How to Communicate Payment Terms Clearly

How to Communicate Payment Terms Clearly

Getting paid on time starts with being specific about payment terms from the start. Many freelancers face payment delays due to vague agreements like "payment upon completion", which can lead to misinterpretations. Clear payment terms not only ensure smoother cash flow but also help establish professionalism and avoid disputes. Here's what you need to know:

- Set clear due dates: Replace ambiguous terms like "Net 30" with specific dates (e.g., "Payment due by 05/11/2026").

- Require deposits: Ask for 50% upfront, especially for new clients or large projects, to reduce financial risk.

- Define payment methods: Specify accepted methods (e.g., ACH, credit card, PayPal) and clarify who covers fees for international payments.

- Include late fees: State a late fee policy (e.g., 1.5% monthly) to discourage delays.

- Break payments into milestones: For large projects, split payments into phases (e.g., 30% upfront, 40% midpoint, 30% upon delivery).

Always document these terms in contracts and invoices to avoid confusion. Tools like Paid on Time can simplify the process by securing payments upfront and automating invoicing. Clear communication and written agreements ensure you get paid without unnecessary delays.

How to Communicate Your Contract Terms When Onboarding a New Client

sbb-itb-66f4c95

What to Include in Your Payment Terms

Payment terms are about more than just setting deadlines - they're essential for maintaining cash flow, weeding out unreliable clients, and protecting yourself legally. Here's what you should include.

Set Specific Payment Due Dates

Leaving payment terms vague, like simply writing "Net 30", can lead to confusion. While Net 30 is common, invoices with this term are often paid in 38 days on average. The problem? Clients may interpret "Net 30" differently - counting from the invoice date, the date they receive it, or even the date they process it.

To avoid this ambiguity, combine the Net term with a clear calendar date:

"Net 30. Payment due by 05/11/2026."

For freelance work, Net 15 often works best. Use Net 30 for larger, well-established companies, and "Due on Receipt" for smaller jobs under $500.

For bigger projects over $2,000, consider breaking payments into milestones based on deliverables. For example:

- 30% upfront at project kickoff

- 40% at the midpoint review

- 30% upon final delivery

This structure not only helps manage cash flow but also minimizes financial risk if the client relationship takes a turn.

Once you've nailed down due dates, make sure to specify the exact payment amounts and acceptable methods.

State Payment Amounts and Accepted Methods

With due dates in place, be crystal clear about the payment amount and how clients can pay. Include the exact figure and list accepted payment methods:

"Payment of $3,500.00 is due via bank transfer (ACH), credit card, or PayPal."

If you accept credit cards, remember that processing fees (usually 2.9% + $0.30 per transaction) can add up. Decide whether you'll cover these fees or pass them on to the client as a surcharge.

For international clients, always specify the currency (e.g., USD) and clarify who will cover wire transfer fees. For instance, a $50 wire fee on a $1,000 invoice can eat into your profits, so it's worth addressing upfront.

Beyond amounts and methods, make sure to include terms for deposits, late fees, and discounts.

Outline Deposits, Late Fees, and Discounts

Start with a deposit - ideally 50% upfront and non-refundable before any work begins. As PactlyApp highlights, this is "the single most important rule for filtering out non-serious clients and mitigating your financial risk". For trusted clients, you might lower this to 25%, but for projects over $2,000 or new clients, stick to a higher deposit to protect yourself.

Also, include a late fee clause. A common rate is 1.5% to 2% per month on overdue balances. Use the term "late payment charge" instead of "penalty" to avoid legal complications in some areas. Even if you don't enforce it, having this clause shows you mean business and discourages late payments.

To encourage faster payments, consider offering an early payment discount like "2/10 Net 30", where clients get a 2% discount if they pay within 10 days.

Lastly, make it clear that intellectual property rights and final deliverables only transfer to the client after full payment is received. This ensures you maintain leverage until all financial obligations are met.

How to Share Payment Terms with Clients

Setting clear payment terms is just the beginning - you also need to make sure your clients fully understand and agree to them. Relying solely on verbal explanations can lead to misunderstandings. Instead, aim for consistent, transparent communication from the start.

Review Payment Terms in Initial Conversations

Don’t wait until the contract stage to discuss payment terms. Bring them up early, ideally during the discovery call or first meeting when discussing the project scope and pricing. This approach establishes expectations and helps you identify clients who respect timely payments.

