Payment Collection Methods: Complete Guide for 2026

Payment Collection Methods: Complete Guide for 2026

Getting paid on time is one of the biggest challenges freelancers face in 2026. Late payments affect 60% of freelancers, with 42% missing personal bill payments and losing 20 hours monthly chasing overdue invoices. Add hidden fees, like up to 10% for cross-border payments, and freelancers often lose significant income.

Here’s how to simplify payment collection while reducing delays and fees:

- ACH Transfers: Low-cost, reliable for domestic payments, but slower (1–3 days standard). Same-Day ACH speeds things up but has limits for high-value transactions.

- Wire Transfers: Fast and final, ideal for large or international payments, though fees are higher ($15–$75).

- Digital Wallets: PayPal, Venmo, and Zelle offer convenience and instant transfers but come with higher fees (2.9%–4.4%).

- Payment Platforms: Tools like Paid on Time secure client payment methods upfront, reducing risks and ensuring smoother transactions.

- Cryptocurrency: Stablecoins like USDC provide low fees and fast cross-border payments but require careful tax compliance.

To maintain steady cash flow:

- Set clear payment terms (e.g., Net 14 or deposits upfront).

- Automate invoicing and reminders.

- Offer multiple payment options to match client preferences.

Choosing the right method depends on your needs - ACH for cost efficiency, wallets for convenience, or crypto for international clients. Balancing client preferences with streamlined tools can help you get paid faster and more reliably.

How Freelancers Get Paid: Invoicing & Payment Setup Made Easy

sbb-itb-66f4c95

ACH and Wire Transfers

Bank-to-bank transfers continue to dominate the payments landscape in 2026, each offering distinct advantages in cost and speed. The ACH network, for instance, handled 33.6 billion payments worth $86.2 trillion in 2024, proving its enduring relevance.

ACH Transfers: Affordable for Domestic Transactions

ACH transfers are processed in batches via the Automated Clearing House network, costing between $0.15 and $3.00 per transaction. While standard transfers typically settle in one to three business days, Same-Day ACH now offers quicker processing with three daily windows at 10:30 AM, 2:45 PM, and 4:45 PM ET. The popularity of Same-Day ACH is evident, with its volume growing 45% year-over-year in 2024 and 336.4 million payments worth $980.3 billion settled in Q2 2025 alone.

One key advantage of ACH transfers is their reversibility. Payments can be reversed or returned within specific timeframes in cases of errors or unauthorized debits. This feature is especially useful for businesses handling subscription billing or working with new clients. ACH also supports both incoming and recurring payments, making it a flexible option.

"A company processing 200 vendor payments per month saves $4,000 to $9,000 annually by using ACH instead of wire transfers." - Brian from Cash Flow Desk

Looking ahead, businesses need to prepare for a critical update: by June 22, 2026, all companies sending ACH payments must comply with NACHA's new rules. These rules require documented fraud detection processes and annual reviews, so ensure your systems meet these standards before the deadline.

While ACH transfers excel in cost-efficiency and flexibility, wire transfers shine when speed and finality are non-negotiable.

Wire Transfers: Fast and Final

Wire transfers operate in real time through systems like Fedwire or SWIFT, with payments typically settling within minutes or hours. This speed comes at a premium, with fees ranging from $15.00 to $50.00 for domestic wires and $35.00 to $75.00 or more for international transfers. However, the benefit is clear: once settled, wire transfers are irrevocable, offering clients absolute certainty that their payment has cleared.

Wire transfers are ideal for situations where same-day settlement is crucial, such as payments exceeding the $1 million cap for Same-Day ACH or transactions involving international clients in over 180 countries. They’re often used for real estate closings, large project deposits, or urgent vendor payments. On an economic scale, the CHIPS clearing system alone processes about $1.9 trillion in payments daily, underscoring its role in handling high-value transactions.

To minimize risks, always verify banking details by contacting your client directly using a phone number from your contract - not one provided in an email. Since wire fraud is irreversible, requiring dual authorization for payments over $10,000 adds an extra layer of security. This simple precaution can protect your accounts from a single compromised email.

Next, we’ll dive into digital payment solutions that further simplify cash flow for freelancers.

Digital Wallets and Payment Platforms

For freelancers, managing cash flow efficiently is crucial, and digital wallets and payment platforms can make a big difference. Digital wallets have become a leading payment method, with over 51% of consumers avoiding businesses that don’t offer them. By 2026, the number of digital wallet users is expected to reach 5 billion.

