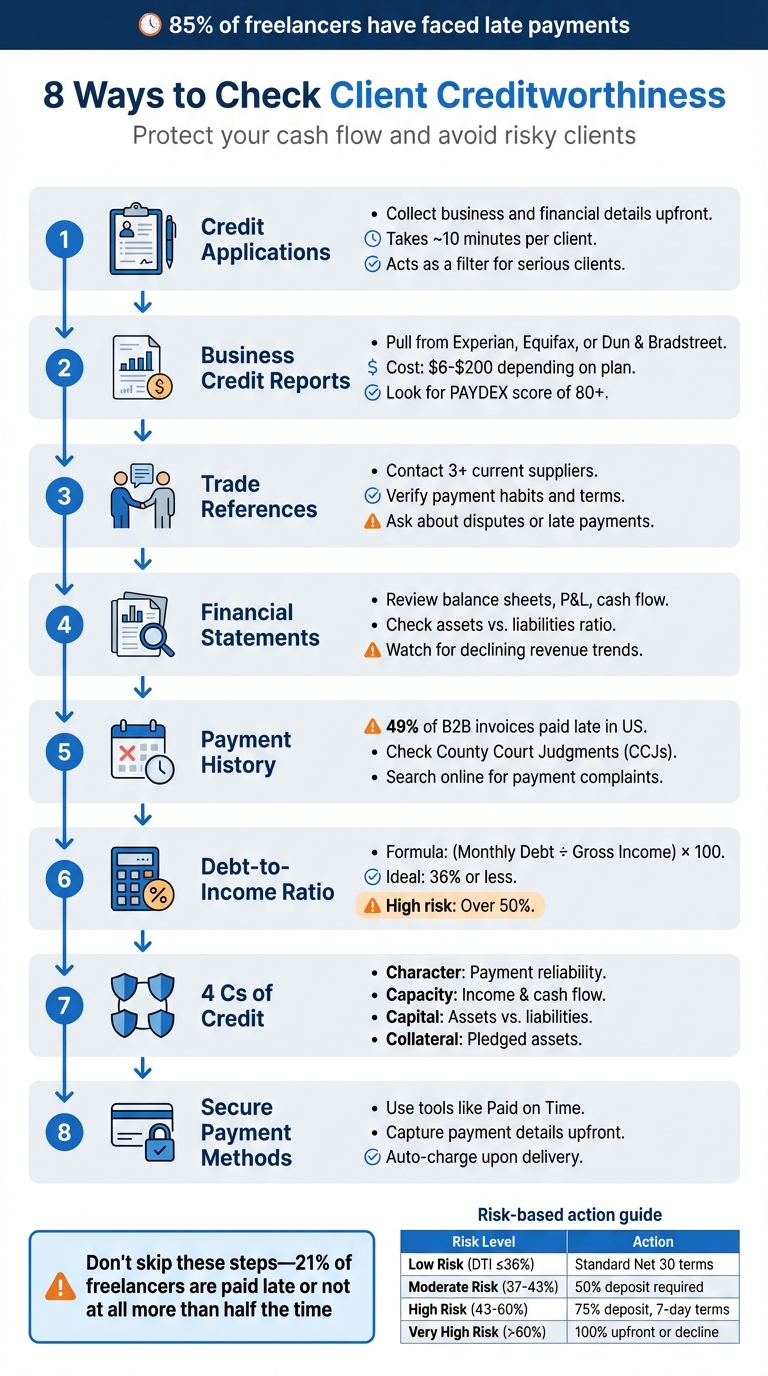

8 Ways to Check Client Creditworthiness

8 Ways to Check Client Creditworthiness

Late payments can hurt your finances. Whether you're a freelancer or a small business owner, ensuring your clients can pay on time is critical. Here's how you can assess their creditworthiness before starting any project:

- Credit Applications: Collect essential business and financial details upfront.

- Business Credit Reports: Use services like Experian or Dun & Bradstreet to review financial health.

- Trade References: Contact their suppliers to verify payment habits.