Use clear, assertive language. For example, instead of asking, "Would a 50% deposit work for you?", confidently state:

"I require a 50% deposit to secure the project and confirm the kickoff date."

Be on the lookout for warning signs. Clients who resist fair deposit requests, are vague about their budgets, or mention unusual payment policies might indicate future challenges. For instance, if a corporate client brings up a "Net 60" payment cycle, acknowledge their policy but explain that your pricing reflects standard payment terms. If necessary, adjust your rates to account for extended payment timelines.

By addressing payment terms early, you pave the way for a smoother proposal and contract process.

Put Terms in Written Proposals and Contracts

Once you’ve outlined payment terms verbally, follow up with clear, written documentation. Be specific, such as:

"Net 15. Payment due by 04/26/2026."

Highlight the payment section when sending the contract. Better yet, streamline the process by integrating payment terms into the proposal approval system. This allows clients to review the scope, agree to the terms, and pay the deposit all in one step.

Your contract should also include protections for you. For example:

- Specify that intellectual property and final deliverables remain yours until the final invoice is paid in full.

- For milestone-based projects, include a "no payment, no progress" clause, ensuring work on the next phase doesn’t begin until the previous invoice is cleared.

- Add a work suspension clause allowing you to pause services if payments are overdue - e.g., 14 days past the due date.

"A deal isn't done when the client agrees to pay you - a deal is done when the money lands in your bank account." - Alex Berman

Act quickly once terms are discussed. Sending your proposal the same day keeps the momentum going and reinforces your professionalism.