Digital Wallets: PayPal, Venmo, and Zelle

Digital wallets like PayPal, Venmo, and Zelle each offer distinct benefits. PayPal, for instance, boasts 434 million active users, making it a go-to choice for international transactions. However, its fees can add up: 2.59%–2.99% + $0.49 for domestic payments and up to 4.4% for international ones, with currency conversion markups ranging from 3.0% to 4.0%.

Venmo, on the other hand, works well for businesses targeting U.S.-based clients. Its "Pay with Venmo" feature has a high conversion rate, with 73% of traffic resulting in completed purchases. Fees for Venmo for Business are lower, at 1.9% + $0.10 per transaction.

For freelancers focused on speed and convenience, Zelle is a standout. It offers instant, fee-free transfers directly through integrated banking apps. Given that over 90% of Americans visit small businesses weekly, many clients expect to use their favorite digital payment methods.

"The choice isn't about finding the perfect tool - it's about cutting administrative overhead." – Emily Lauderdale, News Contributor

Which wallet is best for you? If you handle international clients, PayPal’s global network might outweigh its higher costs. For domestic transactions, Zelle’s instant, fee-free service is hard to beat. Meanwhile, Venmo is ideal for clients who already use the platform and enjoy its social features.

While these wallets simplify payments, freelancers often need more than just a way to get paid - they need tools that address invoicing and billing, which leads us to payment platforms.

Payment Platforms: Paid on Time

Digital wallets are great for processing payments, but they don’t solve issues like invoicing, follow-ups, or disputes. That’s where Paid on Time comes in. This platform secures client payment methods upfront and allows freelancers to charge with a single click once a project is completed. It also creates legally binding agreements that outline project details, payment terms, and deliverables. Clients save their payment info during onboarding, ensuring smooth transactions when the work is done.

Freelancers using Paid on Time are charged a flat 5% per transaction - no monthly fees. The platform automatically generates payment records and receipts, saving time and reducing administrative headaches. For project-based work, this approach shifts the focus from “Will I get paid?” to “When will the work be done?” This can be a game-changer, especially since 42% of freelancers report missing bill payments due to delayed client payments.

"Perceived professionalism often influences how seriously clients take your business." – Chris Do, Designer

For freelancers, combining digital wallets with a platform like Paid on Time can help streamline payments, reduce stress, and ensure a more predictable income flow.

Cryptocurrency and Stablecoins

Cryptocurrency and stablecoins are becoming increasingly popular as payment options for freelancers and small businesses. By 2025, 60% of freelancers had received at least one payment in cryptocurrency, while 25% of businesses globally were using crypto for payroll - up from 15% in 2023. For freelancers working with international clients, stablecoins like USDC and USDT provide a practical alternative to traditional payment systems.

Stablecoins offer quick settlement times, often completing transactions in seconds with minimal fees. They operate 24/7, bypassing issues like banking holidays or time zone delays. Between October 2024 and October 2025, stablecoins facilitated $9 trillion in adjusted payment activity, reflecting an 87% year-over-year growth. On networks like Solana or Polygon, transaction fees are often less than $0.01, a stark contrast to traditional cross-border remittance fees, which average 6.49%. For example, NOWPayments charges a 0.5% deposit fee with no withdrawal costs, whereas PayPal’s international fees can climb to 4.4%.

Another advantage of stablecoins is the elimination of chargebacks. Once a blockchain transaction is confirmed, it becomes final and irreversible, protecting freelancers from fraudulent disputes. However, it's crucial to enter wallet addresses correctly to avoid errors. As Cryptowisser aptly puts it:

"Crypto payments work where traditional systems fail, not where they already excel".

Businesses like Namecheap have embraced Bitcoin and stablecoins to benefit from instant settlements and avoid credit card chargebacks.

Security Considerations and Compliance

Freelancers are advised to prioritize stablecoins over volatile cryptocurrencies like Bitcoin to avoid sudden price fluctuations. Using payment processors that automatically convert crypto to fiat can further reduce financial risks. However, tax compliance is a significant factor. The IRS treats cryptocurrency - including stablecoins - as property, meaning every transaction is taxable. Starting January 1, 2026, new rules will require crypto brokers to issue Form 1099-DA for all sales and exchanges, along with cost basis tracking. To simplify compliance, freelancers should document the fair market value of each transaction and use dedicated wallets for business-related payments.