- Financial Statements: Analyze balance sheets, cash flow, and profit/loss data.

- Payment History: Check past behavior for late or missed payments.

- Debt-to-Income Ratio: Ensure their debt levels are manageable.

- 4 Cs of Credit: Assess Character, Capacity, Capital, and Collateral.

- Secure Payment Methods: Use tools like Paid on Time to guarantee payments.

These steps help you avoid risky clients, protect your cash flow, and ensure you're paid for your work. Don't skip them - it's worth the effort.

8 Steps to Check Client Creditworthiness Before Starting Work

#MasterClass Evaluation of Creditworthiness

sbb-itb-66f4c95

1. Ask Clients to Complete a Credit Application

A credit application is a formal document that gathers key business and financial details from clients before any work begins. It serves as the foundation for assessing potential risks, providing critical information like legal details, contact information, and the necessary authorization to perform background checks, verify references, and evaluate financial stability.

The application should cover essential details, including:

- Basic identity information: full legal business name, registered address, and tax ID or Social Security number.

- Ownership structure: business type and names of key stakeholders.

- Financial records: recent balance sheets or profit and loss statements.

- Trade references: contact details for the client’s bank and at least three suppliers.

Additionally, it must include a signed authorization granting you permission to conduct credit checks and reach out to references.

Effectiveness in Reducing Payment Risks

A credit application does more than collect information - it acts as a filter. Clients unwilling to complete this step or hesitant to sign formal agreements often signal potential payment issues. As Landolio explains:

"Legitimate businesses understand that contracts protect both parties... If they're resisting yours, it's because they don't want to be held accountable to the terms inside it."

The data collected can reveal warning signs, such as declining assets, unresolved court judgments, or a pattern of late filings. By identifying these issues early, you can adjust your terms or decide whether to proceed with the client.

Considering that nearly 60% of B2B transactions involve offering credit, and delinquency rates are at their highest since 2015, this initial step is more important than ever. It lays the groundwork for additional financial vetting methods discussed later.

Ease of Implementation for Freelancers and Small Businesses

Setting up a credit application process is straightforward and doesn’t require fancy software. A simple PDF or Google Form template will do the job. Completing the application takes about 10 minutes per client, and for projects exceeding $1,000, this small effort can save you from significant financial losses down the road.

2. Pull Business Credit Reports from Experian, Equifax, or Dun & Bradstreet

Business credit reports offer a quick snapshot of essential financial data. Unlike personal credit checks, you don’t need a client’s permission to pull a business credit report, unless you’re reviewing the owner’s personal credit under the Fair Credit Reporting Act (FCRA).

Each of the three major bureaus relies on different data sources:

- Dun & Bradstreet (D&B) focuses on trade credit and supplier relationships. They use a D-U-N-S Number to track businesses.

- Equifax sources much of its data from the Small Business Finance Exchange (SBFE), highlighting banking and lender relationships.

- Experian combines trade data, banking records, and public filings, making it a well-rounded option. As SCORE explains:

"Because Experian collects both trade data and bank data, their business credit report could be considered the most balanced of the big three."

Understanding these differences can help you decide which bureau to rely on based on your needs.

Reliability of Credit/Payment History

Business credit reports provide insights into trade payment activity, predictive risk scores (like D&B’s PAYDEX), and public records such as tax liens, judgments, and bankruptcies. For example, a PAYDEX score of 80 or above indicates consistent on-time payments and lower short-term financial risk.

However, there are limitations. Nearly 40% of small-to-medium businesses have less than one month’s operating expenses on hand, and only a fraction of suppliers - about 10,000 out of more than 500,000 - report to business credit agencies. This often results in incomplete data, especially for newer or smaller businesses. To address this, cross-checking reports from multiple bureaus can help fill in the gaps. For high-risk decisions, pulling data from two or three sources provides a clearer picture.