How to Create Clear Invoices

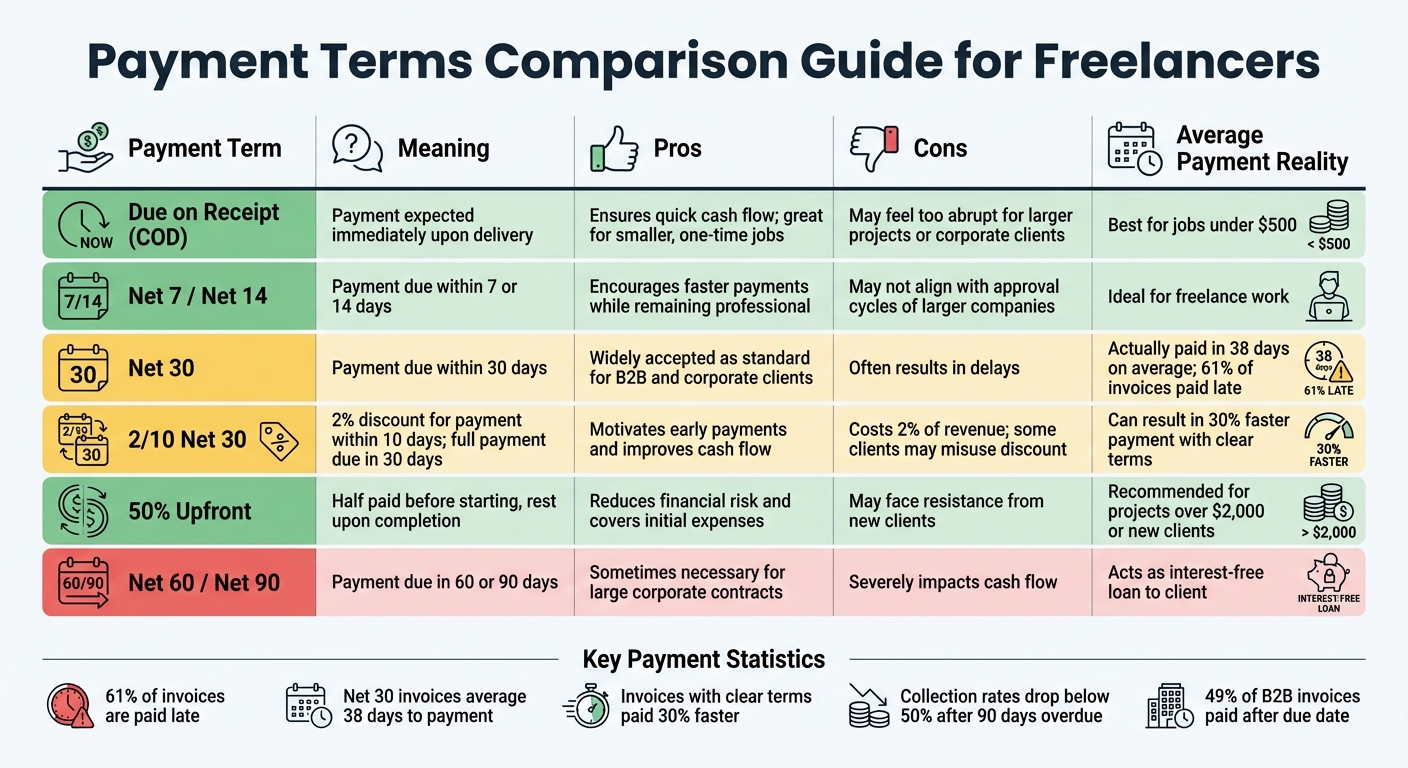

Payment Terms Comparison: Pros, Cons, and Average Payment Times

After crafting clear proposals and contracts, your invoices should follow the same standard of precision. A well-structured invoice not only removes confusion but also speeds up payment. In fact, invoices with clear terms and multiple payment options are settled 30% faster.

Add Required Invoice Information

Make sure your invoice includes all the necessary details to avoid delays. Include your legal name, address, and tax ID (like your EIN), as well as the client’s corresponding information. Assign a unique, sequential invoice number, such as INV-2026-001 or INV-202604-001, and clearly state the invoice date along with a specific due date - for example, "Due: April 25, 2026."

Break down charges into itemized descriptions to provide clarity. For instance, instead of vague terms like "consulting services", specify: "Website redesign consultation - 8 hours @ $125/hour." Display the subtotal, applicable sales tax, and emphasize the total amount due by using bold text or a larger font. To make payment straightforward, include direct bank details, payment links, or a mailing address for checks.

"The goal is not to sound legal. The goal is to remove ambiguity." - CleverInvo

Send your invoices as PDFs to ensure the format remains intact. Clearly outline your late fee policy on the invoice, such as: "A late fee of 1.5% per month applies to overdue balances." Sending the invoice within 24 hours of completing work can result in payments being made 32% faster compared to waiting a week.

Once the essential details are covered, understanding different payment term types can further improve your cash flow strategy.

Payment Term Types Compared

The payment terms you choose can significantly impact your cash flow. Here’s a quick comparison of common options and their effects:

| Payment Term | Meaning | Pros | Cons |

|---|---|---|---|

| Due on Receipt (COD) | Payment expected immediately upon delivery. | Ensures quick cash flow; great for smaller, one-time jobs. | May feel too abrupt for larger projects or corporate clients. |

| Net 7 / Net 14 | Payment due within 7 or 14 days. | Encourages faster payments while remaining professional. | May not align with the approval cycles of larger companies. |

| Net 30 | Payment due within 30 days. | Widely accepted as the standard for B2B and corporate clients. | Often results in delays, with payments averaging 35-45 days. |

| 2/10 Net 30 | 2% discount for payment within 10 days; full payment due in 30 days. | Motivates early payments and improves cash flow. | Costs 2% of revenue, and some clients may misuse the discount and still pay late. |

| 50% Upfront | Half paid before starting, the rest upon completion. | Reduces financial risk and covers initial expenses. | May face resistance from new clients or slow down the sales process. |

| Net 60 / Net 90 | Payment due in 60 or 90 days. | Sometimes necessary for securing large corporate contracts. | Severely impacts cash flow, essentially acting as an interest-free loan to the client. |

It’s worth noting that Net 30 invoices are typically paid in 38 days, and 61% of invoices are paid late. For projects exceeding $3,000, using a 50% upfront deposit or milestone-based payments can protect your cash flow while minimizing risk. A well-crafted invoice not only supports your upfront payment policies but also ensures smoother financial management.