Stablecoins are particularly appealing in regions with unstable banking systems or high inflation. Notably, 56% of Gen Z freelancers are already open to receiving payments in cryptocurrency, hinting at a generational shift in payment preferences. For the lowest fees, networks like Solana or Polygon are ideal, and freelancers should stick to regulated platforms to streamline tax reporting and compliance. Next, we’ll see how these benefits compare to traditional payment methods.

Payment Method Comparison

Payment Methods Comparison: Fees, Speed & Best Use Cases for Freelancers 2026

Understanding the pros and cons of different payment methods is a must for freelancers who want to maintain steady cash flow. Picking the right option often means weighing factors like speed, cost, and - most importantly - client preference. For many freelancers and small businesses, keeping clients happy by offering their preferred payment method often outweighs saving a few dollars on fees. In fact, 78% of freelancers use at least two payment methods to balance reliability, cost, and processing speed.

ACH transfers are a go-to for large domestic invoices due to their minimal fees. On the other hand, digital wallets offer instant authorization and convenience, making them accessible to a global audience. With digital wallet users expected to hit 5 billion by 2026, they’re becoming a popular choice despite higher fees - typically 2.9% + $0.30 for domestic transactions and up to 4.4% for international payments. Meanwhile, cryptocurrency stands out for its low fees (about 0.5% with platforms like NOWPayments), fast cross-border transactions, and zero chargeback risk since blockchain transactions are irreversible.

When it comes to security, each method has its strengths. Digital wallets use advanced tools like tokenization and 3D Secure 2.0 to protect sensitive data. ACH transfers rely on bank-level security, with minimal fraud risk once funds are cleared. Cryptocurrency, being decentralized, requires users to take responsibility for securing their wallets. Interestingly, businesses that provide online payment options often get paid 30% faster and encounter 50% fewer late payments, highlighting how convenience can directly impact revenue.