Ease of Implementation for Freelancers and Small Businesses

Getting started is simple. You’ll need the business’s legal name, registered address, and ideally its Employer Identification Number (EIN) to ensure accuracy. Costs vary depending on the bureau and the type of access you need:

| Bureau/Service | Plan Type | Price |

|---|---|---|

| Experian | CreditScore Report | $49.95 (one-time) |

| Experian | Business Credit Advantage | $199/year (unlimited access) |

| Equifax | Single Business Report | ~$99.95 |

| Dun & Bradstreet | Credit Insights Basic | $49/month or $499/year |

For occasional checks, one-time reports are cost-effective. But if you need frequent access, annual subscriptions are a better value. These tools provide a detailed financial picture and can complement other credit checks, helping you make smarter decisions when setting payment terms.

Effectiveness in Reducing Payment Risks

Monitoring credit reports over time can help you spot potential risks early. For instance, a PAYDEX score dropping from 85 to 70 over six months signals worsening financial health, even though 70 might still seem “moderate”. Trends like recent late payments or slower payment speeds often indicate future problems more reliably than a single score.

With commercial loan delinquency rates at their highest since 2015 and 39% of businesses carrying over $100,000 in debt, these reports act as an early warning system. Experian, for example, retains trade data for 36 months and bankruptcy records for nearly 10 years, giving you a long-term view of a client’s financial habits before committing to a project.

3. Contact Trade References

After crunching the numbers, reaching out for trade references can provide a deeper understanding of a client’s payment habits and overall reliability.

Trade references from existing suppliers shed light on how a client handles payments and manages credit. Interestingly, more than half of trade credit decisions are based on the quality of these references.

When speaking with a reference, ask targeted questions. For example, find out how long they’ve worked with the client, the payment terms offered (e.g., 30 or 60 days), whether payments are made on time, the average monthly invoice amounts, any outstanding balances, and if there have been any disputes or collection issues.

Credit consultant Thea Dudley puts it best:

"God may have dibs on where his soul spends eternity, but that does not tell me where he spends his cash."

Reliability of Credit/Payment History

To get the most out of trade references, look for consistent patterns across multiple sources. A single glowing review won’t cut it - aim for at least three references to confirm a client’s behavior. Focus on recent data, particularly from the last 12–24 months, as it reflects the client’s current financial stability. Be cautious of vague or incomplete responses, as they might indicate hidden risks.

For sole proprietors who aren’t listed in business registries, trade references become even more critical for assessing creditworthiness. Don’t just rely on the contacts provided by the client - reach out to their competitors or other vendors directly. Keep in mind that clients are unlikely to give you the names of suppliers who might have had negative experiences with them [15,16].

Ease of Implementation for Freelancers and Small Businesses

Getting started with trade references doesn’t have to be complicated. Simplify the process by offering a form or template that includes checkboxes for payment terms, average monthly sales, and payment timeliness. This makes it easier for references to provide the needed details. Follow up with a direct call to the contact to ask additional questions and capture insights that might not come through on paper.

One hurdle is that credit managers at other companies often have their own priorities, like managing collections, which can push your reference request to the back burner. As Thea Dudley explains:

"Providing a trade reference is the least important thing to do in my day for my company... running down trade references shouldn't be your fail-safe."

Effectiveness in Reducing Payment Risks

Trade references can reveal qualitative details that standard credit reports often miss. These conversations can highlight a client’s professionalism and how they collaborate with suppliers. They might also uncover red flags, like if a client has been cut off by other vendors or has a history of disputes. Consistent, positive feedback from multiple sources is a strong indicator of a dependable credit culture. On the other hand, if references raise concerns, you might want to adjust your terms - like asking for larger upfront deposits or structuring payments around milestones.

4. Review Client Financial Statements

Checking financial statements goes beyond credit reports and references - it offers a direct view of a client's financial health. These documents provide a snapshot of their liquidity and stability, helping you assess their ability to pay. For instance, balance sheets highlight the relationship between assets and liabilities. If liabilities outweigh assets, that's a red flag for high risk. Similarly, profit and loss (P&L) statements can reveal shrinking profit margins or declining revenue trends, while cash flow statements show how well a company handles liquidity.