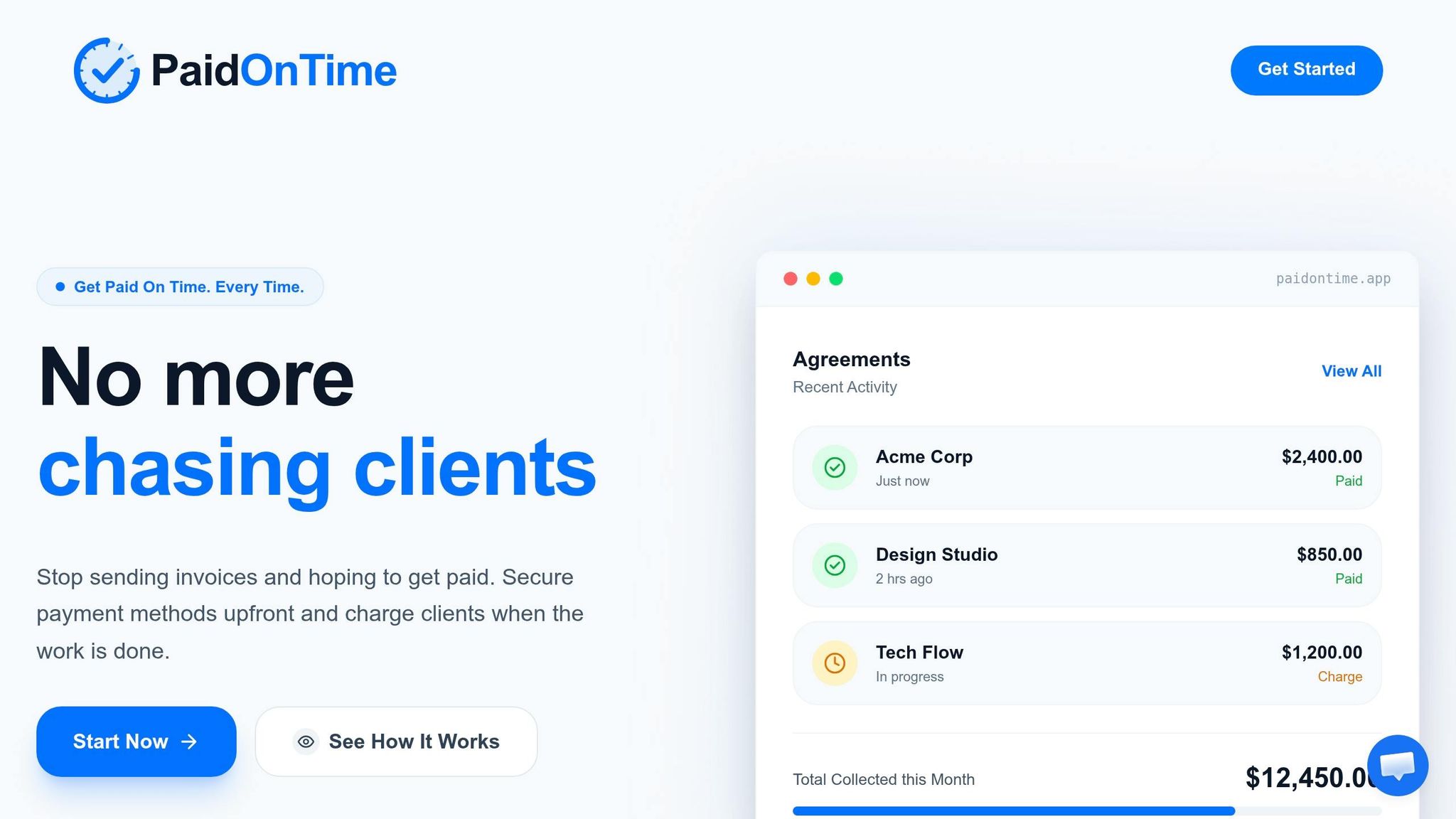

Using Paid on Time to Manage Payments

Chasing payments is one of the biggest headaches of traditional invoicing. Paid on Time changes the game by securing payment methods upfront, letting you charge clients instantly once your work is done. Here’s how the platform ensures you’re paid without the usual hassle.

Collect Payment Methods Before Starting Work

With Paid on Time, you can collect and securely store a client’s payment method before you even begin. When the client approves your proposal, they authorize payment upfront, reducing your financial risk. The system uses tokenization to safeguard sensitive card information, replacing it with a secure reference ID. Once the client gives explicit permission, you’re set to charge them as soon as the project is complete.