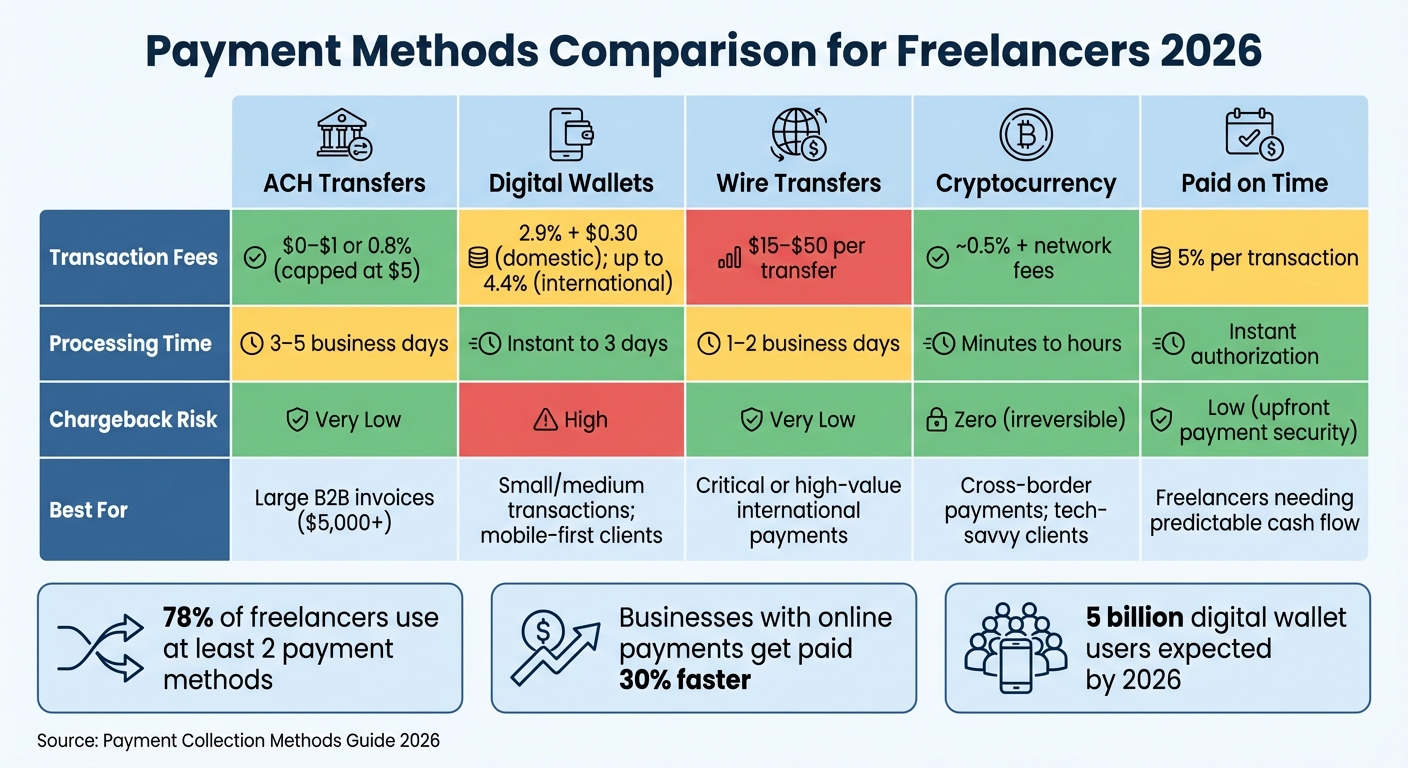

Comparison Table

Here’s a quick breakdown of key features for each payment method:

| Payment Method | Transaction Fees | Processing Time | Chargeback Risk | Best For |

|---|---|---|---|---|

| ACH Transfers | $0–$1 or 0.8% (capped at $5) | 3–5 business days | Very Low | Large B2B invoices ($5,000+) |

| Digital Wallets | 2.9% + $0.30 (domestic); up to 4.4% (international) | Instant to 3 days | High | Small/medium transactions; mobile-first clients |

| Wire Transfers | $15–$50 per transfer | 1–2 business days | Very Low | Critical or high-value international payments |

| Cryptocurrency | ~0.5% + network fees | Minutes to hours | Zero (irreversible) | Cross-border payments; tech-savvy clients |

| Paid on Time | 5% per transaction | Instant authorization | Low (upfront payment security) | Freelancers needing predictable cash flow |

For smaller invoices, quicker options like credit cards or digital wallets may be ideal. Meanwhile, ACH transfers remain the best choice for high-value transactions. By offering a mix of payment methods - ACH for big invoices and digital wallets for speed - you can meet client needs while ensuring a steady income stream.

Next, explore strategies to minimize late payments and maintain a predictable cash flow.

How to Reduce Late Payments and Maintain Cash Flow

Late payments can seriously disrupt cash flow. In fact, 61% of invoices are paid late, often because they’re overlooked or sent to the wrong person. But with a few smart changes, you can improve payment timelines and keep your cash flow steady - even when delays happen.

Start by setting clear payment terms upfront. Businesses that outline payment deadlines in their contracts get paid 20% faster than those that don’t. Clearly state your payment terms - Net 14 is becoming a common choice - along with accepted payment methods and any late fee policies. For larger projects (over $2,000), consider requesting a 25–50% deposit before starting work. This not only boosts your working capital but also helps weed out less committed clients.

Quick invoicing is another game-changer. Sending invoices within 24 hours of completing a project can make payments three times faster. Including a direct "Pay Now" link in your invoices can double that speed again. Make sure invoices go to the right person - usually the Accounts Payable department or a billing portal - not just the project lead.

Automating your follow-up process can save time and improve results. Set up a reminder schedule: send a polite reminder seven days before the due date, a professional nudge on the due date, and progressively firmer follow-ups at 3, 7, and 14 days overdue. This approach can cut the 15 hours small businesses typically spend chasing payments each month in half. Automation has even been shown to reduce payment delays by up to 50%.

Finally, enforce your policies firmly but respectfully. If an invoice is more than 14 days overdue, pause any ongoing work until it’s settled. Just listing late fees on your invoice - even if you don’t enforce them - can encourage clients to pay 15% faster. Offering early payment discounts, such as "2/10 Net 30" (a 2% discount for paying within 10 days), can also speed up payments; 73% of businesses report success with this approach.

Selecting the Right Payment Method

Choosing the best payment method for your business means aligning it with both your clients' preferences and your operational needs. Start by understanding how your clients prefer to pay. For example, corporate clients often stick to ACH transfers or credit cards through established systems, while individual consumers gravitate toward digital wallets for their speed and ease of use. In fact, 70% of consumers report that having their favorite payment method available influences their shopping decisions. If you push clients toward unfamiliar options, you risk delays or even losing sales.

Your business's size and sales channels also play a big role. Freelancers, for instance, tend to focus on minimizing fees to preserve their slim profit margins. On the other hand, larger small businesses aim to strike a balance between boosting conversion rates and maintaining operational efficiency. The type of sales channel matters too:

- If you sell online, digital wallets can help reduce cart abandonment.

- If you operate in person, tap-to-pay options speed up transactions.

- For B2B transactions, ACH and wire transfers are cost-effective for handling high-value invoices.