If you're dealing with U.S.-based public companies, accessing SEC filings is free and straightforward. For private companies, you'll need to request financial statements directly or rely on business credit reports for verified data.

Accuracy of Financial Data

It's crucial to cross-check the financial information clients provide with independent sources. For larger projects, you might want to request a bank reference or letter of credit as an extra layer of verification. Be cautious if a client offers limited financial data while claiming to be well-established - this could signal a shell company or hidden financial troubles.

Once you're confident in the accuracy of the data, gather the necessary documents in a systematic manner to streamline the process.

Ease of Implementation for Freelancers and Small Businesses

For private companies, financial transparency isn't mandatory, so you may need to directly request balance sheets, P&L statements, and cash flow reports. While this can feel awkward for smaller projects, an alternative is to obtain a business credit report. These reports summarize financial data and are often available for as little as $15, saving you from potentially uncomfortable conversations.

Effectiveness in Reducing Payment Risks

When combined with earlier steps, analyzing financial statements gives you a deeper understanding of a client's financial position. These documents offer concrete evidence of their cash flow and assets. For example, a debt-to-income ratio of 36% or lower is generally considered healthy, while higher ratios may indicate financial strain. It's worth noting that corporate profits saw a sharp decline in 2024, making thorough financial reviews even more critical. Additionally, companies that delay filing annual accounts are often more likely to pay suppliers late - or not at all. By regularly reviewing financial statements alongside credit reports, you can better shield yourself from potential payment risks.

5. Check Past Payment History

A client’s past payment history can reveal a lot about their reliability. If a client consistently pays suppliers late - say, 45 days after the due date - you can likely expect the same from them in the future. This makes reviewing payment behavior a key step in assessing risk. In fact, 49% of B2B invoices in the US are paid late, with small business invoices averaging an 8-day delay beyond terms.

Reliability of Credit/Payment History

Business credit reports from companies like Creditsafe or Experian Business provide trade payment data, which highlights a client’s actual payment habits across multiple transactions. These reports can show how many days past due a client typically pays, offering concrete insights instead of relying on assumptions. For publicly traded companies, you can also check SEC filings to see if they submit reports on time - companies that file late often exhibit similar delays in paying suppliers. Additionally, County Court Judgments (CCJs) are a major red flag, as they indicate a company has been legally forced to settle debts in the past.

Ease of Implementation for Freelancers and Small Businesses

Even small businesses and freelancers can easily check a client’s payment history with minimal effort. Start with a quick online search - type "[Company Name] not paying" or "[Company Name] late payment" to uncover any forum discussions or Reddit threads from others who’ve worked with the client. For publicly traded companies, SEC filings are free to access and can provide useful insights. For larger projects (over $1,000), consider purchasing a business credit report for $6–$20 to gain a deeper understanding of payment behavior. If you’re dealing with a sole trader who isn’t listed in corporate registries, ask for references from other freelancers or suppliers they’ve recently worked with.

Effectiveness in Reducing Payment Risks

When combined with credit applications and trade references, analyzing past payment behavior helps you create a complete risk profile for your clients. This allows you to assign risk levels, such as "green" for standard payment terms, "amber" for requiring deposits or shorter payment windows, and "red" for insisting on 100% upfront payment - or even walking away from the deal entirely. Considering that 85% of freelancers have dealt with late payments, and 21% experience late or non-payment more than half the time, this step is essential. Keep in mind that financial health can change, so reassess major clients every 6 to 12 months or immediately after any missed payment.

6. Calculate the Client's Debt-to-Income Ratio

After reviewing a client's financial statements, calculating their debt-to-income (DTI) ratio offers another way to assess their ability to manage payments. The DTI ratio shows what percentage of a client's gross monthly income goes toward debt payments. It's calculated using the formula: (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100. While credit scores reveal whether a client pays bills on time, the DTI ratio highlights how much room they have to take on additional financial commitments.