Charge Clients with One Click After Completion

Once the work is done, charging your client is as simple as clicking a button. The platform retrieves the stored payment token and processes the transaction through your payment gateway. You can even set up automatic charges for the invoice due date, making the process seamless. Research highlights that one-click checkout solutions speed up transactions by three times compared to traditional methods.

Keep Clear Payment Records

Paid on Time also simplifies record-keeping. The platform automatically generates receipts and stores a searchable transaction history, all accessible through a user-friendly dashboard. You can easily see which invoices are pending, paid, or overdue, helping you identify client payment habits. Plus, all agreements, communications, and payment records are stored in one place, providing a clear paper trail to resolve disputes quickly. The best part? The platform charges a 5% transaction fee with no monthly fees, so you only pay when you get paid.

How to Handle Late Payments

Late payments can still happen even if you’ve sent detailed invoices and required upfront deposits. In the U.S., 49% of B2B invoices are paid after their due date, with small business invoices typically being paid 8 days late. The trick is to handle overdue payments professionally, balancing your cash flow needs with maintaining good client relationships.

Remind Clients About Late Fees

Start with a reminder a few days before the due date - this can help prevent delays. If payment still doesn’t come through, follow up 1–3 days after the due date with a polite nudge. At 7 days overdue, send a firmer reminder, and by 14 days, issue a formal notice that outlines late fees and warns about potential service suspension.

"The goal isn't to 'win' an argument. The goal is to move your invoice through the client's process with clarity, consistency, and a calm tone." - Quick Invoice Tool

Only enforce late fees if they were clearly stated in your original agreement and on the invoice. These fees should encourage timely payments in the future rather than just serve as a penalty. Always include the invoice PDF and direct payment links in every reminder to make it easy for clients to pay without digging through old emails.

Negotiate Payment Plans When Needed

For clients experiencing financial difficulties, consider offering a written payment plan. A common approach might split the balance into three installments, such as 30% upfront, 35% in 30 days, and the remaining 35% in 60 days. Be clear that missing any installment will make the full balance due immediately. To protect your business, pause any ongoing work until the first payment is received and the plan is formalized in writing.

Keep in mind that collection rates drop below 50% for invoices overdue by more than 90 days. Acting swiftly when payments are delayed can help you maintain a steady cash flow while addressing client concerns thoughtfully.

Conclusion

Clear payment terms are not just a formality - they are a cornerstone of a successful freelance business. By specifying due dates, requiring upfront deposits, and formalizing agreements in writing, you can make payment collection a natural part of your workflow while reducing the risk of disputes.

These practices do more than ensure timely payments; they also simplify project management. For example, asking for a 50% deposit can help weed out clients who aren’t serious, while setting Net 15 terms with exact dates removes any confusion about deadlines. For larger projects, milestone billing keeps your financial exposure to a manageable 30–40%, providing an added layer of security and professionalism. Each clear payment term you establish brings you closer to a more stable and efficient freelance operation.

Tools like Paid on Time take these principles further by offering features such as legally binding agreements, upfront payment collection, and one-click invoicing upon project completion. By automating these processes, you can save time, avoid the hassle of chasing payments, and focus on delivering quality work.

FAQs

What payment terms should I use for a new client?

For new clients, it's crucial to set clear payment terms to safeguard your cash flow. A popular choice is specifying a due date, such as Net 30, which requires payment within 30 days. Another option is asking for an upfront deposit - often 50% before starting work. This not only helps weed out clients who aren't committed but also ensures you're not left unpaid for your efforts. Be sure to communicate these terms clearly from the start, and you might want to include late fees to prevent misunderstandings or disputes down the line.

How do I handle a client who insists on Net 60?

If a client insists on Net 60 terms, it's important to negotiate safeguards to protect your cash flow. One effective approach is to request a 40–50% upfront deposit. This reduces the risk of delayed or missed payments. Additionally, make sure your contract includes a late fee clause to encourage prompt payment. By setting clear expectations and securing partial payment upfront, you can better protect your income while accommodating longer payment terms like Net 60.

What should I do if an invoice is overdue?

If an invoice goes overdue, begin with a polite reminder shortly after the due date. If payment still hasn’t been made, follow up with a firmer message around the 7-day mark. By 14 days, consider making a phone call to address the issue directly, if necessary. As a final step, send a formal demand letter before exploring legal options. This step-by-step method keeps the process professional while stressing the need for prompt payment.