These nuances make it clear that the "right" payment method depends heavily on your specific business model and customer base.

"The goal is not finding the 'best' tool in theory, but choosing one that reduces uncertainty and administrative overhead." – Paul Jarvis, Freelance Writer

Another critical factor is understanding the true cost of each payment method. Transaction fees are just the starting point. You also need to consider flat fees, international surcharges, currency conversion markups, and chargeback costs. These hidden costs can add up quickly. Additionally, payout speed is a key consideration, especially for managing cash flow. While standard transfers can take 3–7 business days, faster options like RTP (Real-Time Payments) or FedNow provide real-time access to funds, which can be a game-changer for businesses juggling monthly expenses.

Simplifying your payment systems can also make life easier when it comes to tax reporting and reconciliation. Using too many payment tools can complicate the process. Instead, stick to one or two primary methods, and thoroughly test your checkout process to identify any potential friction or hidden fees before they become a problem. This approach not only streamlines operations but also ensures a smoother experience for your customers.

Conclusion

By 2026, payment methods play a critical role in maintaining cash flow, reducing administrative burdens, and preserving professional relationships. Consider this: 61% of invoices are paid late, and 42% of freelancers have missed personal bill payments, such as rent or utilities, due to client payment delays. These numbers highlight the financial strain that an effective payment system can help alleviate.

To succeed, you need a payment approach that balances client preferences with operational efficiency. For example, corporate clients often prefer ACH transfers or credit cards, while individual consumers lean toward digital wallets. Ignoring these preferences can create unnecessary friction, leading to payment delays. Automation is also a game-changer - streamlined workflows and instant notifications can save time and increase income by up to 15% by reducing the effort spent chasing overdue payments. Tools that handle automatic reminders, validate payment details upfront, and generate instant receipts can transform how you manage payments, allowing you to focus on delivering your services rather than tracking down funds.

"The best payment stack won't be the one with the most prominent logos. The best payment solution will make it fast for your good customers, difficult for bad actors, and easy for your accounting team to reconcile." – Sean Marchese, Senior Writer, Payment Nerds

Start by reviewing your recent transactions to identify where delays and hidden fees occur. Many freelancers lose between 3% and 10% of their earnings to fees and currency conversion markups. Once you’ve pinpointed these issues, standardize your payment methods to match how your clients prefer to pay. Test the process from their perspective, and implement automated reminders to minimize manual follow-ups.

While the payment landscape is evolving - with advancements like real-time payment systems (e.g., FedNow), stablecoins for international transactions, and stricter regulatory requirements - the core principles remain unchanged: speed is essential, friction delays payments, and professional tools build trust. By adopting payment solutions that prioritize efficiency and reliability, you can ensure steady cash flow and foster trust with your clients. These strategies not only secure your income but also free you to focus on what truly matters - your work.

FAQs

Which payment method is best for international clients?

When selecting the best payment method for international clients in 2026, it’s all about balancing fees, currency options, and settlement speed.

- Wise stands out for its low-cost cross-border payments, thanks to minimal foreign exchange markups.

- Stripe offers rapid settlements and supports a wide range of currencies, making it a strong choice for businesses with diverse client bases.

- PayPal remains a trusted option globally, though it’s worth noting that its conversion fees can be higher compared to other platforms.

The right choice will ultimately depend on your business requirements and what works best for your clients.

How can I prevent late payments without losing clients?

To ensure payments are on time while keeping clients happy, it's crucial to establish clear payment terms from the start. Specify due dates and outline any late fees to avoid misunderstandings. Automated reminders can be a helpful way to keep deadlines visible, and offering flexible payment options - like deposits or milestone-based payments - can make the process easier for clients. Staying in regular contact and addressing disputes promptly can smooth out any bumps in the process, building trust and ensuring payments are made on schedule without jeopardizing client relationships.

What do I need to track for crypto taxes in 2026?

Starting in 2026, the IRS has specific requirements for tracking cryptocurrency transactions to ensure accurate tax reporting. Here's what you'll need to keep an eye on:

- Gross Proceeds: Record the total amount earned from selling digital assets.

- Cost Basis: Keep detailed records of the original purchase price of each asset, including fees.

- Wallet Movements: Track transfers between wallets to verify ownership and avoid double-counting.

- Transaction Records: Maintain a complete log of all cryptocurrency transactions, including dates and amounts.

It's crucial to maintain accurate records on a per-wallet basis to meet these IRS requirements. Staying organized will help you avoid issues and stay compliant.