How Freelancers and Small Businesses Can Use It

Calculating DTI is simple and doesn't require advanced tools. Include recurring debts such as:

- Mortgage or rent payments

- Car loans

- Student loans

- Credit card minimum payments

- Personal loans

- Obligations like child support or alimony

Exclude monthly expenses like utilities, groceries, insurance, or subscriptions, as these aren't classified as debt. Use gross income (pre-tax earnings) for consistency. To ensure accuracy, review 2–3 months of bank statements to confirm recurring debt amounts.

Why DTI Matters for Payment Reliability

The DTI ratio works alongside credit reports and financial statements as a reliable metric for predicting payment behavior. A DTI of 36% or less is ideal, signaling manageable debt levels. Many lenders set 43% as the upper limit for acceptable risk. Ratios above 50% indicate significant financial strain. Clients with high DTI ratios are more likely to delay payments when their cash flow tightens. The table below outlines how to adjust payment terms based on DTI levels:

| DTI Range | Risk Level | Recommended Action |

|---|---|---|

| 36% or less | Low | Standard payment terms (Net 30) |

| 37% – 43% | Moderate | 50% deposit; milestone payments |

| 43% – 60% | High | 75% deposit; 7-day payment terms |

| Over 60% | Very High | 100% upfront or consider declining the project |

7. Apply the 4 Cs of Credit: Character, Capacity, Capital, Collateral

Beyond just reviewing credit reports and payment histories, the 4 Cs framework - Character, Capacity, Capital, and Collateral - offers a practical way to evaluate a client’s creditworthiness. Each "C" focuses on a specific aspect of risk, helping you make informed decisions about extending credit.

Reliability of Credit/Payment History

Character reflects a client’s reliability and payment history. A history of late payments often signals potential future delays. You can verify payment history through straightforward online methods, as discussed earlier. Additionally, platforms like LinkedIn can confirm whether the client operates a legitimate business with active employees, rather than a shell company. Interestingly, psychometric character assessments have proven effective in improving credit access. Data shows that individuals who passed these screenings were four times more likely to secure financing within six months (72% vs. 18%).

"The biggest thing I have learned over the years is if something in my gut is iffy about a customer and their application, you are normally right." - Dawn Collar, Credit Manager, Southern Plumbing & Heating Supply Corp.

Capacity examines whether the client has adequate income and cash flow to meet payment obligations. Look at their business credit score and credit utilization, which should ideally stay below 30%. Warning signs include maxed-out credit lines or reports of declining revenue, which could indicate cash flow issues. Once you’ve assessed these factors, dig deeper into their financial backing.

Accuracy of Financial Data

Capital represents the client’s financial investment in their business. Review their financial statements to assess the ratio of assets to liabilities. A company with negative net assets - where liabilities outweigh assets - carries a higher risk. Pay attention to trends over time; shrinking net assets can indicate a business in decline. Lenders often use a debt-to-income (DTI) ratio below 35% as a benchmark for financial stability.

After evaluating character, capacity, and capital, consider the tangible assets that could secure the client’s obligations. Collateral refers to assets the client might pledge in case of default. While freelancers may rarely have collateral, tools like UCC filings can help determine if a business has pledged assets. For industries like construction, mechanics liens can serve as collateral, securing rights to project property if payments are missed.

Ease of Implementation for Freelancers/Small Businesses

Freelancers and small businesses can easily apply the 4 Cs using affordable tools. For example:

- Business credit reports from providers like Creditsafe or Experian typically cost between $6 and $18 per report.

- County Court Judgment (CCJ) searches are available for about $2.50.

- Trade references are free - simply ask clients for the contact details of 2–3 current suppliers and inquire specifically about their payment habits.

Despite these tools, challenges remain. A 2024 survey revealed that 52% of credit professionals struggle with insufficient information provided by customers, while 24% feel pressured to make rushed decisions.

"We can all cross our T's and dot our I's from a due diligence point of view regarding paperwork, but you still need to establish that relationship with the customer. That's the most important piece of the puzzle." - Mark Zavras, Director of Credit, Sub-Zero Group

Effectiveness in Reducing Payment Risks

The 4 Cs provide a well-rounded view of risk. For instance, a client may excel in one area, like character, but fall short in capacity or capital. By assessing all four factors together, you can make better decisions. If you spot multiple red flags - such as poor payment history (character), high DTI (capacity), and shrinking assets (capital) - it’s wise to require 60–75% upfront deposits or even full payment before starting work.

