-you-go tax system. That's why employers are responsible for withholding taxes from their employees' paychecks... If you're self-employed and have enough taxable income, your quarterly payments essentially take the place of that withholding." – Justin W. Jones, EA, JD, Keeper Tax

To stay on track, it’s a good idea to set aside 25% to 30% of every payment you receive in a separate savings account. This ensures you’ll have enough to cover your quarterly taxes when they’re due: April 15, June 15, September 15, and January 15. Missing these deadlines can lead to penalties, which start at 0.5% of the unpaid amount per month and can go as high as 25%. The IRS calculates penalties for each quarter individually, so even if you balance out your tax liability later in the year, you can still face penalties for underpaying earlier.

One way to avoid penalties is by following the Safe Harbor rule. If you pay at least 100% of your previous year’s tax liability - or 110% if your adjusted gross income (AGI) exceeded $150,000 - you won’t face penalties, even if your income varies throughout the year. And if you can’t pay the full amount, partial payments still help reduce penalties. For freelancers with fluctuating income, the annualized income installment method lets you adjust your payments during slower months without being penalized.

To calculate your quarterly payment, use IRS Form 1040-ES. This form includes a worksheet to help estimate your annual income, deductions, and credits. A straightforward method is to estimate your total net profit for the year, calculate your self-employment tax (15.3% on 92.35% of net earnings), add your income tax based on your bracket, and divide the total by four. Keeping your personal and business finances separate can make these calculations easier and help you manage your tax savings more efficiently.

4. Combining Personal and Business Finances

Keeping personal and business finances separate is crucial for accurate bookkeeping and tax preparation. When you use the same bank account or credit card for both, it can create unnecessary confusion. For instance, was that $47 Amazon charge for office supplies or a personal purchase? This kind of mix-up can lead to missed deductions, ultimately increasing your tax bill.

"Commingling is a huge IRS red flag, which may increase your risk for a tax audit. The IRS may question the legitimacy of your deductions and disallow those that aren't clearly business-related." – Business Tax Relief

The fix is simple: open a dedicated checking account and credit card exclusively for business use. With this setup, all business income and expenses stay in one place. This makes it easier to track cash flow, claim deductions, and maintain clean records - especially useful if the IRS ever comes knocking. Plus, it reduces the chances of an audit and streamlines your quarterly tax filings.

For freelancers running an LLC or S-Corp, mixing personal and business funds can have even bigger consequences. It increases audit risks and may endanger your liability protection. If courts decide you're not operating as a separate business entity - a situation referred to as "piercing the corporate veil" - your personal assets could be at risk in lawsuits. To make things easier, consider linking your business accounts to accounting tools like QuickBooks (around $25/month) or Wave (which offers a free version) to automate transaction tracking and simplify tax prep.

Set up a routine to stay organized: spend 5 minutes each week capturing receipts and 20 minutes a month categorizing transactions. For expenses that are both personal and business-related, like your phone or internet, calculate a reasonable business-use percentage - this is often between 50% and 70% - and document it properly.

5. Missing the Self-Employment Tax Deduction and S Corp Benefits

Even if you're diligent with tracking expenses and making quarterly payments, skipping over major tax breaks can cost you big time.

Freelancers have the option to deduct 50% of their self-employment tax when calculating their adjusted gross income. This deduction doesn’t reduce the self-employment tax itself, but it does lower your federal income tax. Why does this matter? Because freelancers are on the hook for the entire 15.3% self-employment tax, which covers both the employer and employee portions of Social Security and Medicare.

Another commonly overlooked opportunity is electing S Corp status, which can lead to significant savings if your net profit regularly exceeds $60,000. By choosing this status, you can divide your income into two parts: a "reasonable" W-2 salary (subject to the 15.3% tax) and shareholder distributions, which are not subject to that tax. For example, if your net profit is $100,000, this strategy could save you about $2,700 to $3,700 per year. At $150,000, the savings jump to $7,300 to $8,300 annually.

"At 15.3%, self-employment tax is often a bigger bill than federal income tax for people earning between $50,000 and $150,000 a year." – Slava Akulov, Founder, Jupid

To maximize S Corp benefits, it’s essential to set a "reasonable" salary based on industry benchmarks. For instance:

- Web developers might set salaries between $50,000 and $90,000.

- Graphic designers might aim for $40,000 to $65,000.

A common starting point for freelancers is a 60/40 split between salary and distributions. However, there are extra costs to factor in:

- Payroll services: $30 to $100 per month.

- Filing Form 1120-S: $1,000 to $3,500 annually.

- Franchise taxes: Some states, like California, charge around $800 per year.

Setting up an S Corp takes preparation. You’ll need to:

- Form an LLC or corporation.

- File IRS Form 2553 by March 15.

- Use payroll software (e.g., Gusto or QuickBooks) and consult with a CPA to document your "reasonable salary." Keep in mind, the IRS pays close attention to compensation levels in S Corps, so proper documentation is key.

Conclusion

Steering clear of these common tax mistakes can safeguard your cash flow and make tax season far less stressful. By sticking to straightforward, consistent habits, you can avoid errors like neglecting expense tracking or overlooking deductions - issues that are entirely preventable.

Start by keeping your business and personal finances separate. Set aside 25%–30% of every payment in a specific tax savings account right away. Dedicate an hour each month to organizing your expenses and checking your income projections. Tools like Expensify or QuickBooks make it easier to scan receipts and store them in monthly cloud folders, simplifying the entire process.

Don’t lose track of quarterly tax deadlines. Missing them could result in underpayment penalties.

Finally, consider working with a CPA who specializes in self-employment. They can help you navigate tricky decisions, like whether to opt for an S Corp structure once your income hits around $60,000 to $70,000. Plus, the cost of their services is tax-deductible.

FAQs

What counts as a business expense for freelancers?

Freelancers often face a variety of business expenses that are considered both ordinary and necessary for keeping their operations running smoothly. Some of the most common tax-deductible expenses include:

- Home office costs: If you have a dedicated workspace at home, you can deduct a portion of your rent or mortgage, utilities, and maintenance.

- Internet and phone usage: The business-related portion of your internet and phone bills can be written off.

- Equipment and software: Tools like laptops, printers, or design software that are essential for your work qualify as deductions.

- Work-related travel: Costs like airfare, lodging, and meals during business trips can be included.

- Professional development: Expenses for courses, certifications, or workshops that enhance your skills are deductible.

- Health insurance premiums: Freelancers can often deduct the cost of their health insurance.

These deductions are an effective way to lower your taxable income when it's time to file your taxes.

How do I estimate my quarterly taxes if my income varies?

To calculate quarterly taxes when your income varies, start by using your recent income to project your total earnings for the year. Divide that annual estimate by four to determine your quarterly payment. It's important to update your estimates regularly based on actual income to avoid penalties for underpayment. Tools like IRS Form 1040-ES or an online tax calculator can make this process easier. The IRS requires quarterly payments based on your best estimate of income, so be sure to adjust your calculations if your earnings change significantly.

When does an S Corp start making sense for a freelancer?

When freelancers reach an annual profit of around $60,000 or more, forming an S Corp can help them save on taxes. This setup reduces self-employment taxes, potentially keeping more money in your pocket. It's a smart move to consult a tax professional to see if this option fits your financial situation and goals.