The small business default rate currently sits at about 2.5%, according to the Equifax Small Business Delinquency Index. Additionally, commercial loan delinquency rates reached their highest level since 2015 in Q2 2024. These statistics underscore the importance of evaluating risks thoroughly before extending credit.

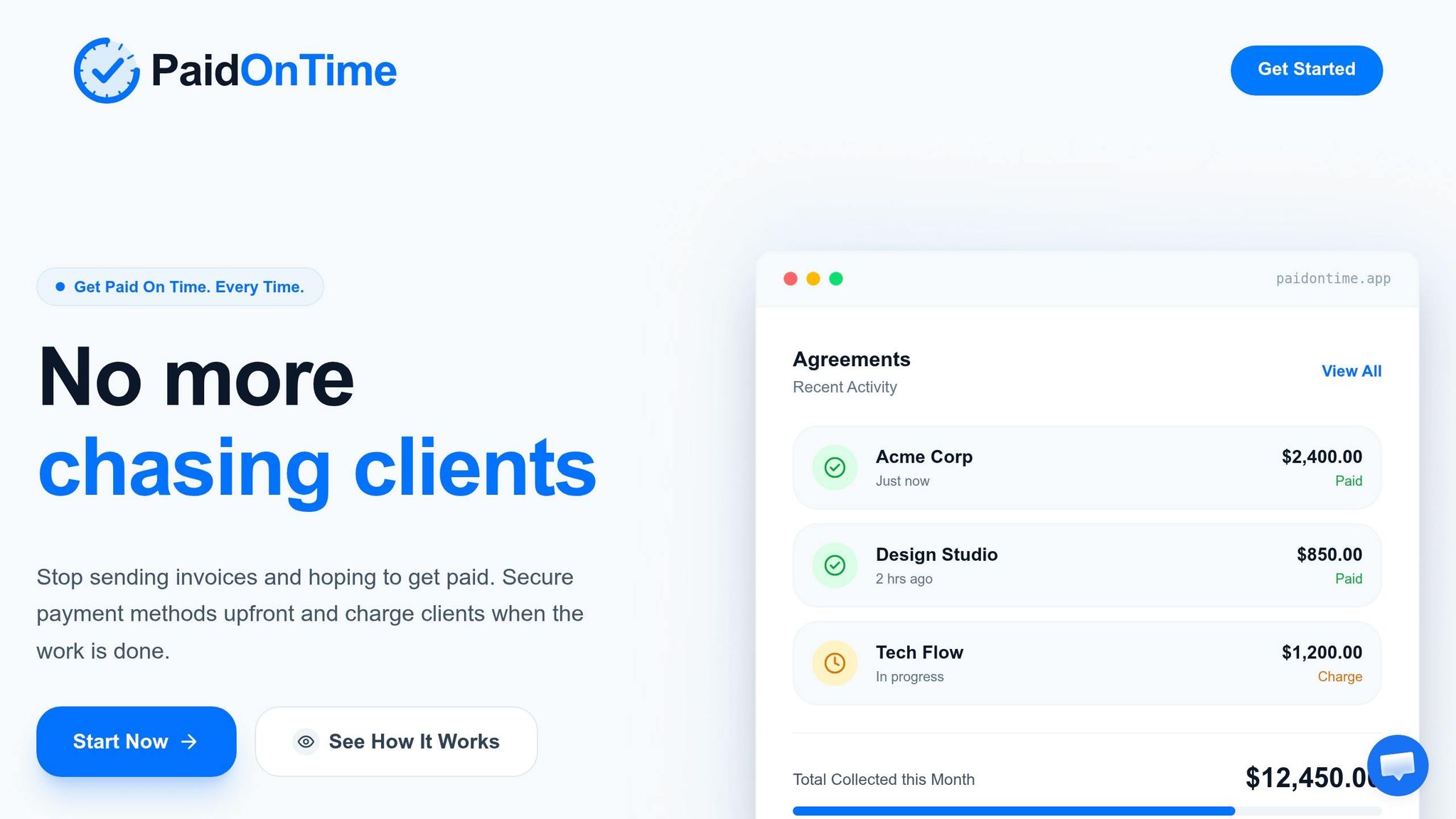

8. Secure Payment Methods Upfront with Paid on Time

Ease of Implementation for Freelancers/Small Businesses

Even with detailed credit checks, ensuring payment can still be tricky. That’s where Paid on Time steps in. This tool lets you secure your client’s payment method upfront, automatically charging the agreed amount once the work is delivered. No more manual invoicing or chasing down payments.

Using PCI DSS-compliant technology, it creates legally binding agreements while keeping payment information secure. Once your project is complete, a single click charges the agreed amount - no waiting for checks or dealing with overdue invoices. The platform charges a 5% transaction fee and has no monthly fees, meaning you only pay when you get paid. After completing credit checks and financial reviews, securing a payment method upfront becomes the final step in safeguarding your earnings.

Effectiveness in Reducing Payment Risks

Even clients with solid credit scores can be unreliable. Late payments are a common issue for freelancers, with 21% reporting they are paid late or not at all more than half the time. By requiring upfront payment details, you can filter out clients who may pose a risk.

"A client who has paid a significant deposit is financially and psychologically invested in the project's success." - PactlyApp

For clients flagged as higher risk, requesting 100% payment upfront can help you avoid potential losses. Another option is to use milestone payments, ensuring the value of completed work never exceeds what has already been paid. Considering that 64% of small businesses deal with late invoice payments and 60% face monthly cash flow challenges, securing upfront payment details transforms guesswork into certainty. By combining thorough credit checks with this approach, you create a robust system for managing payment risks and protecting your cash flow.

Conclusion

Integrating credit applications, financial reviews, and trade references creates a solid foundation for managing payment risks. Assessing a client’s creditworthiness isn’t just a formality - it’s a critical step in protecting your business. A single method rarely paints the full picture; for example, a company might have flawless financial records but a poor history of paying independent contractors. That’s why a multi-layered approach is so important.

The numbers are hard to ignore: 85% of freelancers have faced late payments, and 21% report being paid late or not at all more than half the time. Even a quick vetting process can save you the headache of chasing unpaid invoices for months.

By combining these eight strategies, you can evaluate client creditworthiness more effectively and safeguard your cash flow. Traditional credit checks help confirm whether a client can pay, while tools like Paid on Time ensure payments are processed automatically once work is completed. For clients flagged as high-risk, requesting 100% upfront payment is a smart move. For medium-risk clients, consider increasing deposits to 50–75% and breaking payments into milestones. And always stick to the golden rule: never deliver work worth more than what’s already been paid.

This approach not only protects your earnings but also simplifies your workflow, giving you peace of mind and the confidence to focus on your craft.

FAQs

Which 1–2 credit checks should I do first for a new client?

Start by looking at public credit reports or financial background checks to get a clear picture of the client's credit history. This will help you spot any past issues, like late payments or other financial red flags. After that, review their payment history and references to verify their reliability and confirm they’ve consistently paid on time. Taking these steps ensures you have a solid understanding of their ability to meet payment commitments before moving forward.

What are the biggest red flags that signal a client may not pay?

Key warning signs to look for include hesitation to sign contracts or agree to payment terms, pushback on standard agreements, and indications of financial trouble or dishonesty. Be cautious if you notice unpaid invoices, negative reviews from other freelancers, or actions that hint they might not follow through on their commitments.

How can I secure payment upfront without scaring off good clients?

To make sure you get paid upfront without scaring off reliable clients, establish clear payment terms from the start. Options like deposits, milestone payments, or retainers work well. Be upfront about these policies, presenting them as standard practices that support a smooth working relationship. Use contracts or agreements to spell out payment schedules - this not only protects your income but also reinforces trust and professionalism.